This post could be read as following on from this one in 2010. Let’s add some recent observations…

It’s now clear that our recovery from the GFC has been slowest recovery from recession in more than 50 years.

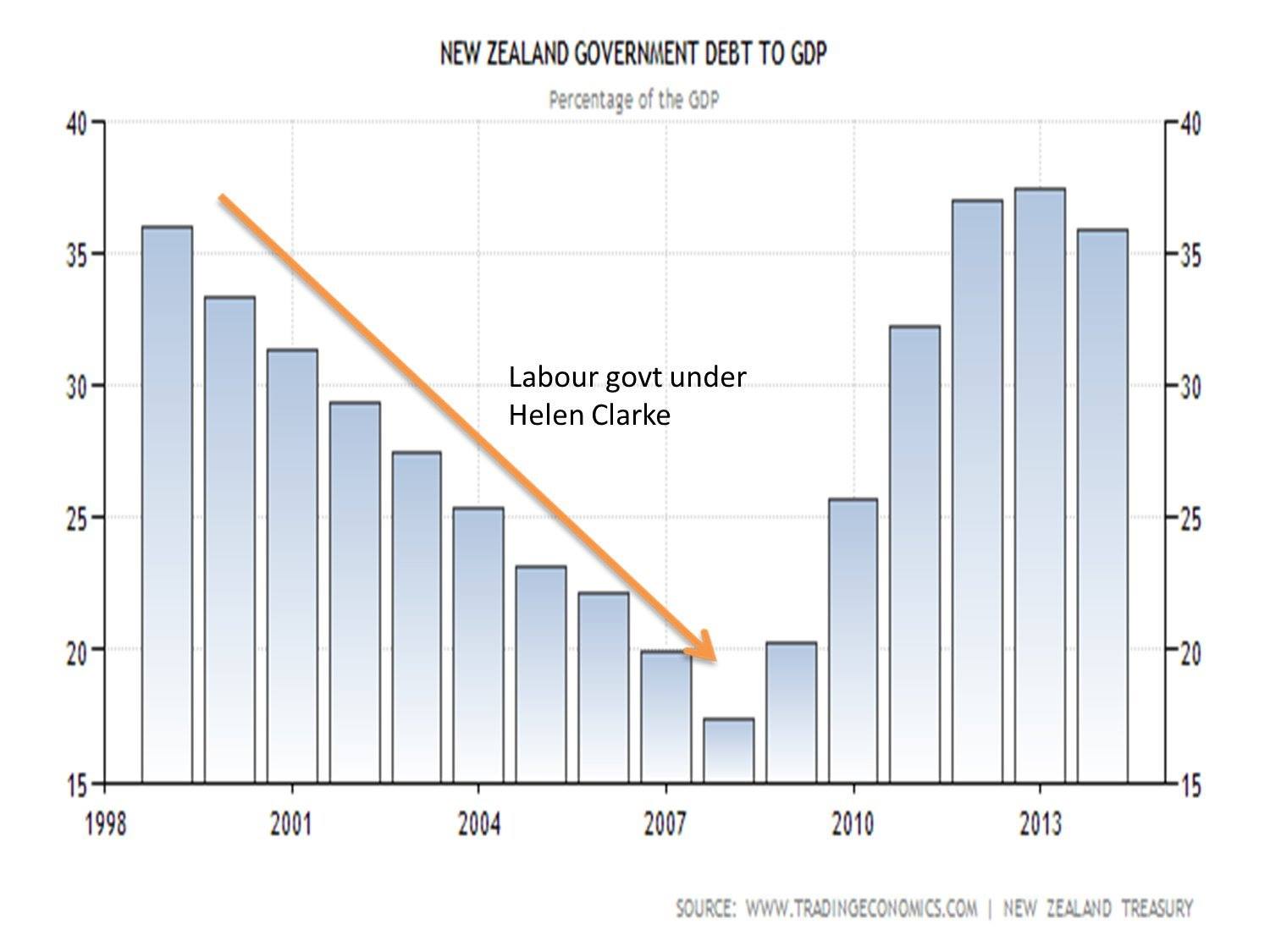

Currently we have record debt both as a country and individually, and the Cullen / Super fund is $17 billion poorer because we foolishly stopped contributions.

In a recent piece on how poorly our economy is doing:

Some snippets on New Zealand’s continuing economic underperformance

…

Successful economies, building on a sustainable footing, do so by selling more and different stuff in competition with the best the rest of the world has to offer. That doesn’t describe New Zealand at all – under this government or its predecessor.We have

• no productivity growth

• a continuing high unemployment rate

• ruinous house prices, and

• a tradables sector that has achieved no per capita growth for 15 years.

…

We currently have the worst productivity since 1996. We hardly have per-capita growth at all – the main reason our economy is “growing” is immigration:

New Zealand’s economic growth driven almost exclusively by rising population

New Zealand’s economic growth is barely keeping up with the speed at which the population is growing, amid a slowdown in the primary sector.

Official figures released on Thursday showed gross domestic product rose by 0.7 per cent in the first three months of the year, bringing annual growth to 2.8 per cent.

But while the construction industry is expanding at speed, economists said almost all of the growth was being driven by population growth, currently at a 40 year high, boosted by record immigration. …

We’re not doing anything better, we’re just have more people doing it. The only thing growing like mad is the housing bubble. In the immortal words of Bernard Hickey:

One of the most depressing aspects of all this is that it is largely self-inflicted. Decades of neoliberal policies dramatically increased inequality. This trend was somewhat softened by the last Labour government, but is back with a vengeance under National. The effects of inequality on our economy are disasterous:

How inequality made these Western countries poorer

Rising inequality holds back economic growth — according to a recent report by the Organization for Economic Co-operation and Development (OECD).

…

Here are the countries that missed out on most growth, according to the OECD:1. New Zealand: New Zealand’s economy could have grown by 44 percent between 1990 and 2010, but the country did only achieve 28 percent growth due to inequality. Hence, it lost 15.5 percentage points — more than any other country. This is particularly surprising, given that New Zealand was once considered a paradise of equality, as Max Rashbrooke, the author of a book called Inequality: A New Zealand Crisis, pointed out in the Guardian newspaper.

“New Zealand halved its top tax rate, cut benefits by up to a quarter of their value, and dramatically reduced the bargaining power – and therefore the share of national income – of ordinary workers. Thousands of people lost their jobs as manufacturing work went overseas, and there was no significant response with increased trade training or skills programs, a policy failure that is ongoing,” Rashbrooke writes in the op-ed. He also blames New Zealand for a lack of affordable homes which led to higher rents and unpaid mortgages. …

I could go on but you get the picture. The National government has made mistake after mistake after mistake. What we have is more or less a zombie economy only partially animated by immigration and a housing bubble.

Powered by WPtouch Mobile Suite for WordPress

{kind=link}