Budget 2014 figures show that the housing crisis will get much, much worse under National’s do-nothing approach.

For every dollar someone uses to pay a mortgage on an average house in 2014, in 2018 a person will need $1.44 to do exactly the same thing. Pay rises will not come close to covering this.

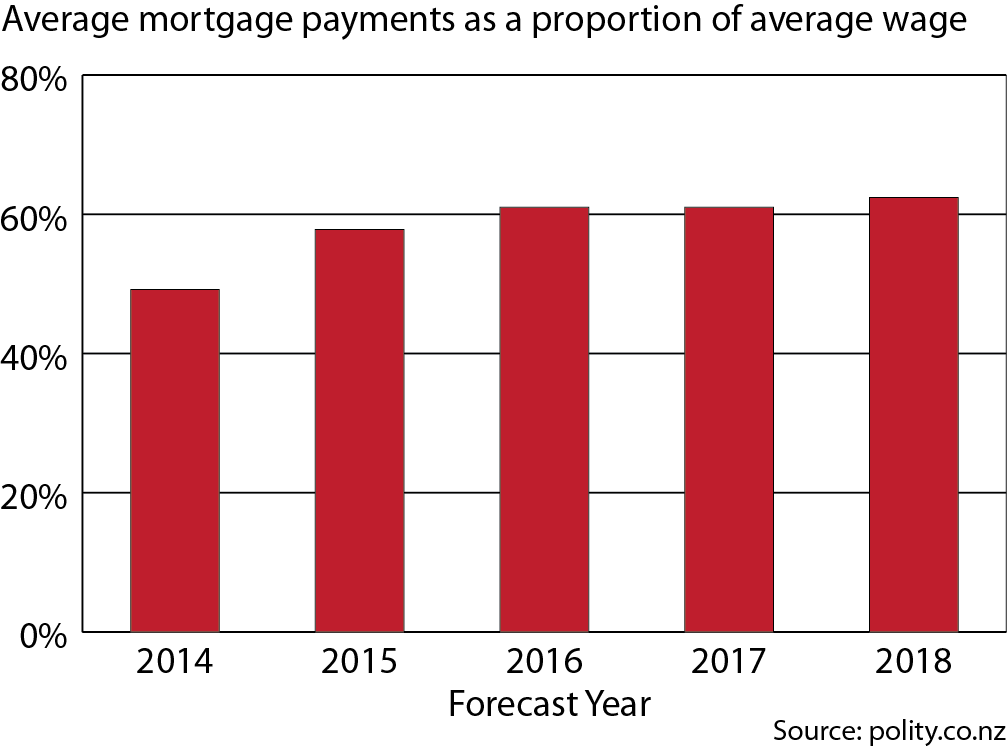

By 2018/19, it will cost 63% of the average gross full time wage to service a standard1 mortgage on an average2 home. Right now, the figure is 49%. That cost increase is shockingly high. The news is even worse in Auckland, where in 2018 a standard mortgage on an average house will cost 86% of the average New Zealand full time wage. Staggering.

And, even worse, escalating interest payments on current mortgages are set to eat up all of most mortgage-holders’ income gains over the next five years. All these New Zealanders’ standard of living will go backwards until 2018, despite a growing economy, because National is doing nothing on housing affordability.

Here is how the numbers break down (Excel here):

First home buyers

Here is a chart showing the projected cost increase for a new standard mortgage on an average home, calculated as a proportion of average full time wages:3

This huge hike in mortgage costs will kill off the dream of home ownership for tens of thousands more New Zealand families. In 2014, the median house price is around 7.7 times the average full time wage. By 2018, it will rise to be 8.0 times as much. Every time this ratio rises, more and more New Zealanders are forced to abandon home ownership. Even as this government published the figures that show how deep the crisis will get, in the Budget it did absolutely nothing to help first home buyers.

Mortgage holders

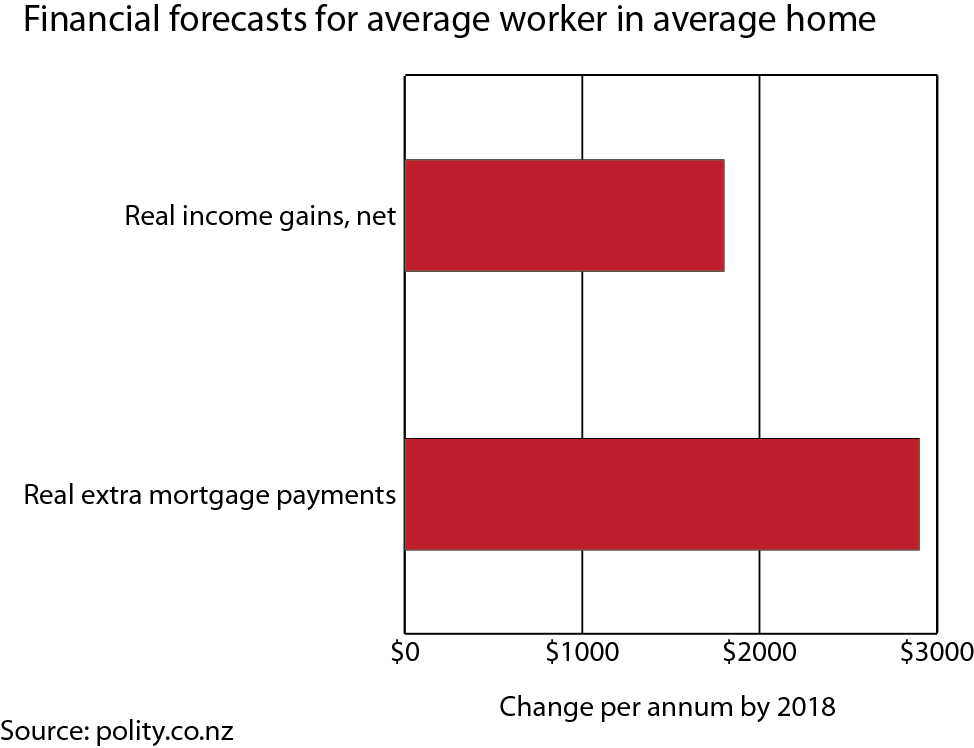

For those who do buy a home, the news isn’t any better. The soaring mortgage interest rates over the next five years could wipe out all their income gains over the period.

Real average full time earnings are projected to go from around $59,500 in 2014/15 to around $62,100 (2014 dollars) in 2018/19. The gain over the period, in real terms, is around $2,600 a year pre-tax, or about $1,800 after tax.4

But the interest rate increases will wipe out those gains entirely. A standard5 floating mortgage on a $467,000 home – the NZ median price in the first year of the forecast period – has payments that will rise from $29,700 a year in 2014 to a whopping $36,020 a year in 2018. Discounting for compound inflation, that is a real increase of around $2,900 (2014 dollars) a year, much more than an average full-time wage worker’s gains over that period.

Families in this position will go backwards in their purchasing power, even as the economy grows strongly for five years. Even families with a full-time earner and also a part-time earner will likely go backwards.6

The combined effect of this unchecked house price inflation, and steeply rising interest rates, is as damaging as it is far-reaching:

First home buyers get it in the neck as rising prices and rising interest rates combine to make home ownership even less achievable.

Current mortgage holders get it in the neck because their mortgage payments will eat up an ever increasing portion of their income over the next five years, even though mortgage payments typically fall as a proportion of income over time.

And, to top it off, renters will also get it in the neck because most of them are renting from a landlord who has a ballooning mortgage.

Housing affordability is a crisis for New Zealand, and it is set to get much, much worse unless there is significant intervention in the housing market. As we saw in yesterday’s Budget, there is no danger of any such intervention coming from National, who seem to think that reducing the building cost of new homes by around 1% will solve the crisis. They are dreaming.

At the same time, New Zealanders are facing up to a nightmare.

1. 80%, 25 year

2. Median NZ price

3. These projections use Treasury figures from the BEFU, and when other raw data is needed they use the same sources as the Treasury used in the BEFU. I am using National’s own numbers, and my calculations are available here.

4. I use real wage gains, not nominal gains, as the comparison point here because interest rate changes are not counted in CPI inflation calculations.

5. 80%, 25 year

6. Of course, families with two good incomes may or may not technically go backwards, depending on what kind of house they choose to live in. Instead, they would merely have a large majority of their income gains eaten by mortgage payments.

Powered by WPtouch Mobile Suite for WordPress

{kind=link}

{kind=link}

{kind=link}