The issues surrounding Chorus get murkier and murkier.

I posted about this issue earlier and thought that if anyone should take a haircut it should be Chorus and its shareholders. It was aware that the review of copper broadband charges could result in a reduction in copper broadband charges. It also looks like it undercooked its tender deliberately so that it could maintain its market dominant position but now wants the good old taxpayer to give it more money so that it can continue to pay large dividends to shareholders many of who are from overseas.

But the Government blew the opportunity of dealing with this issue properly when John Key created something of a panic by saying that Chorus may go broke. The Government commissioned a report to check on Chorus’s viability.

The Ernst & Young report has now been released, on a balmy Saturday afternoon 11 days before Christmas. David Cunliffe thought that it was going to be released yesterday and the choice of Saturday was a cynical attempt to hide it behind the news of the no asset sales referendum.

It took me a bit of time to find a copy of the report. The Minister’s tweet announcing its release did not have a link to it and you would think that the Minister of Information and Technology would understand those linky things. A link did go up on the Beehive website but interestingly although it was dated December 14 it appears to have gone live on December 16. Amy may need a few lessons with the technology.

The report itself is somewhat dry but the politics behind it are interesting. The Government appears to be softening us up for a further grant of some sort of $250 million to Chorus.

The report accepts at face value Chorus’s announced one billion dollar funding gap. This is defined as the “cash flow required to maintain a net interest bearing debt to EBITDA target ration of 3.5 times over the period FY15 to FY20.”

Basically this reflects the reduction in charges by $11 per month of 1.1 million customers for a period of six years plus an allowance for interest. The phrasing is complex to a non economist like myself but the calculation seems straight forward.

It is not as if this should have been a surprise. The law changes were designed to change the pricing of copper broadband to a “cost plus” basis so a change was inevitable. The coming into effect of the decision was delayed to December 2014 so that Chorus could get ready for it. Even Amy Adams says that the Commerce Commission followed the statutory formula so the cries of panic seemed rather too strained.

Chorus basically does not want to wear the loss the Commerce Commission decision will cause. And despite John Key’s statement that it may go broke it seems that Chorus will be fine. It may have to cut back on dividend payments but that is life in the big city. The EY proposal is that a two year dividend holiday be instituted and this will save $290 million. If this was extended over the 6 years then the problem would be solved.

There are other proposals that EY has suggested. $400 to $450 million could be saved by “cash-flow savings initiatives”. There is debt headroom of $130 million that could be utilised. Chorus could also adopt the radical notion of changing its business model.

The report also comments on Chorus’s dividend policy. The current return on equity is 29.7%. The comparable figure for selected New Zealand infrastructure companies is 12.5% and for selected Australian infrastructure companies 11.2%. Its dividend yield was also significantly higher than that for comparable companies. The need for some reduction appears strong and this will not sell the company broke, despite Key’s assertions to the contrary.

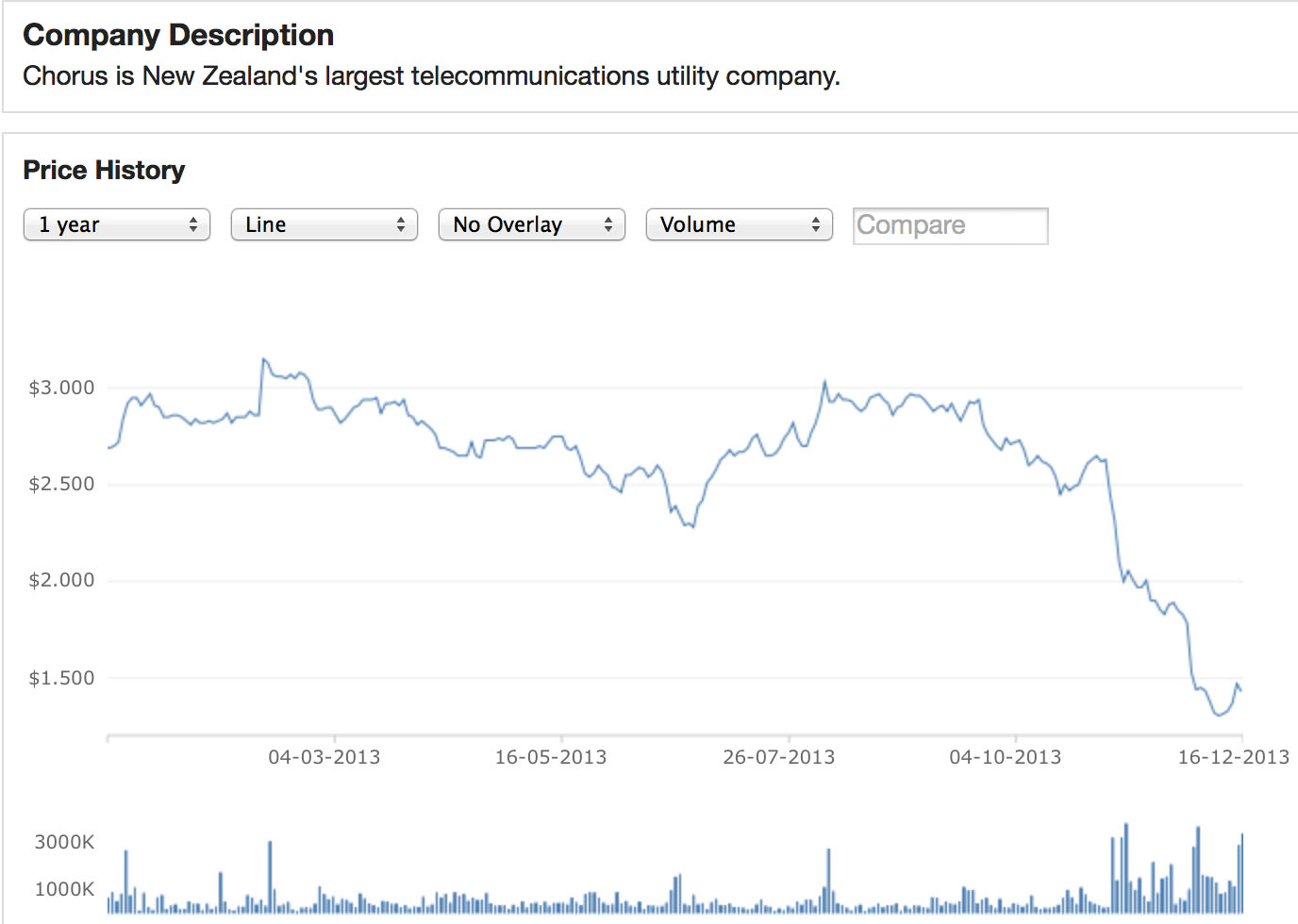

There have been some worrying aspects about the release of the report. It was dated December 12 and was presumably delivered to the Minister that day. Chorus’s share price had taken a hammering during the axe the copper tax campaign. Its shares were worth $3.03 each in August but this price sank to $1.33 on December 11. Its price surged to $1.47 on December 12 and with 3 million shares being traded there was a lot of activity. The phrase insider trading has been used to describe this activity. Although Milford Asset Management had publicly recommended Chorus shares you do get a sneaky feeling that someone in the Beehive may have had a peek at the report and then mentioned it to someone.

TUANZ certainly smells a rat. TVNZ reports:

NZX, the stock exchange operator, is declining comment on a claim by telecommunications lobbyists that there’s an emerging pattern of spikes in the Chorus share price ahead of the release of market-sensitive information from the government. The chief executive of the Telecommunications Users Association of New Zealand, Paul Brislen, cited two incidents, in August and in the last five days, where an imminent announcement from Communications Minister Amy Adams and a price spike in the telecommunications infrastructure provider’s shares were linked.

“It seems when Ms Adams makes a market-sensitive announcement, shares in Chorus move significantly beforehand but not after,” said Brislen in a statement.

The report notes that the eventual cost of copper broadband, at $34.44 per month would be lower than that for fibre optic cable which will be $37.50. Given that fibre is considerably superior to copper this is not unusual.

The earlier incident was in August when during the 7 days leading up to the Government’s announcement of a discussion paper suggesting changes to the law to help Chorus the share price went from $2.70 to $3.03. Movement in the share price after the announcement of a very generous package would have been understandable but movement before is rather odd to put it mildly.

So in typical style the Government appears to be readying itself for some more corporate largesse to a company that does not need it. And you have to wonder if TUANZ is right in its concern that some insider trading has occurred.

Powered by WPtouch Mobile Suite for WordPress

{kind=link}