Merrill Lynch: Nats will privatise ACC

Merrill Lynch: Nats will privatise ACC

Written By:

- Date published:

12:18 pm, July 2nd, 2008 - 93 comments

Categories: national, privatisation, workers' rights -

Tags: ACC, merryl lynch, PriceWaterhouseCoopers

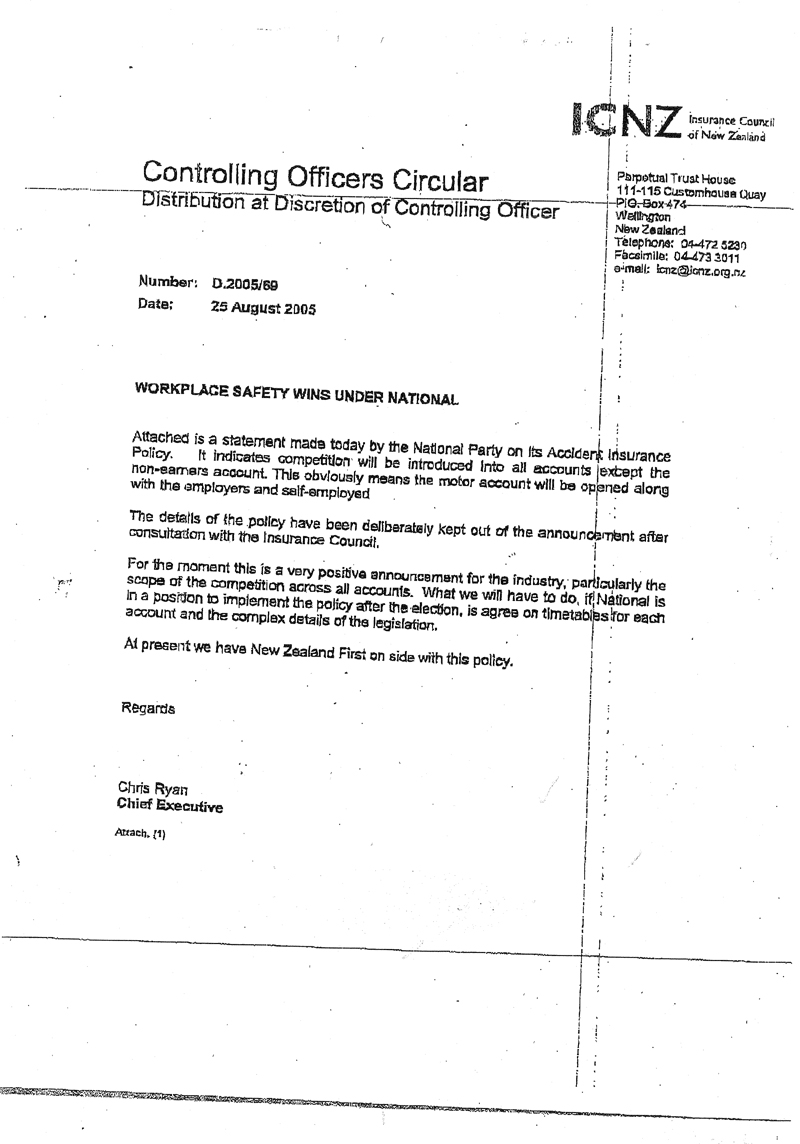

It’s refreshing to see some proper investigative journalism in this morning’s Dominion Post, with a revelation from Vernon Small that while National continues to try and downplay ACC and talk about “no privatisation in the first term,” a report from John Key’s old firm Merrill Lynch suggests National’s privatisation plans are an open secret among Aussie insurance companies, who are lining up for windfall profits.

“Publicly, as best we can identify, and contrary to the statements made by several insurers we have met with in New Zealand, the National Party has made no formal statement on its plans for the ACC,” the report by analyst Andrew Kearnan says.

“Informally, however, we understand the National Party has been very clear in saying it will privatise the ACC.”

It is expected such a privatisation programme would involve the handing over of the workers’ compensation and motor casualty accounts to private insurers, worth $2.1 billion in new ‘premium’ income to the Aussie insurance companies.

The cost of this will of course fall to ordinary Kiwis, who will be forced to pay higher premiums for reduced coverage, as both Merrill Lynch and PriceWaterhouseCoopers point out. Clearly this is not a party with New Zealanders’ best interests at heart.

It doesn’t take a rocket scientist to figure out National’s telling the public one thing and its backers in the insurance industry another on this one. You’ll recall this is exactly what happened last election when National met secretly with the private insurance lobby to collude on ACC policy, which was then deliberately withheld from the public to avoid political fallout.

Ultimately it worked for National last election – even when the damning memo leaked it was lost in the bustle and confusion of the election campaign and voters went to the polls none the wiser. National’s hoping to get away with the same trick this time; it’s up to the media to make sure that doesn’t happen.

{kind=link}

UPDATE: Selected pages from the Merryl Lynch report [JPEG, 300k] are available by clicking the thumbnails below:

__________

__________

93 comments on “Merrill Lynch: Nats will privatise ACC ”

- Comments are now closed

Links to post

- Comments are now closed

Recent Comments

- Backbone, revisited

The schools are on holiday and the sun is shining in the seaside village and all day long I have been seeing bunches of bikes; Mums, Dads, teens and toddlers chattering, laughing, happy, having a bloody great time together. Cheers, AT, for the bits of lane you’ve added lately around the ...5 hours ago

The schools are on holiday and the sun is shining in the seaside village and all day long I have been seeing bunches of bikes; Mums, Dads, teens and toddlers chattering, laughing, happy, having a bloody great time together. Cheers, AT, for the bits of lane you’ve added lately around the ...5 hours ago - Ministers are not above the law

Today in our National-led authoritarian nightmare: Shane Jones thinks Ministers should be above the law: New Zealand First MP Shane Jones is accusing the Waitangi Tribunal of over-stepping its mandate by subpoenaing a minister for its urgent hearing on the Oranga Tamariki claim. The tribunal is looking into the ...6 hours ago

Today in our National-led authoritarian nightmare: Shane Jones thinks Ministers should be above the law: New Zealand First MP Shane Jones is accusing the Waitangi Tribunal of over-stepping its mandate by subpoenaing a minister for its urgent hearing on the Oranga Tamariki claim. The tribunal is looking into the ...6 hours ago - What’s the outfit you can hear going down the gurgler? Probably it’s David Parker’s Oceans Sec...

Buzz from the Beehive Point of Order first heard of the Oceans Secretariat in June 2021, when David Parker (remember him?) announced a multi-agency approach to protecting New Zealand’s marine ecosystems and fisheries. Parker (holding the Environment, and Oceans and Fisheries portfolios) broke the news at the annual Forest & ...6 hours ago

Buzz from the Beehive Point of Order first heard of the Oceans Secretariat in June 2021, when David Parker (remember him?) announced a multi-agency approach to protecting New Zealand’s marine ecosystems and fisheries. Parker (holding the Environment, and Oceans and Fisheries portfolios) broke the news at the annual Forest & ...6 hours ago - Will politicians let democracy die in the darkness?

Bryce Edwards writes – Politicians across the political spectrum are implicated in the New Zealand media’s failing health. Either through neglect or incompetent interventions, successive governments have failed to regulate, foster, and allow a healthy Fourth Estate that can adequately hold politicians and the powerful to account. ...9 hours ago

Bryce Edwards writes – Politicians across the political spectrum are implicated in the New Zealand media’s failing health. Either through neglect or incompetent interventions, successive governments have failed to regulate, foster, and allow a healthy Fourth Estate that can adequately hold politicians and the powerful to account. ...9 hours ago - Matt Doocey doubles down on trans “healthcare”Citizen Science writes – Last week saw two significant developments in the debate over the treatment of trans-identifying children and young people – the release in Britain of the final report of Dr Hilary Cass’s review into gender healthcare, and here in New Zealand, the news that the ...10 hours ago

- A TikTok Prime Minister.

One night while sleeping in my bed I had a beautiful dreamThat all the people of the world got together on the same wavelengthAnd began helping one anotherNow in this dream, universal love was the theme of the dayPeace and understanding and it happened this wayAfter such an eventful day ...11 hours ago

One night while sleeping in my bed I had a beautiful dreamThat all the people of the world got together on the same wavelengthAnd began helping one anotherNow in this dream, universal love was the theme of the dayPeace and understanding and it happened this wayAfter such an eventful day ...11 hours ago - Texas Lessons

This is a guest post by Oscar Simms who is a housing activist, volunteer for the Coalition for More Homes, and was the Labour Party candidate for Auckland Central at the last election.

This is a guest post by Oscar Simms who is a housing activist, volunteer for the Coalition for More Homes, and was the Labour Party candidate for Auckland Central at the last election....

14 hours ago - Bernard's pick 'n' mix of the news links at 6:06 am

The top six news links I’ve seen elsewhere in the last 24 hours as of 6:06 am on Wednesday, April 17 are:Must read: Secrecy shrouds which projects might be fast-tracked RNZ Farah HancockScoop: Revealed: Luxon has seven staffers working on social media content - partly paid for by taxpayer Newshub ...16 hours ago

The top six news links I’ve seen elsewhere in the last 24 hours as of 6:06 am on Wednesday, April 17 are:Must read: Secrecy shrouds which projects might be fast-tracked RNZ Farah HancockScoop: Revealed: Luxon has seven staffers working on social media content - partly paid for by taxpayer Newshub ...16 hours ago - Fighting poverty on the holiday highway

Turning what Labour called the “holiday highway” into a four-lane expressway from Auckland to Whangarei could bring at least an economic benefit of nearly two billion a year for Northland each year. And it could help bring an end to poverty in one of New Zealand’s most deprived regions. The ...17 hours ago

Turning what Labour called the “holiday highway” into a four-lane expressway from Auckland to Whangarei could bring at least an economic benefit of nearly two billion a year for Northland each year. And it could help bring an end to poverty in one of New Zealand’s most deprived regions. The ...17 hours ago - Bernard's six-stack of substacks at 6:26 pm

Tonight’s six-stack includes: launching his substack with a bunch of his previous documentaries, including this 1992 interview with Dame Whina Cooper. and here crew give climate activists plenty to do, including this call to submit against the Fast Track Approvals bill. writes brilliantly here on his substack ...1 day ago

Tonight’s six-stack includes: launching his substack with a bunch of his previous documentaries, including this 1992 interview with Dame Whina Cooper. and here crew give climate activists plenty to do, including this call to submit against the Fast Track Approvals bill. writes brilliantly here on his substack ...1 day ago - At a glance – Is the science settled?

On February 14, 2023 we announced our Rebuttal Update Project. This included an ask for feedback about the added "At a glance" section in the updated basic rebuttal versions. This weekly blog post series highlights this new section of one of the updated basic rebuttal versions and serves as a ...1 day ago

On February 14, 2023 we announced our Rebuttal Update Project. This included an ask for feedback about the added "At a glance" section in the updated basic rebuttal versions. This weekly blog post series highlights this new section of one of the updated basic rebuttal versions and serves as a ...1 day ago - Apposite Quotations.

1 day ago

1 day ago - What’s a life worth now?

You're in the mall when you hear it: some kind of popping sound in the distance, kids with fireworks, maybe. But then a moment of eerie stillness is followed by more of the fireworks sound and there’s also screaming and shrieking and now here come people running for their lives.Does ...1 day ago

You're in the mall when you hear it: some kind of popping sound in the distance, kids with fireworks, maybe. But then a moment of eerie stillness is followed by more of the fireworks sound and there’s also screaming and shrieking and now here come people running for their lives.Does ...1 day ago - Howling at the MoonKarl du Fresne writes – There’s a crisis in the news media and the media are blaming it on everyone except themselves. Culpability is being deflected elsewhere – mainly to the hapless Minister of Communications, Melissa Lee, and the big social media platforms that are accused of hoovering ...1 day ago

- Newshub is Dead.

I don’t normally send out two newsletters in a day but I figured I’d say something about… the news. If two newsletters is a bit much then maybe just skip one, I don’t want to overload people. Alternatively if you’d be interested in sometimes receiving multiple, smaller updates from me, ...1 day ago

I don’t normally send out two newsletters in a day but I figured I’d say something about… the news. If two newsletters is a bit much then maybe just skip one, I don’t want to overload people. Alternatively if you’d be interested in sometimes receiving multiple, smaller updates from me, ...1 day ago - Seymour is chuffed about cutting early-learning red tape – but we hear, too, that Jones has loose...Buzz from the Beehive David Seymour and Winston Peters today signalled that at least two ministers of the Crown might be in Wellington today. Seymour (as Associate Minister of Education) announced the removal of more red tape, this time to make it easier for new early learning services to be ...1 day ago

- Bryce Edwards: Will politicians let democracy die in the darkness?

Politicians across the political spectrum are implicated in the New Zealand media’s failing health. Either through neglect or incompetent interventions, successive governments have failed to regulate, foster, and allow a healthy Fourth Estate that can adequately hold politicians and the powerful to account. Our political system is suffering from the ...1 day ago

Politicians across the political spectrum are implicated in the New Zealand media’s failing health. Either through neglect or incompetent interventions, successive governments have failed to regulate, foster, and allow a healthy Fourth Estate that can adequately hold politicians and the powerful to account. Our political system is suffering from the ...1 day ago - Was Hawkesby entirely wrong?David Farrar writes – The Broadcasting Standards Authority ruled: Comments by radio host Kate Hawkesby suggesting Māori and Pacific patients were being prioritised for surgery due to their ethnicity were misleading and discriminatory, the Broadcasting Standards Authority has found. It is a fact such patients are prioritised. ...1 day ago

- PRC shadow looms as the Solomons head for electionPRC and its proxies in Solomons have been preparing for these elections for a long time. A lot of money, effort and intelligence have gone into ensuring an outcome that won’t compromise Beijing’s plans. Cleo Paskall writes – On April 17th the Solomon Islands, a country of ...1 day ago

- Climate Change: Criminal ecocideWe are in the middle of a climate crisis. Last year was (again) the hottest year on record. NOAA has just announced another global coral bleaching event. Floods are threatening UK food security. So naturally, Shane Jones wants to make it easier to mine coal: Resources Minister Shane Jones ...1 day ago

- Is saving one minute of a politician's time worth nearly $1 billion?

Is speeding up the trip to and from Wellington airport by 12 minutes worth spending up more than $10 billion? Photo: Lynn Grieveson / The KākāTL;DR: The six news items that stood out to me in the last day to 8:26 am today are:The Lead: Transport Minister Simeon Brown announced ...1 day ago

Is speeding up the trip to and from Wellington airport by 12 minutes worth spending up more than $10 billion? Photo: Lynn Grieveson / The KākāTL;DR: The six news items that stood out to me in the last day to 8:26 am today are:The Lead: Transport Minister Simeon Brown announced ...1 day ago - Long Tunnel or Long Con?Yesterday it was revealed that Transport Minister had asked Waka Kotahi to look at the options for a long tunnel through Wellington. State Highway 1 (SH1) through Wellington City is heavily congested at peak times and while planning continues on the duplicate Mt Victoria Tunnel and Basin Reserve project, the ...2 days ago

- Smoke And Mirrors.

You're a fraud, and you know itBut it's too good to throw it all awayAnyone would do the sameYou've got 'em goingAnd you're careful not to show itSometimes you even fool yourself a bitIt's like magicBut it's always been a smoke and mirrors gameAnyone would do the sameForty six billion ...2 days ago

You're a fraud, and you know itBut it's too good to throw it all awayAnyone would do the sameYou've got 'em goingAnd you're careful not to show itSometimes you even fool yourself a bitIt's like magicBut it's always been a smoke and mirrors gameAnyone would do the sameForty six billion ...2 days ago - What is Mexico doing about climate change?This is a re-post from Yale Climate Connections The June general election in Mexico could mark a turning point in ensuring that the country’s climate policies better reflect the desire of its citizens to address the climate crisis, with both leading presidential candidates expressing support for renewable energy. Mexico is the ...2 days ago

- State of humanity, 2024

2024, it feels, keeps presenting us with ever more challenges, ever more dismay.Do you give up yet? It seems to ask.No? How about this? Or this?How about this?When I say 2024 I really mean the state of humanity in 2024.Saturday night, we watched Civil War because that is one terrifying cliff we've ...2 days ago

2024, it feels, keeps presenting us with ever more challenges, ever more dismay.Do you give up yet? It seems to ask.No? How about this? Or this?How about this?When I say 2024 I really mean the state of humanity in 2024.Saturday night, we watched Civil War because that is one terrifying cliff we've ...2 days ago - Govt’s Wellington tunnel vision aims to ease the way to the airport (but zealous promoters of cycl...Buzz from the Beehive A pet project and governmental tunnel vision jump out from the latest batch of ministerial announcements. The government is keen to assure us of its concern for the wellbeing of our pets. It will be introducing pet bonds in a change to the Residential Tenancies Act ...2 days ago

- The case for cultural connectednessA recent report generated from a Growing Up in New Zealand (GUiNZ) survey of 1,224 rangatahi Māori aged 11-12 found: Cultural connectedness was associated with fewer depression symptoms, anxiety symptoms and better quality of life. That sounds cut and dry. But further into the report the following appears: Cultural connectedness is ...2 days ago

- Useful context on public sector job cutsDavid Farrar writes – The Herald reports: From the gory details of job-cuts news, you’d think the public service was being eviscerated. While the media’s view of the cuts is incomplete, it’s also true that departments have been leaking the particulars faster than a Wellington ...2 days ago

- Gordon Campbell On When Racism Comes Disguised As Anti-racismRemember the good old days, back when New Zealand had a PM who could think and speak calmly and intelligently in whole sentences without blustering? Even while Iran’s drones and missiles were still being launched, Helen Clark was live on TVNZ expertly summing up the latest crisis in the Middle ...2 days ago

- Govt ignored economic analysis of smokefree reversal3 days ago

- True Blue.

True loveYou're the one I'm dreaming ofYour heart fits me like a gloveAnd I'm gonna be true blueBaby, I love youI’ve written about the job cuts in our news media last week. The impact on individuals, and the loss to Aotearoa of voices covering our news from different angles.That by ...3 days ago

True loveYou're the one I'm dreaming ofYour heart fits me like a gloveAnd I'm gonna be true blueBaby, I love youI’ve written about the job cuts in our news media last week. The impact on individuals, and the loss to Aotearoa of voices covering our news from different angles.That by ...3 days ago - Who is running New Zealand’s foreign policy?While commentators, including former Prime Minister Helen Clark, are noting a subtle shift in New Zealand’s foreign policy, which now places more emphasis on the United States, many have missed a key element of the shift. What National said before the election is not what the government is doing now. ...3 days ago

- 2024 SkS Weekly Climate Change & Global Warming News Roundup #15A listing of 31 news and opinion articles we found interesting and shared on social media during the past week: Sun, April 7, 2024 thru Sat, April 13, 2024. Story of the week Our story of the week is about adults in the room setting terms and conditions of ...3 days ago

- Feline Friends and Fragile Fauna The Complexities of Cats in New Zealand’s Conservation Efforts

Cats, with their independent spirit and beguiling purrs, have captured the hearts of humans for millennia. In New Zealand, felines are no exception, boasting the highest national cat ownership rate globally [definition cat nz cat foundation]. An estimated 1.134 million pet cats grace Kiwi households, compared to 683,000 dogs ...

3 days ago - Or is that just they want us to think?

Nice guy, that Peter Williams. Amiable, a calm air of no-nonsense capability, a winning smile. Everything you look for in a TV presenter and newsreader.I used to see him sometimes when I went to TVNZ to be a talking head or a panellist and we would yarn. Nice guy, that ...4 days ago

Nice guy, that Peter Williams. Amiable, a calm air of no-nonsense capability, a winning smile. Everything you look for in a TV presenter and newsreader.I used to see him sometimes when I went to TVNZ to be a talking head or a panellist and we would yarn. Nice guy, that ...4 days ago - Fact Brief – Did global warming stop in 1998?Skeptical Science is partnering with Gigafact to produce fact briefs — bite-sized fact checks of trending claims. This fact brief was written by Sue Bin Park in collaboration with members from our Skeptical Science team. You can submit claims you think need checking via the tipline. Did global warming stop in ...4 days ago

- Arguing over a moot point.

I have been following recent debates in the corporate and social media about whether it is a good idea for NZ to join what is known as “AUKUS Pillar Two.” AUKUS is the Australian-UK-US nuclear submarine building agreement in which … Continue reading ...4 days ago

I have been following recent debates in the corporate and social media about whether it is a good idea for NZ to join what is known as “AUKUS Pillar Two.” AUKUS is the Australian-UK-US nuclear submarine building agreement in which … Continue reading ...4 days ago - No Longer Trusted: Ageing Boomers, Laurie & Les, Talk Politics.4 days ago

- Mortgage rates at 10% anyone?

No – nothing about that in PM Luxon’s nine-point plan to improve the lives of New Zealanders. But beyond our shores Jamie Dimon, the long-serving head of global bank J.P. Morgan Chase, reckons that the chances of a goldilocks soft landing for the economy are “a lot lower” than the ...4 days ago

No – nothing about that in PM Luxon’s nine-point plan to improve the lives of New Zealanders. But beyond our shores Jamie Dimon, the long-serving head of global bank J.P. Morgan Chase, reckons that the chances of a goldilocks soft landing for the economy are “a lot lower” than the ...4 days ago - Sad tales from the leftMichael Bassett writes – Have you noticed the odd way in which the media are handling the government’s crackdown on surplus employees in the Public Service? Very few reporters mention the crazy way in which State Service numbers rocketed ahead by more than 16,000 during Labour’s six years, ...4 days ago

- In Whose Best Interests?On The Spot: The question Q+A host, Jack Tame, put to the Workplace & Safety Minister, Act’s Brooke van Velden, was disarmingly simple: “Are income tax cuts right now in the best interests of lowering inflation?”JACK TAME has tested another MP on his Sunday morning current affairs show, Q+A. Minister for Workplace ...4 days ago

- Don’t Question, Don’t Complain.

It has to start somewhereIt has to start sometimeWhat better place than here?What better time than now?So it turns out that I owe you all an apology.It seems that all of the terrible things this government is doing, impacting the lives of many, aren’t necessarily ‘bad’ per se. Those things ...4 days ago

It has to start somewhereIt has to start sometimeWhat better place than here?What better time than now?So it turns out that I owe you all an apology.It seems that all of the terrible things this government is doing, impacting the lives of many, aren’t necessarily ‘bad’ per se. Those things ...4 days ago - Auckland faces 25% water inflation shock

Three Waters became a focus of anti-Government protests under Labour, but its dumping by the new Government hasn’t solved councils’ funding problems and will eventually hit the back pockets of everyone. Photo: Lynn Grieveson/Getty ImagesTL;DR: The six news items that stood out to me at 8:06 am today are:The Government ...5 days ago

Three Waters became a focus of anti-Government protests under Labour, but its dumping by the new Government hasn’t solved councils’ funding problems and will eventually hit the back pockets of everyone. Photo: Lynn Grieveson/Getty ImagesTL;DR: The six news items that stood out to me at 8:06 am today are:The Government ...5 days ago - Small accomplishments and large ironies

5 days ago

5 days ago - The Song of Saqua: Volume VII

In order to catch up to the actual progress of the D&D campaign, I present you with another couple of sessions. These were actually held back to back, on a Monday and Tuesday evening. Session XV Alas, Goatslayer had another lycanthropic transformation… though this time, he ran off into the ...5 days ago

In order to catch up to the actual progress of the D&D campaign, I present you with another couple of sessions. These were actually held back to back, on a Monday and Tuesday evening. Session XV Alas, Goatslayer had another lycanthropic transformation… though this time, he ran off into the ...5 days ago - Accelerating the Growth Rate?

There is a constant theme from the economic commentariat that New Zealand needs to lift its economic growth rate, coupled with policies which they are certain will attain that objective. Their prescriptions are usually characterised by two features. First, they tend to be in their advocate’s self-interest. Second, they are ...5 days ago

There is a constant theme from the economic commentariat that New Zealand needs to lift its economic growth rate, coupled with policies which they are certain will attain that objective. Their prescriptions are usually characterised by two features. First, they tend to be in their advocate’s self-interest. Second, they are ...5 days ago - The only thing we have to fear is tenants themselves

1. Which of these acronyms describes the experience of travelling on a Cook Strait ferry?a. ROROb. FOMOc. RAROd. FMLAramoana, first boat ever boarded by More Than A Feilding, four weeks after the Wahine disaster2. What is the acronym for the experience of watching the government risking a $200 million break ...5 days ago

1. Which of these acronyms describes the experience of travelling on a Cook Strait ferry?a. ROROb. FOMOc. RAROd. FMLAramoana, first boat ever boarded by More Than A Feilding, four weeks after the Wahine disaster2. What is the acronym for the experience of watching the government risking a $200 million break ...5 days ago - Peters talks of NZ “renewing its connections with the world” – but who knew we had been discon...Buzz from the Beehive The thrust of the country’s foreign affairs policy and its relationship with the United States have been addressed in four statements from the Beehive over the past 24 hours. Foreign Affairs Minister Winston Peters somewhat curiously spoke of New Zealand “renewing its connections with a world ...5 days ago

- Muldoonism, solar farms, and legitimacyNewsHub had an article yesterday about progress on Aotearoa's largest solar farm, at "The Point" in the Mackenzie Country. 420MW, right next to a grid connection and transmission infrastructure, and next to dams - meaning it can work in tandem with them to maximise water storage. Its exactly the sort ...5 days ago

- NZTA does not know how much it spends on conesBarrie Saunders writes – Astonishing as it may seem NZTA does not know either how much it spends on road cones as part of its Temporary Traffic Management system, or even how many companies it uses to supply and manage the cones. See my Official Information Act request ...5 days ago

- If this is Back on Track – let's not.

I used to want to plant bombs at the Last Night of the PromsBut now you'll find me with the baby, in the bathroom,With that big shell, listening for the sound of the sea,The baby and meI stayed in bed, alone, uncertainThen I met you, you drew the curtainThe sun ...5 days ago

I used to want to plant bombs at the Last Night of the PromsBut now you'll find me with the baby, in the bathroom,With that big shell, listening for the sound of the sea,The baby and meI stayed in bed, alone, uncertainThen I met you, you drew the curtainThe sun ...5 days ago - Welfare: Just two timid targets from the National governmentLindsay Mitchell writes – The National Government has announced just two targets for the Ministry of Social Development. They are: – to reduce the number of people receiving Jobseeker Support by 50,000 to 140,000 by June 2029, and – (alongside HUD) to reduce the number of households in emergency ...5 days ago

- The Hoon around the week to April 12Photo: Lynn Grieveson / The KākāTL;DR: The podcast above features co-hosts Bernard Hickey and Peter Bale, along with regular guests Robert Patman on Gaza and AUKUS II, Merja Myllylahti on AUT’s trust in news report, Awhi’s Holly Bennett on a watered-down voluntary code for lobbyists, plus special guest Patrick Gower ...6 days ago

- A Dead Internet?

Hi,Four years ago I wrote about a train engineer who derailed his train near the port in Los Angeles.He was attempting to slam thousands of tonnes of screaming metal into a docked Navy hospital ship, because he thought it was involved in some shady government conspiracy theory. He thought it ...6 days ago

Hi,Four years ago I wrote about a train engineer who derailed his train near the port in Los Angeles.He was attempting to slam thousands of tonnes of screaming metal into a docked Navy hospital ship, because he thought it was involved in some shady government conspiracy theory. He thought it ...6 days ago - Weekly Roundup 12-April-2024Welcome back to another Friday. Here’s some articles that caught our attention this week. This Week in Greater Auckland On Wednesday Matt looked at the latest with the Airport to Botany project. On Thursday Matt covered the revelation that Auckland Transport have to subsidise towing illegally parked cars. ...6 days ago

- Weekly Roundup 12-April-2024Welcome back to another Friday. Here’s some articles that caught our attention this week. This Week in Greater Auckland On Wednesday Matt looked at the latest with the Airport to Botany project. On Thursday Matt covered the revelation that Auckland Transport have to subsidise towing illegally parked cars. ...6 days ago

- Antarctic heat spike shocks climate scientistsA ‘Regime Shift’ could raise sea levels sooner than anticipated. Has a tipping point been triggered in the Antarctic? Photo: Juan Barreto/Getty Images TL;DR: Here’s the top six news items of note in climate news for Aotearoa-NZ this week, and a discussion above that was recorded yesterday afternoon between and ...6 days ago

- Skeptical Science New Research for Week #15 2024Open access notables Global carbon emissions in 2023, Liu et al., Nature Reviews Earth & Environment Annual global CO2 emissions dropped markedly in 2020 owing to the COVID-19 pandemic, decreasing by 5.8% relative to 2019 (ref. 1). There were hopes that green economic stimulus packages during the COVD crisis might mark the beginning ...6 days ago

- Everything will be just fine

In our earlier days of national self-loathing, we made a special place for the attitude derided as she’ll be right.You don't hear many people younger than age Boomer using that particular expression these days. But that doesn’t mean there are not younger people in possession of such an attitude.The likes of ...6 days ago

In our earlier days of national self-loathing, we made a special place for the attitude derided as she’ll be right.You don't hear many people younger than age Boomer using that particular expression these days. But that doesn’t mean there are not younger people in possession of such an attitude.The likes of ...6 days ago - Farmers and landlords are given news intended to lift their confidence – but the media must muse o...Buzz from the Beehive People working in the beleaguered media industry have cause to yearn for a minister as busy as Todd McClay and his associates have been in recent days. But if they check out the Beehive website for a list of Melissa Lee’s announcements, pronouncements, speeches and what-have-you ...6 days ago

- National’s war on rentersWhen the National government came into office, it complained of a "war on landlords". It's response? Start a war on renters instead: The changes include re-introducing 90-day "no cause" terminations for periodic tenancies, meaning landlords can end a periodic tenancy without giving any reason. [...] Landlords will now only ...6 days ago

- DrawnA ballot for two Member's Bills was held today, and the following bills were drawn: Repeal of Good Friday and Easter Sunday as Restricted Trading Days (Shop Trading and Sale of Alcohol) Amendment Bill (Cameron Luxton) Consumer Guarantees (Right to Repair) Amendment Bill (Marama Davidson) The ...6 days ago

- At last some scienceEle Ludemann writes – Is getting rid of plastic really good for the environment? Substituting plastics with alternative materials is likely to result in increased GHG emissions, according to research from the University of Sheffield. The study by Dr. Fanran Meng from Sheffield’s Department of Chemical and Biological Engineering, ...6 days ago

- Something important: the curious death of the School Strike 4 Climate MovementThe Christchurch Mosque Massacres, Covid-19, deep political disillusionment, and the jealous cruelty of the intersectionists: all had a part to play in causing School Strike 4 Climate’s bright bubble of hope and passion to burst. But, while it floated above us, it was something that mattered. Something Important. ...6 days ago

- The day the TV media died…Peter Dunne writes – April 10 is a dramatic day in New Zealand’s history. On April 10, 1919, the preliminary results of a referendum showed that New Zealanders had narrowly voted for prohibition by a majority of around 13,000 votes. However, when the votes of soldiers still overseas ...6 days ago

- What's the point in Melissa Lee?

While making coffee this morning I listened to Paddy Gower from Newshub being interviewed on RNZ. It was painful listening. His hurt and love for that organisation, its closure confirmed yesterday, quite evident.As we do when something really matters, he hasn’t giving up hope. Paddy talked about the taonga that ...6 days ago

While making coffee this morning I listened to Paddy Gower from Newshub being interviewed on RNZ. It was painful listening. His hurt and love for that organisation, its closure confirmed yesterday, quite evident.As we do when something really matters, he hasn’t giving up hope. Paddy talked about the taonga that ...6 days ago - Bernard's Top 10 'pick 'n' mix' at 10:10 am on Thursday, April 11

TL;DR: Here’s the 10 news and other links elsewhere that stood out for me over the last day, as at 10:10 am on Wednesday, April 10:Photo by Iva Rajović on UnsplashMust-read: As more than half of the nation’s investigative journalists are sacked, Newsroom’s Tim Murphy shows what it takes to ...6 days ago

TL;DR: Here’s the 10 news and other links elsewhere that stood out for me over the last day, as at 10:10 am on Wednesday, April 10:Photo by Iva Rajović on UnsplashMust-read: As more than half of the nation’s investigative journalists are sacked, Newsroom’s Tim Murphy shows what it takes to ...6 days ago - Gordon Campbell On Winston Peters’ Pathetic Speech At The UNGood grief, Winston Peters. Tens of thousands of Gazans have been slaughtered, two million are on the brink of starvation and what does our Foreign Minister choose to talk about at the UN? The 75 year old issue of whether the five permanent members should continue to have veto powers ...7 days ago

- Subsidising illegal parkingHopefully finally over his obsession with raised crossings, the Herald’s Bernard Orsman has found something to actually be outraged at. Auckland ratepayers are subsidising the cost of towing, storing and releasing cars across the city to the tune of $15 million over five years. Under a quirk in the law, ...7 days ago

- When 'going for growth' actually means saying no to new social homesTL;DR: These six things stood out to me over the last day in Aotearoa-NZ’s political economy, as of 7:06 am on Thursday, April 11:The Government has refused a community housing provider’s plea for funding to help build 42 apartments in Hamilton because it said a $100 million fund was used ...7 days ago

- https://www.politik.co.nz/?p=12733As the public sector redundancies rolled on, with the Department of Conservation saying yesterday it was cutting 130 positions, a Select Committee got an insight into the complexities and challenges of cutting the Government’s workforce. Immigration New Zealand chiefs along with their Minister, Erica Stanford, appeared before Parliament’s Education and ...7 days ago

- Bernard's six-stack of substacks at 6:06 pm on Wednesday, April 10

TL;DR: Six substacks that stood out to me in the last day:Explaining is winning for journalists wanting to regain trust, writes is his excellent substack. from highlights Aotearoa-NZ’s greenwashing problem in this weekly substack. writes about salt via his substack titled: The Second Soul, Part I ...1 week ago

TL;DR: Six substacks that stood out to me in the last day:Explaining is winning for journalists wanting to regain trust, writes is his excellent substack. from highlights Aotearoa-NZ’s greenwashing problem in this weekly substack. writes about salt via his substack titled: The Second Soul, Part I ...1 week ago - EGU2024 – Picking and chosing sessions to attend virtuallyThis year's General Assembly of the European Geosciences Union (EGU) will take place as a fully hybrid conference in both Vienna and online from April 15 to 19. I decided to join the event virtually this year for the full week and I've already picked several sessions I plan to ...1 week ago

- But here's my point about the large irony in what Luxon is saying

Grim old week in the media business, eh? And it’s only Wednesday, to rework an old upbeat line of poor old Neil Roberts.One of the larger dark ironies of it all has been the line the Prime Minister is serving up to anyone asking him about the sorry state of ...1 week ago

Grim old week in the media business, eh? And it’s only Wednesday, to rework an old upbeat line of poor old Neil Roberts.One of the larger dark ironies of it all has been the line the Prime Minister is serving up to anyone asking him about the sorry state of ...1 week ago - Govt gives farmers something to talk about (regarding environmental issues) at those woolshed meetin...Buzz from the Beehive Hard on the heels of three rurally oriented ministers launching the first of their woolshed meetings, the government brought good news to farmers on the environmental front. First, Agriculture Minister Todd McClay announced an additional $18 million is being committed to reduce agricultural emissions. Not all ...1 week ago

{kind=link}

{kind=link}

{kind=link}

- Release: Dark day for Kiwi kids as a third of Govt cuts affect them

News that 1000 jobs at the Ministry of Education and Oranga Tamariki could go is devastating for future generations of New Zealanders. ...8 hours ago

News that 1000 jobs at the Ministry of Education and Oranga Tamariki could go is devastating for future generations of New Zealanders. ...8 hours ago - Release: Alarm as Government signals further blow to school lunchesMore essential jobs could be on the chopping block, this time Ministry of Education staff on the school lunches team are set to find out whether they're in line to lose their jobs. ...11 hours ago

- Release: Quick, submit – stop Govt’s dodgy approvals billThe Government is trying to bring in a law that will allow Ministers to cut corners and kill off native species, Labour environment spokesperson Rachel Brooking said. ...1 day ago

- Government throws coal on the climate crisis fire

The Government’s policy announced today to ease consenting for coal mining will have a lasting impact across generations. ...1 day ago

The Government’s policy announced today to ease consenting for coal mining will have a lasting impact across generations. ...1 day ago - Release: Public transport costs to double as National looks at unaffordable roading project insteadCancelling urgently needed new Cook Strait ferries and hiking the cost of public transport for many Kiwis so that National can announce the prospect of another tunnel for Wellington is not making good choices, Labour Transport Spokesperson Tangi Utikere said. ...2 days ago

- Release: Cost of living in Auckland still not a priorityA laundry list of additional costs for Tāmaki Makarau Auckland shows the Minister for the city is not delivering for the people who live there, says Labour Auckland Issues spokesperson Shanan Halbert. ...3 days ago

- Greens look to fast-track submissions on harmful lawThe Green Party has today launched a step-by-step guide to help New Zealanders make their voice heard on the Government’s democracy dodging and anti-environment fast track legislation. ...5 days ago

- Release: Govt should stop making people’s lives harder and build more homesThe National Government’s proposed changes to the Residential Tenancies Act will mean tenants can be turfed from their homes by landlords with little notice, Labour housing spokesperson Kieran McAnulty said. ...6 days ago

- Release: Melissa Lee missing in action on mediaThe action Melissa Lee promised to protect democracy and the media sector is missing, Media and Communications spokesperson Willie Jackson said. ...6 days ago

- Landlord Government leaves little hope for rentersThe Government’s announcement on tenancy rules prove that it does not care about renters. ...6 days ago

- Opportunity to build a more sustainable economyGreen Party co-leader Marama Davidson is calling on all parties to support a common-sense change that’s great for the planet and great for consumers after her member’s bill was drawn from the ballot today. ...6 days ago

- Significant step forward in fixing cruel and unjust pastA significant milestone has been reached in the fight to strike an anti-Pasifika and unfair law from the country’s books after Teanau Tuiono’s members’ bill passed its first reading. ...1 week ago

- Missed opportunity but NZ will surely one day recognise the right to a sustainable environmentNew Zealand has today missed the opportunity to uphold the right to a clean, healthy, and sustainable environment, says James Shaw after his member’s bill was voted down in its first reading. ...1 week ago

- Release: Don’t cut our lunches – clear message sent to GovernmentTens of thousands of people are demanding the Government commits to fully funding free and healthy school lunches. ...1 week ago

- Release: Govt makes U-turn on Suicide Prevention OfficeLabour welcomes the Government’s U-turn on the closure of the Suicide Prevention Office, says Labour Mental Health spokesperson Ingrid Leary. ...1 week ago

- CCC issues warning over further climate delayToday’s advice from the Climate Change Commission paints a sobering reality of the challenge we face in combating climate change, especially in light of recent Government policy announcements. ...1 week ago

- Luxon targets lame and lousy example of leadershipIf talk is cheap, Chris Luxon’s “targets” are bankrupt. ...1 week ago

- Luxon targets are lousy example of leadershipIf talk is cheap, Chris Luxon’s “targets” are bankrupt. ...1 week ago

- Release: Commitment to disability communities missing from Govt prioritiesMinister for Disability Issues Penny Simmonds appears to have delayed a report back to Cabinet on the progress New Zealand is making against international obligations for disabled New Zealanders. ...1 week ago

- Methane target review is dangerous duplicationThe Government’s newly announced review of methane emissions reduction targets hints at its desire to delay Aotearoa New Zealand’s urgent transition to a climate safe future, the Green Party said. ...2 weeks ago

- Release: Government must commit to school building project for disabled studentsThe Government must commit to the Maitai School building project for students with high and complex needs, to ensure disabled students from the top of the South Island have somewhere to learn. ...2 weeks ago

- Release: National must take mental health seriouslyMental Health Minister Matt Doocey and his Government colleagues have made a meal of their mental health commitments, showing how flimsy their efforts to champion the issue truly are, says Labour Mental Health spokesperson Ingrid Leary. ...2 weeks ago

- Referendums for Māori wards a racist step backwardsThe Government's imposed referendum on Māori wards is a racist step backwards for Māori representation, and disregards Te Tiriti o Waitangi. ...2 weeks ago

- Release: Job losses at Health not worth it for tax cutsNew Zealand will feel the harm of the National Government’s reckless cuts to jobs at the health ministry for generations, says Ayesha Verrall. ...2 weeks ago

- Press release: No Māori initiatives in Government’s nothing planMāori are yet to see anything from this Government except cuts, reversals and taking our people backwards, Māori Development spokesperson Willie Jackson said. ...2 weeks ago

- Thirty six point PR spinThe Government’s ‘36 point’ plan for the next three months is as pointless as it is hollow. ...2 weeks ago

- Thirty six point PR spinThe Government’s ‘36 point’ plan for the next three months is as pointless as it is hollow. ...2 weeks ago

- Thirty six point PR spinThe Government’s ‘36 point’ plan for the next three months is as pointless as it is hollow. ...2 weeks ago

- Release: Social housing off Government’s to-do listThe Coalition Government’s refusal to commit to ongoing funding for social housing is seeing the sector pull back on developments and families watch their dreams of securing a home fade away, says Labour Housing spokesperson Kieran McAnulty. ...2 weeks ago

- Release: Less money in most people’s pockets this AprilChanges to minimum wage and benefit indexation means many New Zealanders will get less this year, as the Government gives a big tax break to landlords instead. ...2 weeks ago

- Thailand and NZ to agree to Strategic Partnership

Prime Minister Christopher Luxon and his Thai counterpart, Prime Minister Srettha Thavisin, have today agreed that New Zealand and the Kingdom of Thailand will upgrade the bilateral relationship to a Strategic Partnership by 2026. “New Zealand and Thailand have a lot to offer each other. We have a strong mutual desire to build ...5 hours ago

Prime Minister Christopher Luxon and his Thai counterpart, Prime Minister Srettha Thavisin, have today agreed that New Zealand and the Kingdom of Thailand will upgrade the bilateral relationship to a Strategic Partnership by 2026. “New Zealand and Thailand have a lot to offer each other. We have a strong mutual desire to build ...5 hours ago - Government consults on extending coastal permits for portsRMA Reform Minister Chris Bishop and Transport Minister Simeon Brown have today announced the Coalition Government’s intention to extend port coastal permits for a further 20 years, providing port operators with certainty to continue their operations. “The introduction of the Resource Management Act in 1991 required ports to obtain coastal ...9 hours ago

- Inflation coming down, but more work to doToday’s announcement that inflation is down to 4 per cent is encouraging news for Kiwis, but there is more work to be done - underlining the importance of the Government’s plan to get the economy back on track, acting Finance Minister Chris Bishop says. “Inflation is now at 4 per ...9 hours ago

- School attendance restored as a priority in health adviceRefreshed health guidance released today will help parents and schools make informed decisions about whether their child needs to be in school, addressing one of the key issues affecting school attendance, says Associate Education Minister David Seymour. In recent years, consistently across all school terms, short-term illness or medical reasons ...11 hours ago

- Unnecessary bureaucracy cut in oceans sectorOceans and Fisheries Minister Shane Jones is streamlining high-level oceans management while maintaining a focus on supporting the sector’s role in the export-led recovery of the economy. “I am working to realise the untapped potential of our fishing and aquaculture sector. To achieve that we need to be smarter with ...13 hours ago

- Patterson promoting NZ’s wool sector at International CongressAssociate Agriculture Minister Mark Patterson is speaking at the International Wool Textile Organisation Congress in Adelaide, promoting New Zealand wool, and outlining the coalition Government’s support for the revitalisation the sector. "New Zealand’s wool exports reached $400 million in the year to 30 June 2023, and the coalition Government ...1 day ago

- Removing red tape to help early learners thriveThe Government is making legislative changes to make it easier for new early learning services to be established, and for existing services to operate, Associate Education Minister David Seymour says. The changes involve repealing the network approval provisions that apply when someone wants to establish a new early learning service, ...2 days ago

- RMA changes to cut coal mining consent red tapeChanges to the Resource Management Act will align consenting for coal mining to other forms of mining to reduce barriers that are holding back economic development, Resources Minister Shane Jones says. “The inconsistent treatment of coal mining compared with other extractive activities is burdensome red tape that fails to acknowledge ...2 days ago

- McClay reaffirms strong NZ-China trade relationshipTrade, Agriculture and Forestry Minister Todd McClay has concluded productive discussions with ministerial counterparts in Beijing today, in support of the New Zealand-China trade and economic relationship. “My meeting with Commerce Minister Wang Wentao reaffirmed the complementary nature of the bilateral trade relationship, with our Free Trade Agreement at its ...2 days ago

- Prime Minister Luxon acknowledges legacy of Singapore Prime Minister LeePrime Minister Christopher Luxon today paid tribute to Singapore’s outgoing Prime Minister Lee Hsien Loong. Meeting in Singapore today immediately before Prime Minister Lee announced he was stepping down, Prime Minister Luxon warmly acknowledged his counterpart’s almost twenty years as leader, and the enduring legacy he has left for Singapore and South East ...2 days ago

- PMs Luxon and Lee deepen Singapore-NZ tiesPrime Minister Christopher Luxon held a bilateral meeting today with Singapore Prime Minister Lee Hsien Loong. While in Singapore as part of his visit to South East Asia this week, Prime Minister Luxon also met with Singapore President Tharman Shanmugaratnam and will meet with Deputy Prime Minister Lawrence Wong. During today’s meeting, Prime Minister Luxon ...2 days ago

- Antarctica New Zealand Board appointmentsForeign Minister Winston Peters has made further appointments to the Board of Antarctica New Zealand as part of a continued effort to ensure the Scott Base Redevelopment project is delivered in a cost-effective and efficient manner. The Minister has appointed Neville Harris as a new member of the Board. Mr ...2 days ago

- Finance Minister travels to Washington DCFinance Minister Nicola Willis will travel to the United States on Tuesday to attend a meeting of the Five Finance Ministers group, with counterparts from Australia, the United States, Canada, and the United Kingdom. “I am looking forward to meeting with our Five Finance partners on how we can work ...2 days ago

- Pet bonds a win/win for renters and landlordsThe coalition Government has today announced purrfect and pawsitive changes to the Residential Tenancies Act to give tenants with pets greater choice when looking for a rental property, says Housing Minister Chris Bishop. “Pets are important members of many Kiwi families. It’s estimated that around 64 per cent of New ...2 days ago

- Long Tunnel for SH1 Wellington being consideredState Highway 1 (SH1) through Wellington City is heavily congested at peak times and while planning continues on the duplicate Mt Victoria Tunnel and Basin Reserve project, the Government has also asked NZ Transport Agency (NZTA) to consider and provide advice on a Long Tunnel option, Transport Minister Simeon Brown ...3 days ago

- New Zealand condemns Iranian strikesPrime Minister Christopher Luxon and Foreign Minister Winston Peters have condemned Iran’s shocking and illegal strikes against Israel. “These attacks are a major challenge to peace and stability in a region already under enormous pressure," Mr Luxon says. "We are deeply concerned that miscalculation on any side could ...3 days ago

- Huge interest in Government’s infrastructure plansHundreds of people in little over a week have turned out in Northland to hear Regional Development Minister Shane Jones speak about plans for boosting the regional economy through infrastructure. About 200 people from the infrastructure and associated sectors attended an event headlined by Mr Jones in Whangarei today. Last ...5 days ago

- Health Minister thanks outgoing Health New Zealand ChairHealth Minister Dr Shane Reti has today thanked outgoing Health New Zealand – Te Whatu Ora Chair Dame Karen Poutasi for her service on the Board. “Dame Karen tendered her resignation as Chair and as a member of the Board today,” says Dr Reti. “I have asked her to ...5 days ago

- Roads of National Significance planning underwayThe NZ Transport Agency (NZTA) has signalled their proposed delivery approach for the Government’s 15 Roads of National Significance (RoNS), with the release of the State Highway Investment Proposal (SHIP) today, Transport Minister Simeon Brown says. “Boosting economic growth and productivity is a key part of the Government’s plan to ...5 days ago

- Navigating an unstable global environmentNew Zealand is renewing its connections with a world facing urgent challenges by pursuing an active, energetic foreign policy, Foreign Minister Winston Peters says. “Our country faces the most unstable global environment in decades,” Mr Peters says at the conclusion of two weeks of engagements in Egypt, Europe and the United States. “We cannot afford to sit back in splendid ...5 days ago

- NZ welcomes Australian Governor-GeneralPrime Minister Christopher Luxon has announced the Australian Governor-General, His Excellency General The Honourable David Hurley and his wife Her Excellency Mrs Linda Hurley, will make a State visit to New Zealand from Tuesday 16 April to Thursday 18 April. The visit reciprocates the State visit of former Governor-General Dame Patsy Reddy ...5 days ago

- Pseudoephedrine back on shelves for WinterAssociate Health Minister David Seymour has announced that Medsafe has approved 11 cold and flu medicines containing pseudoephedrine. Pharmaceutical suppliers have indicated they may be able to supply the first products in June. “This is much earlier than the original expectation of medicines being available by 2025. The Government recognised ...6 days ago

- NZ and the US: an ever closer partnershipNew Zealand and the United States have recommitted to their strategic partnership in Washington DC today, pledging to work ever more closely together in support of shared values and interests, Foreign Minister Winston Peters says. “The strategic environment that New Zealand and the United States face is considerably more ...6 days ago

- Joint US and NZ declarationApril 11, 2024 Joint Declaration by United States Secretary of State the Honorable Antony J. Blinken and New Zealand Minister of Foreign Affairs the Right Honourable Winston Peters We met today in Washington, D.C. to recommit to the historic partnership between our two countries and the principles that underpin it—rule ...6 days ago

- NZ and US to undertake further practical Pacific cooperationForeign Minister Winston Peters has announced further New Zealand cooperation with the United States in the Pacific Islands region through $16.4 million in funding for initiatives in digital connectivity and oceans and fisheries research. “New Zealand can achieve more in the Pacific if we work together more urgently and ...6 days ago

- Government redress for Te Korowai o WainuiāruaThe Government is continuing the bipartisan effort to restore its relationship with iwi as the Te Korowai o Wainuiārua Claims Settlement Bill passed its first reading in Parliament today, says Treaty Negotiations Minister Paul Goldsmith. “Historical grievances of Te Korowai o Wainuiārua relate to 19th century warfare, land purchased or taken ...6 days ago

- Focus on outstanding minerals permit applicationsNew Zealand Petroleum and Minerals is working to resolve almost 150 outstanding minerals permit applications by the end of the financial year, enabling valuable mining activity and signalling to the sector that New Zealand is open for business, Resources Minister Shane Jones says. “While there are no set timeframes for ...6 days ago

- Applications open for NZ-Ireland Research CallThe New Zealand and Irish governments have today announced that applications for the 2024 New Zealand-Ireland Joint Research Call on Agriculture and Climate Change are now open. This is the third research call in the three-year Joint Research Initiative pilot launched in 2022 by the Ministry for Primary Industries and Ireland’s ...6 days ago

- Tenancy rules changes to improve rental marketThe coalition Government has today announced changes to the Residential Tenancies Act to encourage landlords back to the rental property market, says Housing Minister Chris Bishop. “The previous Government waged a war on landlords. Many landlords told us this caused them to exit the rental market altogether. It caused worse ...6 days ago

- Boosting NZ’s trade and agricultural relationship with ChinaTrade and Agriculture Minister Todd McClay will visit China next week, to strengthen relationships, support Kiwi exporters and promote New Zealand businesses on the world stage. “China is one of New Zealand’s most significant trade and economic relationships and remains an important destination for New Zealand’s products, accounting for nearly 22 per cent of our good and ...6 days ago

- Freshwater farm plan systems to be improvedThe coalition Government intends to improve freshwater farm plans so that they are more cost-effective and practical for farmers, Associate Environment Minister Andrew Hoggard and Agriculture Minister Todd McClay have announced. “A fit-for-purpose freshwater farm plan system will enable farmers and growers to find the right solutions for their farm ...1 week ago

- New Fast Track Projects advisory group namedThe coalition Government has today announced the expert advisory group who will provide independent recommendations to Ministers on projects to be included in the Fast Track Approvals Bill, say RMA Reform Minister Chris Bishop and Regional Development Minister Shane Jones. “Our Fast Track Approval process will make it easier and ...1 week ago

- Pacific and Gaza focus of UN talksForeign Minister Winston Peters says his official talks with the United Nations Secretary-General Antonio Guterres in New York today focused on a shared commitment to partnering with the Pacific Islands region and a common concern about the humanitarian catastrophe in Gaza. “Small states in the Pacific rely on collective ...1 week ago

- Government honours Taranaki Maunga dealThe Government is honouring commitments made to Taranaki iwi with the Te Pire Whakatupua mō Te Kāhui Tupua/Taranaki Maunga Collective Redress Bill passing its first reading Parliament today, Treaty Negotiations Minister Paul Goldsmith says. “This Bill addresses the commitment the Crown made to the eight iwi of Taranaki to negotiate ...1 week ago

- Enhanced partnership to reduce agricultural emissionsThe Government and four further companies are together committing an additional $18 million towards AgriZeroNZ to boost New Zealand’s efforts to reduce agricultural emissions. Agriculture Minister Todd McClay says the strength of the New Zealand economy relies on us getting effective and affordable emission reduction solutions for New Zealand. “The ...1 week ago

- 110km/h limit proposed for Kāpiti ExpresswayTransport Minister Simeon Brown has welcomed news the NZ Transport Agency (NZTA) will begin consultation this month on raising speed limits for the Kāpiti Expressway to 110km/h. “Boosting economic growth and productivity is a key part of the Government’s plan to rebuild the economy and this proposal supports that outcome ...1 week ago

- New Zealand Biosecurity Awards – Winners announcedTwo New Zealanders who’ve used their unique skills to help fight the exotic caulerpa seaweed are this year’s Biosecurity Awards Supreme Winners, says Biosecurity Minister Andrew Hoggard. “Strong biosecurity is vital and underpins the whole New Zealand economy and our native flora and fauna. These awards celebrate all those in ...1 week ago

- Attendance action plan to lift student attendance ratesThe Government is taking action to address the truancy crisis and raise attendance by delivering the attendance action plan, Associate Education Minister David Seymour announced today. New Zealand attendance rates are low by national and international standards. Regular attendance, defined as being in school over 90 per cent of the ...1 week ago

- World must act to halt Gaza catastrophe – PetersForeign Minister Winston Peters has told the United Nations General Assembly (UNGA) in New York today that an immediate ceasefire is needed in Gaza to halt the ongoing humanitarian catastrophe. “Palestinian civilians continue to bear the brunt of Israel’s military actions,” Mr Peters said in his speech to a ...1 week ago

- Speech to United Nations General Assembly: 66th plenary meeting, 78th sessionMr President, The situation in Gaza is an utter catastrophe. New Zealand condemns Hamas for its heinous terrorist attacks on 7 October and since, including its barbaric violations of women and children. All of us here must demand that Hamas release all remaining hostages immediately. At the ...1 week ago

- Ministry of Education plans to cut 565 roles

It makes the proposal the biggest single slash to a public service agency so far. ...1 hour ago

It makes the proposal the biggest single slash to a public service agency so far. ...1 hour ago - Oranga Tamariki proposes to cut more than 400 jobsAbout 1900 roles would be affected overall - either changed or disestablished - in the "scope of restructuring work". ...1 hour ago

- Politics with Michelle Grattan: Independent MP Dai Le on the church attack in her electorate

Source: The Conversation (Au and NZ) – By Michelle Grattan, Professorial Fellow, University of Canberra After the stabbing of Bishop Mar Mari Emmanuel in an Assyrian Orthodox Church in Wakeley on Monday, and the killings in Bondi Junction shopping centre just two days earlier, many people in Sydney and in ...2 hours ago

Source: The Conversation (Au and NZ) – By Michelle Grattan, Professorial Fellow, University of Canberra After the stabbing of Bishop Mar Mari Emmanuel in an Assyrian Orthodox Church in Wakeley on Monday, and the killings in Bondi Junction shopping centre just two days earlier, many people in Sydney and in ...2 hours ago - Government issues guidelines for when sick children should be kept home from schoolCovid-19? Symptoms including fever, vomiting, diarrhoea or head lice? Your children should be at home, new government guidelines say. ...3 hours ago

- Australia’s long-sought stronger environmental laws just got indefinitely deferred. It’s back to...Source: The Conversation (Au and NZ) – By Euan Ritchie, Professor in Wildlife Ecology and Conservation, School of Life & Environmental Sciences, Deakin University We’ve long known Australia’s main environmental protection laws aren’t doing their job, and we know Australians want better laws. Labor was elected promising to fix them. ...4 hours ago

- AI is making smart devices – watches, speakers, doorbells – easier to hack. Here’s how to stay...Source: The Conversation (Au and NZ) – By Chao Chen, Deputy Director, Enterprise AI and Data Analytics Hub, RMIT Univeristy, RMIT University Ivan Bandura/Unsplash From asking our smart speakers for the weather to receiving personalised advice from smartwatches, devices powered by artificial intelligence (AI) are increasingly streamlining our routines ...4 hours ago

- Police Association members reject latest government pay offerPolice Association says members are looking for a sincere effort by the government to address the cost of living crisis and recognise the increasing dangers officers faced. ...4 hours ago

- Global coral bleaching caused by global warming demands a global responseSource: The Conversation (Au and NZ) – By Britta Schaffelke, Manager International Partnerships and Co-ordinator of the Global Coral Reef Monitoring Network (GCRMN), Australian Institute of Marine Science Bleached coral at the Keppel Islands in the southern Great Barrier Reef in early March 2024. © AIMS | Eoghan Aston ...4 hours ago

- The beginnings of modern science shaped how philosophers saw alien life – and how we understand it...Source: The Conversation (Au and NZ) – By Philip C. Almond, Emeritus Professor in the History of Religious Thought, The University of Queensland Wikipedia Speculation about extraterrestrials is not all that new. There was a vibrant debate in 17th-century Europe about the existence of life on other planets. ...5 hours ago

- Families including someone with mental illness can experience deep despair. They need supportSource: The Conversation (Au and NZ) – By Amanda Cole, Lead, Mental Health, Edith Cowan University In the aftermath of the tragic Bondi knife attack, Joel Cauchi’s parents have spoken about their son’s long history of mental illness, having been diagnosed with schizophrenia at age 17. They said they were ...5 hours ago

- How Fast-track Consenting Might Impact The Environment – Expert Reaction

Submissions on the Fast-track Approvals Bill close at the end of Friday. The law would allow major infrastructure projects to bypass lengthy resource consenting processes – being assessed instead by an expert panel , with Ministers ultimately having ...5 hours ago

Submissions on the Fast-track Approvals Bill close at the end of Friday. The law would allow major infrastructure projects to bypass lengthy resource consenting processes – being assessed instead by an expert panel , with Ministers ultimately having ...5 hours ago - Changes To ECE RegulationsIn QPEC's view, the Coalition changes to ECE announced mid-April are exactly the opposite of what is needed The Issue David Seymour is loosening regulations and qualifications for Early Childhood Centres, removing government signoff for new ...6 hours ago

- NZDSN Opinion: Organisations Must Do Better For Disabled New ZealandersWe at New Zealand Disability Support Network applaud the Commerce Commission for filing proceedings against One NZ for their latest failure on 111 Contact Code. It doesn’t take much to think of harmful or fatal scenarios for people with disabilities ...6 hours ago

- Caviar Before Children"Caviar before children is what has happened today!” says Pat Newman spokesperson for Te Tai Tokerau Principals Association "The cuts to day to both the Ministry of Education and Oranga Tamariki, point to a government hell bent on delivering tax ...6 hours ago

- Gone By Lunchtime: Aukus ruckus reveals division on foreign policy direction

Is New Zealand’s trumpeted independent foreign policy in peril? Helen Clark has raised the alarm over New Zealand inching towards a pillar two status with Aukus, warning of a “profoundly undemocratic” direction of travel away from the independent foreign policy forged over four decades. Peters, foreign minister today and for ...6 hours ago

Is New Zealand’s trumpeted independent foreign policy in peril? Helen Clark has raised the alarm over New Zealand inching towards a pillar two status with Aukus, warning of a “profoundly undemocratic” direction of travel away from the independent foreign policy forged over four decades. Peters, foreign minister today and for ...6 hours ago - Inspectorate Report Shows Prisoners Denied Entitlement To Daily Time Out Of CellsA report from the Office of the Inspectorate shows that prisoners in three units at Auckland Prison were not able to leave their cells every day for many months. For up to nine months (until mid-July 2023), prisoners in three units were denied ...7 hours ago

- 'I thought we were friends': Dave Letele reveals falling out with PM Christopher LuxonCommunity leader Dave Letele considered Christopher Luxon a friend - until the PM reacted badly to an open letter he signed decrying racism. ...7 hours ago

- Watch: Luxon defends hosting Myanmar officials at ASEAN conferencePrime Minister Christopher Luxon says the government condemns outright the Myanmar coup, and NZ is simply following the policy set by ASEAN. ...7 hours ago

- You could help minimise harm in a public attack. Here’s what it means to be a ‘zero responder’Source: The Conversation (Au and NZ) – By Milad Haghani, Senior Lecturer of Urban Mobility, Public Safety & Disaster Risk, UNSW Sydney The tragic Westfield attack in Sydney highlights the vulnerability of crowded public spaces. Six people were killed and many were injured by a knife-wielding attacker in a short ...7 hours ago

- Could not getting enough sleep increase your risk of type 2 diabetes?Source: The Conversation (Au and NZ) – By Giuliana Murfet, Casual Academic, Faculty of Health, University of Technology Sydney Andrey_Popov/Shutterstock Not getting enough sleep is a common affliction in the modern age. If you don’t always get as many hours of shut-eye as you’d like, perhaps you were concerned ...7 hours ago

- Ministry of Education to cut 565 roles, more than 400 to go at Oranga TamarikiThe announcement comes hours after Oranga Tamariki announced it was axing 400 roles. ...8 hours ago

- Ministers announce plan to extend port permits by 20 yearsPorts are having their permits for pre-RMA activities extended so they won't need to obtain new ones before September 2026. ...8 hours ago

- ‘Coffee table books or Dune’: Secrets from the bookshop floorWelcome to The Spinoff Bookseller Confessional, in which we get to know Aotearoa’s booksellers. This week: Lisa Jean O’Reilly, bookseller at Unity Books Auckland. The weirdest question/request you’ve had on the shop floor Last week a couple came into the store, holding hands, and asked if we stock any practical ...8 hours ago

- Brutal Day Of Govt Cuts, Axing Support For Children And Young PeopleOranga Tamariki and Ministry of Education propose scrapping 1012 jobs ...8 hours ago

- The High Court is hearing another high-stakes immigration case. Can people be forced to assist in th...Source: The Conversation (Au and NZ) – By Sara Dehm, Senior lecturer, international migration and refugee law, University of Technology Sydney Starting today, the High Court will hear a case to decide if the government’s indefinite detention of a bisexual Iranian man is lawful, partly because he is unwilling to ...8 hours ago

- Why Australia’s Olympic funding changes might widen the gap between rich and poor sportsSource: The Conversation (Au and NZ) – By John Cairney, Head of Human Movement and Nutrition Sciences, The University of Queensland The Australian Olympic Committee (AOC) has proposed a new strategy to bolster the financial health of Olympic sports, ranging from minor sports such as table tennis to dominant codes ...8 hours ago

- Large Scale Cuts At Education Ministry Will Have Negative Impacts On Schools And ChildrenThe cuts will affect both the daily running of schools and early childhood education services, and will make support for students even more difficult to access. ...8 hours ago

- Watch live: Prime Minister Christopher Luxon in ThailandThe Prime Minister Christopher Luxon is taking questions ahead of a meeting with his Thai counterpart. ...9 hours ago

- Indigenous businesses are worth billions but we don’t know enough about themSource: The Conversation (Au and NZ) – By Michelle Evans, Associate Professor, The University of Melbourne Indigenous businesses generate about A$16 billion a year in revenue and employ more than 116,000 people – almost as many as the massive Coles retail group. But the contribution of these businesses to the ...9 hours ago

- NEW POLL: Strong Support For Inflation Adjustment Of Tax Brackets To End The Stealth TaxA new Taxpayers’ Union — Curia poll has revealed that New Zealanders – at a ratio of five to one – support inflation adjustment of income tax brackets. 67% of respondents supported inflation adjustments while just 13% were opposed. ...9 hours ago

- Watch live: Ministers announce plan to extend port permits by 20 yearsPorts are having their permits for pre-RMA activities extended so they won't need to obtain new ones before September 2026. ...9 hours ago

- Time For Associate Minister Of Education To Reveal His School Lunches Magic TrickIt’s time for him to explain how he will do this, what the consequences will be and what evidence he has that these changes will achieve the same results. ...9 hours ago

- Letter From Te Hunga Roia Maori O Aotearoa / NZ Maori Law Society Re Cabinet BreachTe Hunga Roia Māori o Aotearoa | the New Zealand Māori Law Society are concerned about recent comments made by Minister Shane Jones in respect of the Waitangi Tribunal. We consider that his comments breach the principle of the separation of powers ...9 hours ago

- Tolerate Online Abuse Or Resign: How The Law Fails Women MPsAs women MPs face social media vitriol, where are the plans to combat it? Human rights law expert Dr Cassandra Mudgway explores the global issue in a free talk. ...10 hours ago

- Inflation Data Shows Need For A Plan On Climate And PopulationData today shows headline CPI inflation at 4%, continuing the fall begun in March 2023. Rises are concentrated in particular sectors – especially services. This data also shows that that the minimum wage increase will be half the rate of inflation ...10 hours ago

- Myles Thomas: Newshub, TVNZ job cuts: We now have the worst TV in the Western worldCOMMENTARY: By Myles Thomas The announced closure of Television New Zealand’s last primetime current affairs programme seems to be the final nail in the coffin for New Zealand’s television credibility. Coming a day after the announcement of the closure of Newshub, it shows that Kiwis have the worst television and ...10 hours ago

- Woolworths chief Brad Banducci couldn’t give senators his company’s ‘return on equity’. What...Source: The Conversation (Au and NZ) – By Sean Pinder, Associate Professor, Finance , The University of Melbourne During yesterday’s senate inquiry into supermarket pricing, Greens senator Nick McKim threatened to hold outgoing Woolworths chief executive Brad Banducci in contempt for refusing to directly answer questions about the company’s profitability. ...10 hours ago

- Netflix’s Ripley is the most controversial adaptation yet – it’s also the bestPip Adams reviews the Netflix adaptation Patricia Highsmith’s famous novel, which is dividing critics. Recently, 1,000 victims of human trafficking were freed from scam factories in Myanmar. While tech billionaires live off the profits from selling the information their platforms produce, these factory workers use this same information to engage ...10 hours ago

- Let the games begin – coalition negotiations underway in HoniaraBy Koroi Hawkins, RNZ Pacific editor in Honiara Polls have opened today in Solomon Islands. “Today is polling day. Polling Station opens at 7 am and closes at 4 pm. Be at the correct polling station and be in the voting line before 4 pm,” a text message from the ...11 hours ago

- Government Spending Still Driving Cost Of Living SkywardResponding to today’s release of the latest Consumer Price Index (CPI) figures, Taxpayers’ Union Policy and Public Affairs Manager, James Ross, said: “Domestic inflation is still punishing Kiwis, with non-tradeable inflation – the aspect most ...11 hours ago

- Annual Inflation At 4.0 PercentNew Zealand's consumers price index increased 4.0 percent in the 12 months to the March 2024 quarter, according to figures released by Stats NZ today. The 4.0 percent increase follows a 4.7 percent increase in the 12 months to the December 2023 quarter. ...11 hours ago

- Review: Don’t let ‘based on a video game’ put you off FalloutA gaming novice explains why you should watch the latest big video game adaptation to hit our screens. Gamers, avert your eyes. The extent of my gaming experience is graduating from Sims University in lieu of finishing my master’s degree, and you’re about to read what I thought about the ...11 hours ago

- Two wheels, to where? Exploring the North Shore by bikeWe spoke with three people from the North Shore about why they love to cycle, and their favourite cycle routes. The North Shore of Tāmaki Makaurau has many cycleways and green parks to choose from. The biking community in the area is relatively large, and the occasional bike on the ...11 hours ago

- Job cuts at Oranga Tamariki hit more than 400 rolesMore than 400 jobs are likely to go at the children's ministry, RNZ understands. ...12 hours ago

- Women MPs Acknowledge Report Highlighting Increased Harassment Of MPs“The research reflects the real experiences of women in politics, and I would like to acknowledge the mahi by the researchers in highlighting this,” Ikaroa-Rawhiti MP Cushla Tangaere-Manuel said. ...13 hours ago

- Choice and control: the NDIS was designed to give participants choice, but mandatory registration co...Source: The Conversation (Au and NZ) – By Sam Bennett, Disability Program Director, Grattan Institute Shutterstock/Benjamin Crone Many Australians with disability feel on the edge of a precipice right now. Recommendations from the disability royal commission and the NDIS review were released late last year. Now a draft NDIS ...13 hours ago

- Introducing some of our 100 new sea friendsA scientific expedition has found 100 previously unknown New Zealand marine species. Who are these creatures from the depths of the Bounty Trough? A big lipped, dark eyed, slimy limp fish. A juicy, elongated orb with 16 little legs, four bouncing from its topside and a mouth pouting with stubby ...13 hours ago

- Is a 24-hour Home and Away channel the answer to subscription fatigue?Source: The Conversation (Au and NZ) – By Alexa Scarlata, Research Fellow, Media & Communications, RMIT University Do you find yourself endlessly scrolling through streaming channels, wondering what to watch among the hundreds (or thousands) of options? Do you worry about spending more money on yet another subscription just to ...13 hours ago