A few weeks ago, The Economist led with this paragraph.

THE struggle has been long and arduous. But gazing across the battered economies of the rich world it is time to declare that the fight against financial chaos and deflation is won. In 2015, the IMF says, for the first time since 2007 every advanced economy will expand. Rich-world growth should exceed 2% for the first time since 2010 and America’s central bank is likely to raise its rock-bottom interest rates.

But anyone who has been through the start of a few downturns knows the feeling that is circling around the world at present. It isn’t that of successfully slaying the dragon and walking away to find the partner of your dreams. Jon Berkeley caught the mood for the Economist perfectly…

However, the global economy still faces all manner of hazards, from the Greek debt saga to China’s shaky markets. Few economies have ever gone as long as a decade without tipping into recession—America’s started growing in 2009. Sod’s law decrees that, sooner or later, policymakers will face another downturn. The danger is that, having used up their arsenal, governments and central banks will not have the ammunition to fight the next recession. Paradoxically, reducing that risk requires a willingness to keep policy looser for longer today.

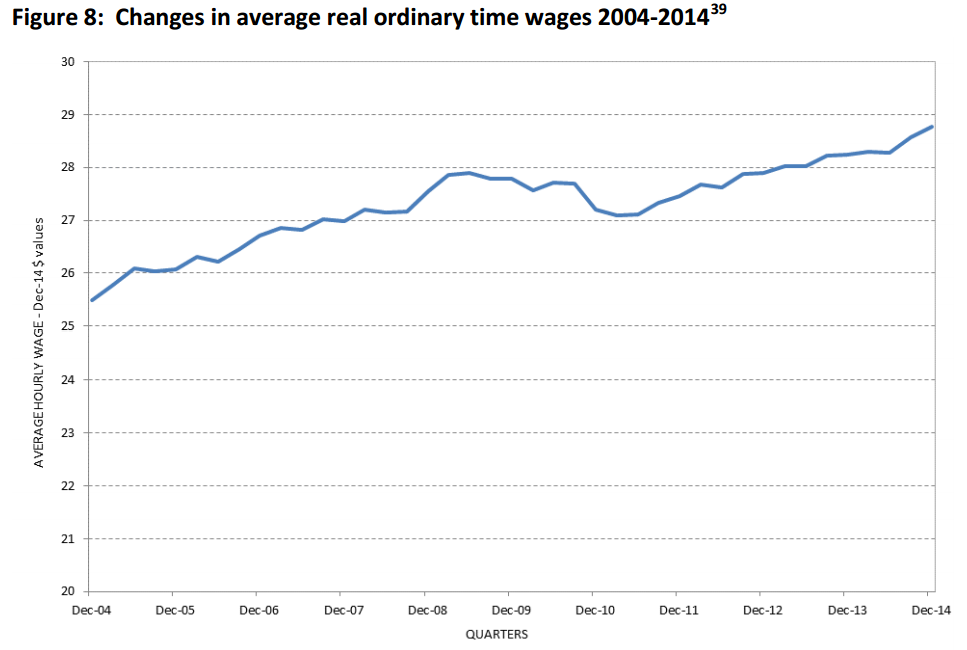

In the rich world in particular (including New Zealand), this has been a wageless recovery. For the majority of workers, they have been getting bugger all wage rises, usually less than the nominal rates of inflation and certainly less than their cost of living. The increasing prevalence of casual work like the “zero hour” contracts and unpaid “internships” is a symptom of the issue. And it is only now starting to turn in some countries.

The good news comes mainly from America, which leads the rich-world pack. Its unexpected contraction in the first quarter looks like a blip, owing a lot to factors like the weather (see article). The most recent data, including surging vehicle sales and another round of robust employment figures, show that the pace of growth is rebounding. American firms took on 280,000 new workers last month. Bosses are at last having to pay more to find the workers they need.

This is about 7 years after the global financial crisis took hold. It is much the same here. Ordinary wages took five years after the GFC before they exceeded the level reached at the GFC. See “Recent Wealth and income trends in New Zealand” from Alan Johnson at The Salvation Army. Their rise since has been somewhat constrained despite a relatively low (by European and US standards) unemployment rate.

On the cost side, the costs that the wages pay for has been kept creeping up despite the usage of saving devices. I have particularly noticed our power bill s creeping up even as we put in power saving devices that reduce what we consume.

Meanwhile looking offshore, the countries and areas that we market to or have influence on the state of our markets don’t look good. The Economist leader article nails the issue

Inevitably fragilities remain. Europe is deep in debt and dependent on exports. Japan cannot get inflation to take hold. Wage growth could quickly dent corporate earnings and valuations in America. Emerging economies, which accounted for the bulk of growth in the post-crisis years, have seen better days. The economies of both Brazil and Russia are expected to shrink this year. Poor trade data suggest that Chinese growth may be slowing faster than the government wishes.

If any of these worries causes a downturn the world will be in a rotten position to do much about it. Rarely have so many large economies been so ill-equipped to manage a recession, whatever its provenance, as our “wriggle-room” ranking makes clear (see article). Rich countries’ average debt-to-GDP ratio has risen by about 50% since 2007. In Britain and Spain debt has more than doubled. Nobody knows where the ceiling is, but governments that want to splurge will have to win over jumpy electorates as well as nervous creditors. Countries with only tenuous access to bond markets, as in the euro zone’s periphery, may be unable to launch a big fiscal stimulus.

Monetary policy is yet more cramped. The last time the Federal Reserve raised interest rates was in 2006. The Bank of England’s base rate sits at 0.5%. Records dating back to the 17th century show that, before 2009, it had never fallen below 2%; and futures prices suggest that in early 2018 it will still be only around 1.5%. That is healthy compared with the euro area and Japan, where rates in 2018 are expected to remain stuck near zero. When central banks face their next recession, in other words, they risk having almost no room to boost their economies by cutting interest rates. That would make the next downturn even harder to escape.

And in NZ, National’s over dependence on a commodity price boom in whole milk powder over the last 7 years is starting to constrain our economy.

The Economist has some good advice for policy makers world wide, but especially those in the US.

Raising rates while wages are flat and inflation is well below the central bankers’ target risks pushing economies back to the brink of deflation and precipitating the very recession they seek to avoid. When central banks have raised rates too early—as the European Central Bank did in 2011—they have done such harm that they have felt compelled to reverse course. Better to wait until wage growth is entrenched and inflation is at least back to its target level. Inflation that is a little too high is a lot less dangerous for an economy than premature rate rises are.

Indeed, the very last thing that the world needs today is to drop into another widespread recession too fast – especially from ideological idiots. Looking worldwide, what recession recovery has happened looks way too fragile to disturb much. To reduce the levels of debt that much of the developed world has incurred over the last 7 years will take a number of years of taxing solid wage growth to refill the government coffers so that they can be ready for the next recession.

Crazed conservative ideologues like Bill English wanting to give tax cuts to the rich will have to wait until they have at least got the finances ready to face the next recession. After all the watch cry of tax bracket creep beloved by the crazies of Act hardly shows up with ordinary wages like those above. Most people would prefer to have real wage rise above what they were earning nearly a decade ago.

Perhaps MP’s should just constrain their own wages to a similar rate of increase (it has been highly noticeable that they have been acting like pigs in a trough in the last seven years). It’d probably help with their sense of proportion.

Powered by WPtouch Mobile Suite for WordPress

{kind=link}