Landlords: youse are better off renting

Landlords: youse are better off renting

Written By:

- Date published:

8:43 am, July 23rd, 2008 - 31 comments

Categories: housing -

Tags:

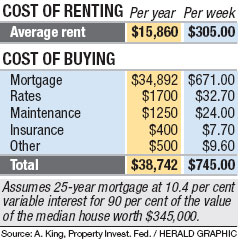

The graphic to the left was produced by the Property Investors’ Federation and was printed unquestioned in the Herald yesterday. The PIF uses the figures to claim Kiwis are better off renting. Here’s what’s wrong with them.

The graphic to the left was produced by the Property Investors’ Federation and was printed unquestioned in the Herald yesterday. The PIF uses the figures to claim Kiwis are better off renting. Here’s what’s wrong with them.

First, it’s comparing the average rent to the cost of buying a median house. Rental properties tend to be lower quality, cheaper – so are likely on average to be worth well below the national median. Comparing apples with apples would look at the rent on properties of the same value.

Secondly and most importantly, if you’re buying the house at the end of 25 years, you own a house. If you rent, at the end of 25 years you have nothing. That’s a pretty serious difference. If you buy rather than rent you might pay some more (less than the difference in the graphic though) but you end up with an asset in the end.

So, what is the Property Investors’ Federation‘s interest in trying to convince Kiwis they are better off renting? Well, as the name suggests, the PIF is a political lobby group that represents landlords – ie people who make money off others renting from them, people who obviously think that owning properties, multiple properties, is worthwhile.

Why would a group of landlords want people to think renting is better than buying?

- to decrease demand for buying houses, so PIF members can buy them more cheaply

- to increase demand for rentals, allowing PIF members to put up rents

- to undermine the demand for the Government to intervene in the housing market with a large affordable housing policy. If the Government builds lots of affordable houses, PIF members’ tenants will be able to find cheaper rentals and cheaper houses to buy. That’s good for most Kiwis, bad for the PIF landlords.

Landlord lobby group comes out with flawed figures suggesting renting is cheap just as the Government appears to be developing a housing affordability policy. Funny coincidence that.

31 comments on “Landlords: youse are better off renting ”

- Comments are now closed

Links to post

- Comments are now closed

Recent Comments

- World Domination

Just one year of loveIs better than a lifetime aloneOne sentimental moment in your armsIs like a shooting star right through my heartIt's always a rainy day without youI'm a prisoner of love inside youI'm falling apart all around you, yeahSongwriter: John Deacon.Morena folks, it feels like it’s been quite ...7 hours ago

Just one year of loveIs better than a lifetime aloneOne sentimental moment in your armsIs like a shooting star right through my heartIt's always a rainy day without youI'm a prisoner of love inside youI'm falling apart all around you, yeahSongwriter: John Deacon.Morena folks, it feels like it’s been quite ...7 hours ago - “I think I was, at that time, the only girl in Taranaki who ever wrote a line”

“It's a history of colonial ruin, not a history of colonial progress,” says Michele Leggott, of the Harris family.We’re talking about Groundwork: The Art and Writing of Emily Cumming Harris, in which she and Catherine Field-Dodgson recall a near-forgotten and fascinating life, the female speck in the history of texts.Emily’s ...12 hours ago

“It's a history of colonial ruin, not a history of colonial progress,” says Michele Leggott, of the Harris family.We’re talking about Groundwork: The Art and Writing of Emily Cumming Harris, in which she and Catherine Field-Dodgson recall a near-forgotten and fascinating life, the female speck in the history of texts.Emily’s ...12 hours ago - A Baptism in the Forest: Accepted

Hitherto, 2025 has not been great in terms of luck on the short story front (or on the personal front. Several acquaintances have sadly passed away in the last few days). But I can report one story acceptance today. In fact, it’s quite the impressive acceptance, being my second ‘professional ...1 day ago

Hitherto, 2025 has not been great in terms of luck on the short story front (or on the personal front. Several acquaintances have sadly passed away in the last few days). But I can report one story acceptance today. In fact, it’s quite the impressive acceptance, being my second ‘professional ...1 day ago - Bernard’s Saturday Soliloquy for the week to April 12

Six long stories short from our political economy in the week to Saturday, April 12:Donald Trump exploded a neutron bomb under 80 years of globalisation, but Nicola Willis said the Government would cut operational and capital spending even more to achieve a Budget surplus by 2027/28. That even tighter fiscal ...1 day ago

Six long stories short from our political economy in the week to Saturday, April 12:Donald Trump exploded a neutron bomb under 80 years of globalisation, but Nicola Willis said the Government would cut operational and capital spending even more to achieve a Budget surplus by 2027/28. That even tighter fiscal ...1 day ago - Budget 2025: delivering for whom?

On 22 May, the coalition government will release its budget for 2025, which it says will focus on "boosting economic growth, improving social outcomes, controlling government spending, and investing in long-term infrastructure.” But who, really, is this budget designed to serve? What values and visions for Aotearoa New Zealand lie ...1 day ago

On 22 May, the coalition government will release its budget for 2025, which it says will focus on "boosting economic growth, improving social outcomes, controlling government spending, and investing in long-term infrastructure.” But who, really, is this budget designed to serve? What values and visions for Aotearoa New Zealand lie ...1 day ago - The Other Side

Lovin' you has go to be (Take me to the other side)Like the devil and the deep blue sea (Take me to the other side)Forget about your foolish pride (Take me to the other side)Oh, take me to the other side (Take me to the other side)Songwriters: Steven Tyler, Jim ...1 day ago

Lovin' you has go to be (Take me to the other side)Like the devil and the deep blue sea (Take me to the other side)Forget about your foolish pride (Take me to the other side)Oh, take me to the other side (Take me to the other side)Songwriters: Steven Tyler, Jim ...1 day ago - It’s (past) time to get serious about funding Australia’s defence and security

In the week of Australia’s 3 May election, ASPI will release Agenda for Change 2025: preparedness and resilience in an uncertain world, a report promoting public debate and understanding on issues of strategic importance to ...1 day ago

In the week of Australia’s 3 May election, ASPI will release Agenda for Change 2025: preparedness and resilience in an uncertain world, a report promoting public debate and understanding on issues of strategic importance to ...1 day ago - The Downward Spiral of Arise Church: Part 4

Hi,Back in 2022 I spent a year reporting on New Zealand’s then-biggest megachurch, Arise, revealing the widespread abuse of hundreds of interns.That series led to a harrowing review (leaked by Webworm) and the resignation of its founders and leaders John and Gillian Cameron, who fled to Australia where they now ...2 days ago

Hi,Back in 2022 I spent a year reporting on New Zealand’s then-biggest megachurch, Arise, revealing the widespread abuse of hundreds of interns.That series led to a harrowing review (leaked by Webworm) and the resignation of its founders and leaders John and Gillian Cameron, who fled to Australia where they now ...2 days ago - Whatever the CCP says, regimes don’t have the rights of nations

All nation states have a right to defend themselves. But do regimes enjoy an equal right to self-defence? Is the security of a particular party-in-power a fundamental right of nations? The Chinese government is asking ...2 days ago

- Countervailing Trumpian Sense

A modest attempt to analyse Donald Trump’s tariff policies.Alfred Marshall, whose text book was still in use 40 years after he died wrote ‘every short statement about economics is misleading with the possible exception of my present one.’ (The text book is 719 pages.) It’s a timely reminder that any ...2 days ago

A modest attempt to analyse Donald Trump’s tariff policies.Alfred Marshall, whose text book was still in use 40 years after he died wrote ‘every short statement about economics is misleading with the possible exception of my present one.’ (The text book is 719 pages.) It’s a timely reminder that any ...2 days ago - Uncertainty, Hierarchy and the Dilemma of Democracy.

If nothing else, we have learned that the economic and geopolitical turmoil caused by the Trump tariff see-saw raises a fundamental issue of the human condition that extends beyond trade wars and “the markets.” That issue is uncertainty and its centrality to individual and collective life. It extends further into ...2 days ago

If nothing else, we have learned that the economic and geopolitical turmoil caused by the Trump tariff see-saw raises a fundamental issue of the human condition that extends beyond trade wars and “the markets.” That issue is uncertainty and its centrality to individual and collective life. It extends further into ...2 days ago - Strengthening South Korea’s national security by adopting the cloud

To improve its national security, South Korea must improve its ICT infrastructure. Knowing this, the government has begun to move towards cloud computing. The public and private sectors are now taking a holistic national-security approach ...2 days ago

- Workers’ Memorial Day 2025

28 April 2025 Mournfor theDead FightFor theLiving Every week in New Zealand 18 workers are killed as a consequence of work. Every 15 minutes, a worker suffers ...2 days ago

28 April 2025 Mournfor theDead FightFor theLiving Every week in New Zealand 18 workers are killed as a consequence of work. Every 15 minutes, a worker suffers ...2 days ago - Reset Pax Americana: the West needs a grand accord

The world is trying to make sense of the Trump tariffs. Is there a grand design and strategy, or is it all instinct and improvisation? But much more important is the question of what will ...2 days ago

- Poisoning The Well – It’s Not Just ACT

OPINION:Yesterday was a triumphant moment in Parliament House.The “divisive”, “disingenous”, “unfair”, “discriminatory” and “dishonest” Treaty Principles Bill, advanced by the right wing ACT Party, failed.Spectacularly.11 MP votes for (ACT).112 MP votes against (All Other Parties).As the wonderful Te Pāti Māori MP, Hana-Rāwhiti Maipi-Clarke said: We are not divided, but united.Green ...2 days ago

OPINION:Yesterday was a triumphant moment in Parliament House.The “divisive”, “disingenous”, “unfair”, “discriminatory” and “dishonest” Treaty Principles Bill, advanced by the right wing ACT Party, failed.Spectacularly.11 MP votes for (ACT).112 MP votes against (All Other Parties).As the wonderful Te Pāti Māori MP, Hana-Rāwhiti Maipi-Clarke said: We are not divided, but united.Green ...2 days ago - The Pacific Response Group is making pleasing progress but needs more buy-in

The Pacific Response Group (PRG), a new disaster coordination organisation, has operated through its first high-risk weather season. But as representatives from each Pacific military leave Brisbane to return to their home countries for the ...2 days ago

- Friday 11 April

The Treaty Principles Bill has been defeated in Parliament with 112 votes in opposition and 11 in favour, but the debate about Te Tiriti and Māori rights looks set to stay high on the political agenda. Supermarket giant Woolworths has confirmed a new operating model that Workers First say will ...2 days ago

- A few wins, for now

2 days ago

2 days ago - Aotearoa Wins!

And this is what I'm gonna doI'm gonna put a call to you'Cause I feel good tonightAnd everything's gonna beRight-right-rightI'm gonna have a good time tonightRock and roll music gonna play all nightCome on, baby, it won't take longOnly take a minute just to sing my songSongwriters: Kirk Pengilly / ...2 days ago

And this is what I'm gonna doI'm gonna put a call to you'Cause I feel good tonightAnd everything's gonna beRight-right-rightI'm gonna have a good time tonightRock and roll music gonna play all nightCome on, baby, it won't take longOnly take a minute just to sing my songSongwriters: Kirk Pengilly / ...2 days ago - Indonesia’s cyber soldiers: armed without a compass

The Indonesian military has a new role in cybersecurity but, worryingly, no clear doctrine on what to do with it nor safeguards against human rights abuses. Assignment of cyber responsibility to the military is part ...2 days ago

- Weekly Roundup 11-April-2025

Another Friday, another roundup. Autumn is starting to set in, certainly getting darker earlier but we hope you enjoy some of the stories we found interesting this week. This week in Greater Auckland On Tuesday we ran a guest post from the wonderful Darren Davis about what’s happening ...2 days ago

Another Friday, another roundup. Autumn is starting to set in, certainly getting darker earlier but we hope you enjoy some of the stories we found interesting this week. This week in Greater Auckland On Tuesday we ran a guest post from the wonderful Darren Davis about what’s happening ...2 days ago - Bernard’s Dawn Chorus & Pick ‘n’ Mix Six for Friday, April 11

Long stories shortest: The White House confirms Donald Trump’s total tariffs now on China are 145%, not 125%. US stocks slump again. Gold hits a record high. PM Christopher Luxon joins a push for a new rules-based trading system based around CPTPP and EU, rather than US-led WTO. Winston Peters ...2 days ago

Long stories shortest: The White House confirms Donald Trump’s total tariffs now on China are 145%, not 125%. US stocks slump again. Gold hits a record high. PM Christopher Luxon joins a push for a new rules-based trading system based around CPTPP and EU, rather than US-led WTO. Winston Peters ...2 days ago - The Hoon around the week to April 11

The podcast above of the weekly ‘Hoon’ webinar for paying subscribers on Thursday night features co-hosts & talking about the week’s news with regular and special guests, including: and on the week in geopolitics and climate, including Donald Trump’s shock and (partial) backflip; and,Health Coalition Aotearoa Chair ...3 days ago

- Skeptical Science New Research for Week #15 2025

Open access notables Global and regional drivers for exceptional climate extremes in 2023-2024: beyond the new normal, Minobe et al., npj Climate and Atmospheric Science: Climate records have been broken with alarming regularity in recent years, but the events of 2023–2024 were exceptional even when accounting for recent climatic trends. ...3 days ago

Open access notables Global and regional drivers for exceptional climate extremes in 2023-2024: beyond the new normal, Minobe et al., npj Climate and Atmospheric Science: Climate records have been broken with alarming regularity in recent years, but the events of 2023–2024 were exceptional even when accounting for recent climatic trends. ...3 days ago - The US harms its image in the Pacific with aid cuts and tariffs

USAID cuts and tariffs will harm the United States’ reputation in the Pacific more than they will harm the region itself. The resilient region will adjust to the economic challenges and other partners will fill ...3 days ago

- Good fucking riddance

National's racist and divisive Treaty Principles Bill was just voted down by the House, 112 to 11. Good fucking riddance. The bill was not a good-faith effort at legislating, or at starting a "constitutional conversation". Instead it was a bad faith attempt to stoke division and incite racial hatred - ...3 days ago

National's racist and divisive Treaty Principles Bill was just voted down by the House, 112 to 11. Good fucking riddance. The bill was not a good-faith effort at legislating, or at starting a "constitutional conversation". Instead it was a bad faith attempt to stoke division and incite racial hatred - ...3 days ago - The threat spectrum

Democracy watch Indonesia’s parliament passed revisions to the country’s military law, which pro-democracy and human rights groups view as a threat to the country’s democracy. One of the revisions seeks to expand the number of ...3 days ago

- Australia needs a civilian cyber reserve. State emergency services are the model

Australia should follow international examples and develop a civilian cyber reserve as part of a whole-of-society approach to national defence. By setting up such a reserve, the federal government can overcome a shortage of expertise ...3 days ago

- Drawn

A ballot for three Member's Bills was held today, and the following bills were drawn: Life Jackets for Children and Young Persons Bill (Cameron Brewer) Sale and Supply of Alcohol (Restrictions on Issue of Off-Licences and Low and No Alcohol Products) Amendment Bill (Mike Butterick) Crown ...3 days ago

- Thursday 10 April

Te Whatu Ora is proposing to slash jobs from a department that brings in millions of dollars a year and ensures safety in hospitals, rest homes and other community health providers. The Treaty Principles Bill is back in Parliament this evening and is expected to be voted down by all parties, ...3 days ago

- Paying For Small Indignities

Hi,The piece I wrote last week about the chances of being rounded up and evicted (and/or detained) by the United States seems more… pressing.To be clear: antisemitism is fucking horrible — and in that same breath I also wonder what today’s statement from The Department of Homeland security means for ...3 days ago

Hi,The piece I wrote last week about the chances of being rounded up and evicted (and/or detained) by the United States seems more… pressing.To be clear: antisemitism is fucking horrible — and in that same breath I also wonder what today’s statement from The Department of Homeland security means for ...3 days ago - Joint naval exercises with Russia undermine Indonesia’s commitment to international law

Indonesian President Prabowo Subianto has repeatedly asserted the country’s commitment to a non-aligned foreign policy. But can Indonesia still credibly claim neutrality while tacitly engaging with Russia? Holding an unprecedented bilateral naval drills with Moscow ...3 days ago

- Wednesday 9 April

The NZCTU have launched a new policy programme and are calling on political parties to adopt bold policies in the lead up to the next election. The Government is scrapping the 30-day rule that automatically signs an employee up to the collective agreement when they sign on to a new ...3 days ago

- Anticipating what Trump wants: Taiwan puts money in America first

Taiwan’s President Lai Ching-te must have been on his toes. The island’s trade and defence policy has snapped into a new direction since US President Donald Trump took office in January. The government was almost ...3 days ago

- Auckland’s Big Easter Rail Shutdown

Auckland’s ongoing rail pain will intensify again from this weekend as Kiwirail shut down the network for two weeks as part of their push to get the network ready for the City Rail Link. KiwiRail will progress upgrade and renewal projects across Auckland’s rail network over the Easter holiday period ...3 days ago

- Renewables allow us to pay less, not twice

This is a re-post from The Electrotech Revolution by Daan Walter Last week, UK Conservative Party leader Kemi Badenoch took the stage to advocate for slowing the rollout of renewables, arguing that they ultimately lead to higher costs: “Huge amounts are being spent on switching round how we distribute electricity ...3 days ago

- Refusing to Disappear

That there, that's not meI go where I pleaseI walk through wallsI float down the LiffeyI'm not hereThis isn't happeningI'm not hereI'm not hereSongwriters: Philip James Selway / Jonathan Richard Guy Greenwood / Edward John O'Brien / Thomas Edward Yorke / Colin Charles Greenwood.I had mixed views when the first ...3 days ago

That there, that's not meI go where I pleaseI walk through wallsI float down the LiffeyI'm not hereThis isn't happeningI'm not hereI'm not hereSongwriters: Philip James Selway / Jonathan Richard Guy Greenwood / Edward John O'Brien / Thomas Edward Yorke / Colin Charles Greenwood.I had mixed views when the first ...3 days ago - Bernard’s Dawn Chorus & Pick ‘n’ Mix Six

(A note to subscribers: I’m going to keep these daily curated news updates shorter in future to ensure an earlier and more regular delivery. Expect this format and delivery around 7 am Monday to Friday from now on. My apologies for not delivering yesterday. There was too much news… This ...3 days ago

(A note to subscribers: I’m going to keep these daily curated news updates shorter in future to ensure an earlier and more regular delivery. Expect this format and delivery around 7 am Monday to Friday from now on. My apologies for not delivering yesterday. There was too much news… This ...3 days ago - Gordon Campbell On Marketing The Military Threat Posed By China

As Donald Trump zigs and zags on tariffs and trashes America’s reputation as a safe and stable place to invest, China has a big gun that it could bring to this tariff knife fight. Behind Japan, China has the world’s second largest holdings of American debt. As a huge US ...4 days ago

As Donald Trump zigs and zags on tariffs and trashes America’s reputation as a safe and stable place to invest, China has a big gun that it could bring to this tariff knife fight. Behind Japan, China has the world’s second largest holdings of American debt. As a huge US ...4 days ago - Seabed sensors and mapping: what China’s survey ship could be up to

Civilian exploration may be the official mission of a Chinese deep-sea research ship that sailed clockwise around Australia over the past week and is now loitering west of the continent. But maybe it’s also attending ...4 days ago

- South Korea must move beyond partisan division to tackle security threats

South Korea’s internal political instability leaves it vulnerable to rising security threats including North Korea’s military alliance with Russia, China’s growing regional influence and the United States’ unpredictability under President Donald Trump. South Korea needs ...4 days ago

- Billionaire Bust-Ups

Here are 5 updates that you may be interested in today:Speed kills and costs - so why does National want more of it?James (Jim) Grenon Board Takeover Gets Shaky - As Canadian Calls An Australian Shareholder a “Flake” Billionaire Bust-ups -The World’s Richest Men Are UncomfortableOver 3,500 Australian doctors on ...4 days ago

Here are 5 updates that you may be interested in today:Speed kills and costs - so why does National want more of it?James (Jim) Grenon Board Takeover Gets Shaky - As Canadian Calls An Australian Shareholder a “Flake” Billionaire Bust-ups -The World’s Richest Men Are UncomfortableOver 3,500 Australian doctors on ...4 days ago - Member’s Day

Today is a Member's Day, and its all first readings. First up is Laura McClure's Employment Relations (Termination of Employment by Agreement) Amendment Bill, followed by Carl Bates' Juries (Age of Excusal) Amendment Bill, Adrian Rurawhe's Employment Relations (Collective Agreements in Triangular Relationships) Amendment Bill and then Kieran McAnulty's Sale ...4 days ago

- Australia’s cyber strategy needs a vulnerability disclosure upgrade

Australia is in a race against time. Cyber adversaries are exploiting vulnerabilities faster than we can identify and patch them. Both national security and economic considerations demand policy action. According to IBM’s Data Breach Report, ...4 days ago

- The Comparative Notebook on Trump’s Tariffs.

The ever brilliant Kate Nicholls has kindly agreed to allow me to re-publish her substack offering some under-examined backdrop to Trump’s tariff madness. The essay is not meant to be a full scholarly article but instead an insight into the thinking (if that is the correct word) behind the current ...4 days ago

- Humanitarian assistance in the Pacific should be led by Pacific countries

In the Pacific, the rush among partner countries to be seen as the first to assist after disasters has become heated as part of ongoing geopolitical contest. As partners compete for strategic influence in the ...4 days ago

- Tariff madness and monetary policy

We’ve seen this morning the latest step up in the Trump-initiated trade war, with the additional 50 per cent tariffs imposed on imports from China. If the tariff madness persists – but in fact even if were wound back in some places (eg some of the particularly absurd tariffs on ...4 days ago

We’ve seen this morning the latest step up in the Trump-initiated trade war, with the additional 50 per cent tariffs imposed on imports from China. If the tariff madness persists – but in fact even if were wound back in some places (eg some of the particularly absurd tariffs on ...4 days ago - Weak

Weak as I am, no tears for youWeak as I am, no tears for youDeep as I am, I'm no one's foolWeak as I amSongwriters: Deborah Ann Dyer / Richard Keith Lewis / Martin Ivor Kent / Robert Arnold FranceMorena.

Weak as I am, no tears for youWeak as I am, no tears for youDeep as I am, I'm no one's foolWeak as I amSongwriters: Deborah Ann Dyer / Richard Keith Lewis / Martin Ivor Kent / Robert Arnold FranceMorena. This morning, I couldn’t settle on a single topic. Too ... 4 days ago

This morning, I couldn’t settle on a single topic. Too ... 4 days ago - Getting Cross with AT’s awful last minute re-designs of Project K

A few weeks ago, I wrote a post extensively detailing the scandal of what happened with the Upper Mercury Lane part of the Karanga-a-Hape Station precinct integration project (also known by its cool title, Project K). It was a prime example of Auckland Transport’s habitual failure to follow through on ...4 days ago

- Climate risks to security in the Indo-Pacific: Indonesia in 2035

Australian policy makers are vastly underestimating how climate change will disrupt national security and regional stability across the Indo-Pacific. A new ASPI report assesses the ways climate impacts could threaten Indonesia’s economic and security interests ...4 days ago

- Brace position

So here we are in London again because we’re now at the do-it-while-you-still-can stage of life. More warm wide-armed hugs, more long talks and long walks and drinks in lovely old pubs with our lovely daughter.And meanwhile the world is once more in one of its assume-the-brace-position stages.We turned on ...4 days ago

So here we are in London again because we’re now at the do-it-while-you-still-can stage of life. More warm wide-armed hugs, more long talks and long walks and drinks in lovely old pubs with our lovely daughter.And meanwhile the world is once more in one of its assume-the-brace-position stages.We turned on ...4 days ago - To Dire Wolf Or Not To Dire Wolf?

Hi,Back in September of 2023, I got pitched an interview:David -Thanks for the quick response to the DM! Means the world. Re-stating some of the DM below for your team’s reference -I run a business called Animal Capital - we are a venture capital fund advised by Noah Beck, Paris ...5 days ago

Hi,Back in September of 2023, I got pitched an interview:David -Thanks for the quick response to the DM! Means the world. Re-stating some of the DM below for your team’s reference -I run a business called Animal Capital - we are a venture capital fund advised by Noah Beck, Paris ...5 days ago - A Bit Of Nuance Would Be Nice: Some Thoughts on the Trump Tariffs

I didn’t want to write about this – but, alas, the 2020s have forced my hand. I am going to talk about the Trump Tariffs… and in the process probably irritate nearly everyone. You see, alone on the Internet, I am one of those people who think we need a ...5 days ago

I didn’t want to write about this – but, alas, the 2020s have forced my hand. I am going to talk about the Trump Tariffs… and in the process probably irritate nearly everyone. You see, alone on the Internet, I am one of those people who think we need a ...5 days ago - No, it’s not new. Russia and China have been best buddies for decades

Maybe people are only just beginning to notice the close alignment of Russia and China. It’s discussed as a sudden new phenomenon in world affairs, but in fact it’s not new at all. The two ...5 days ago

- The dishonest crown

The High Court has just ruled that the government has been violating one of the oldest Treaty settlements, the Sealord deal: The High Court has found the Crown has breached one of New Zealand's oldest Treaty Settlements by appropriating Māori fishing quota without compensation. It relates to the 1992 ...5 days ago

- Middle Arm project: the infrastructure enabler for Northern Territory development

Darwin’s proposed Middle Arm Sustainable Development Precinct is set to be the heart of a new integrated infrastructure network in the Northern Territory, larger and better than what currently exists in northern Australia. However, the ...5 days ago

- Grooming us for identity theft

5 days ago

- As tensions grow, an Australian AI safety institute is a no-brainer

Australia needs to deliver its commitment under the Seoul Declaration to create an Australian AI safety, or security, institute. Australia is the only signatory to the declaration that has yet to meet its commitments. Given ...5 days ago

- Hine Ruhi (Slice Of Heaven)

Ko kōpū ka rere i te paeMe ko Hine RuhiTīaho mai tō arohaMe ko Hine RuhiDa da da ba du da da ba du da da da ba du da da da da da daDa da da ba du da da ba du da da da ba du da da ...5 days ago

Ko kōpū ka rere i te paeMe ko Hine RuhiTīaho mai tō arohaMe ko Hine RuhiDa da da ba du da da ba du da da da ba du da da da da da daDa da da ba du da da ba du da da da ba du da da ...5 days ago - ‘We can afford more drones, but not more homes’

Army, Navy and AirForce personnel in ceremonial dress: an ongoing staffing exodus means we may get more ships, drones and planes but not have enough ‘boots on the ground’ to use them. Photo: Lynn GrievesonLong stories short in Aotearoa’s political economy this morning: PM Christopher Luxon says the Government can ...5 days ago

Army, Navy and AirForce personnel in ceremonial dress: an ongoing staffing exodus means we may get more ships, drones and planes but not have enough ‘boots on the ground’ to use them. Photo: Lynn GrievesonLong stories short in Aotearoa’s political economy this morning: PM Christopher Luxon says the Government can ...5 days ago - Oliver’s struggle: a case study in the frustration of trying to join the ADF

If you’re a qualified individual looking to join the Australian Army, prepare for a world of frustration over the next 12 to 18 months. While thorough vetting is essential, the inefficiency of the Australian Defence ...5 days ago

- NZD Freefall, Winston Peters Linked To Green Party Attack Ads & More

I’ve inserted a tidbit and rumours section1. Colonoscopy wait times increase, procedures drop under NationalWait times for urgent, non-urgent and surveillance colonoscopies all progressively worsened last year. Health NZ data shows the total number of publicly-funded colonoscopies dropped by more than 7 percent.Health NZ chief medical officer Helen Stokes-Lampard blamed ...5 days ago

I’ve inserted a tidbit and rumours section1. Colonoscopy wait times increase, procedures drop under NationalWait times for urgent, non-urgent and surveillance colonoscopies all progressively worsened last year. Health NZ data shows the total number of publicly-funded colonoscopies dropped by more than 7 percent.Health NZ chief medical officer Helen Stokes-Lampard blamed ...5 days ago - Tuesday 8 April

Three billion dollars has been wiped off the value of New Zealand’s share market as the rout of global financial markets caught up with the local market. A Sāmoan national has been sentenced for migrant exploitation and corruption following a five-year investigation that highlights the serious consequences of immigration fraud ...5 days ago

- Wherefore now with Kiwirail

This is a guest post by Darren Davis. It originally appeared on his excellent blog, Adventures in Transitland, which we encourage you to check out. It is shared by kind permission. Rail Network Investment Plan quietly dropped While much media attention focused on the 31st March 2025 announcement that the replacement Cook ...5 days ago

- More unneeded officers, more military influence. Indonesia’s law revision is a mistake

Amendments to Indonesia’s military law risk undermining civilian supremacy and the country’s defence capabilities. Passed by the House of Representatives on 20 March, the main changes include raising the retirement age and allowing military officers ...5 days ago

- Gordon Campbell On Peter Dutton’s Fading Election Prospects.

So New Zealand is about to spend $12 billion on our defence forces over the next four years – with $9 million of it being new money that is not being spent on pressing needs here at home. Somehow this lavish spend-up on Defence is “affordable,” says PM Christopher Luxon, ...6 days ago

- A letter to America from an appreciative ally

Donald Trump’s philosophy about the United States’ place in the world is historically selfish and will impoverish his country’s spirit. While he claimed last week to be ‘liberating’ Americans from the exploiters and freeloaders who’ve ...6 days ago

- Myanmar’s scam centres demand ASEAN-Australia collaboration

China’s crackdown on cyber-scam centres on the Thailand-Myanmar border may cause a shift away from Mandarin, towards English-speaking victims. Scammers also used the 28 March earthquake to scam international victims. Australia, with its proven capabilities ...6 days ago

- The return of dirty politics

At the 2005 election campaign, the National Party colluded with a weirdo cult, the Exclusive Brethren, to run a secret hate campaign against the Greens. It was the first really big example of the rich using dark money to interfere in our democracy. And unfortunately, it seems that they're trying ...6 days ago

- Our MOOC Denial101x has run its course

Many of you will know that in collaboration with the University of Queensland we created and ran the massive open online course (MOOC) "Denial101x - Making sense of climate science denial" on the edX platform. Within nine years - between April 2015 and February 2024 - we offered 15 runs ...6 days ago

- In trade, nothing can replace the US consumer. Still, Asian countries look to each other

How will the US assault on trade affect geopolitical relations within Asia? Will nations turn to China and seek protection by trading with each other? The happy snaps a week ago of the trade ministers ...6 days ago

- Why Did Police Clear Brian Tamaki Of All Charges?

I mentioned this on Friday - but thought it deserved some emphasis.Auckland Waitematā District Commander Superintendent Naila Hassan has responded to Countering Hate Speech Aotearoa, saying police have cleared Brian Tamaki of all incitement charges relating to the Te Atatu library rainbow event assault.Hassan writes:..There is currently insufficient evidence to ...6 days ago

I mentioned this on Friday - but thought it deserved some emphasis.Auckland Waitematā District Commander Superintendent Naila Hassan has responded to Countering Hate Speech Aotearoa, saying police have cleared Brian Tamaki of all incitement charges relating to the Te Atatu library rainbow event assault.Hassan writes:..There is currently insufficient evidence to ...6 days ago - Reviewing the intelligence reviews (so far)

With the report of the recent intelligence review by Heather Smith and Richard Maude finally released, critics could look on and wonder: why all the fuss? After all, while the list of recommendations is substantial, ...6 days ago

- Healthy Beginnings, Hopeful Futures

Well, I don't know if I'm readyTo be the man I have to beI'll take a breath, I'll take her by my sideWe stand in awe, we've created lifeWith arms wide open under the sunlightWelcome to this place, I'll show you everythingSongwriters: Scott A. Stapp / Mark T. Tremonti.Today is ...6 days ago

Well, I don't know if I'm readyTo be the man I have to beI'll take a breath, I'll take her by my sideWe stand in awe, we've created lifeWith arms wide open under the sunlightWelcome to this place, I'll show you everythingSongwriters: Scott A. Stapp / Mark T. Tremonti.Today is ...6 days ago - Monday 7 April

Staff at Kāinga Ora are expecting details of another round of job cuts, with the Green Party claiming more than 500 jobs are set to go. The New Zealand Defence Force has made it easier for people to apply for a job in a bid to get more boots on ...6 days ago

- Release: Students struggling as Govt sits on hands

The Government is continuing to sit on its hands as students struggle to pay rent due to delays with StudyLink. ...2 days ago

The Government is continuing to sit on its hands as students struggle to pay rent due to delays with StudyLink. ...2 days ago - Release: More must be done to stop children going hungry

More children are going hungry and statistics showing children in material hardship continue to get worse. ...2 days ago

- Greens continue to call for Pacific Visa Waiver

The Green Party recognises the extension of visa allowances for our Pacific whānau as a step in the right direction but continues to call for a Pacific Visa Waiver. ...2 days ago

The Green Party recognises the extension of visa allowances for our Pacific whānau as a step in the right direction but continues to call for a Pacific Visa Waiver. ...2 days ago - More children going hungry under Coalition govt

The Government yesterday released its annual child poverty statistics, and by its own admission, more tamariki across Aotearoa are now living in material hardship. ...2 days ago

- Release: Longer wait for treatment under National

New Zealanders have waited longer to get an appointment with a specialist and to get elective surgery under the National Government. ...2 days ago

- Ka mate te Pire- Ka ora te mana o Te Tiriti o Waitangi me te iwi Māori

Today, Te Pāti Māori join the motu in celebration as the Treaty Principles Bill is voted down at its second reading. “From the beginning, this Bill was never welcome in this House,” said Te Pāti Māori Co-Leader, Rawiri Waititi. “Our response to the first reading was one of protest: protesting ...3 days ago

- Chris Hipkins speech: Treaty Principles Bill second reading

Normally, when I rise in this House to speak on a bill, I say it's a great privilege to speak on the bill. That is not the case today. ...3 days ago

- Release: End to the Treaty Principles Bill, but challenges remain ahead for Aotearoa

Ka mate te pire I te rā neiThe bill dies today ...3 days ago

- Ka mate te Pire, ka ora Te Tiriti o Waitangi – Treaty Principles Bill dead, Te Tiriti o Waitangi m...

The Green Party is proud to have voted down the Coalition Government’s Treaty Principles Bill, an archaic piece of legislation that sought to attack the nation’s founding agreement. ...3 days ago

- Member’s Bill an opportunity for climate action

A Member’s Bill in the name of Green Party MP Julie Anne Genter which aims to stop coal mining, the Crown Minerals (Prohibition of Mining) Amendment Bill, has been pulled from Parliament’s ‘biscuit tin’ today. ...3 days ago

- Release: Bill to make trading laws fairer passes first hurdle

Labour MP Kieran McAnulty’s Members Bill to make the law simpler and fairer for businesses operating on Easter, Anzac and Christmas Days has passed its first reading after a conscience vote in Parliament. ...3 days ago

- Release: Reserve Bank acts while Govt shrugs

Nicola Willis continues to sit on her hands amid a global economic crisis, leaving the Reserve Bank to act for New Zealanders who are worried about their jobs, mortgages, and KiwiSaver. ...4 days ago

- Release: Property Law Amendment Bill pulled from ballot

A Bill to protect first home buyers and others from bad faith property vendors has been drawn from the Member’s Ballot. ...4 days ago

- Release: More children at risk of losing family connections

Karen Chhour is proposing to scrap Oranga Tamariki targets which aim to connect more children under state care with family and their culture. ...4 days ago

- Release: David Parker made a difference – Hipkins

The Labour Leader today acknowledged and celebrated David Parker’s 23-year contribution to the Labour Party and to Parliament. ...5 days ago

- Release: David Parker to step down from Parliament

Long-serving Labour MP and former Minister David Parker has today announced his intention to leave Parliament. ...5 days ago

- Release: Flaws in Govt’s climate strategy will cost us money

The Government’s plan to achieve our climate goals falls short, and will cost New Zealanders money and jobs. ...6 days ago

- Green Party differing view on the Treaty Principles Bill

Read the Green Party's differing view on the Treaty Principles Bill, prepared by Tamatha Paul. ...6 days ago

- Te Pāti Māori Urges Governor-General to Block Repeal of 7AA

Today, the Oranga Tamariki (Repeal of Section 7AA) Amendment Bill has passed its third and final reading, but there is one more stage before it becomes law. The Governor-General must give their ‘Royal assent’ for any bill to become legally enforceable. This means that, even if a bill gets voted ...1 week ago

- Release: Abortion care quietly shelved amid staff shortage

Abortion care at Whakatāne Hospital has been quietly shelved, with patients told they will likely have to travel more than an hour to Tauranga to get the treatment they need. ...1 week ago

- Release: Govt guts Kāinga Ora, third of workforce under axe

The gutting of Kāinga Ora shows public housing is not a priority for this Government as it removes a third of the roles at the housing agency. ...1 week ago

- Release: Thousands of submissions excluded from Treaty Principles Bill report

Thousands of New Zealanders’ submissions are missing from the official parliamentary record because the National-dominated Justice Select Committee has rushed work on the Treaty Principles Bill. ...1 week ago

- Release: Uncertainty remains over the impact of tariffs

Today’s announcement of 10 percent tariffs for New Zealand goods entering the United States is disappointing for exporters and consumers alike, with the long-lasting impact on prices and inflation still unknown. ...1 week ago

- Release: Worst February for building consents in over a decade

The National Government’s choices have contributed to a slow-down in the building sector, as thousands of people have lost their jobs in construction. ...2 weeks ago

- Release: Labour supports Willie Apiata’s selfless act

Willie Apiata’s decision to hand over his Victoria Cross to the Minister for Veterans is a powerful and selfless act, made on behalf of all those who have served our country. ...2 weeks ago

- Te Pāti Māori MPs Denied Fundamental Rights in Privileges Committee Hearing

The Privileges Committee has denied fundamental rights to Debbie Ngarewa-Packer, Rawiri Waititi and Hana-Rawhiti Maipi-Clarke, breaching their own standing orders, breaching principles of natural justice, and highlighting systemic prejudice and discrimination within our parliamentary processes. The three MPs were summoned to the privileges committee following their performance of a haka ...2 weeks ago

- Release: Govt health and safety changes put workers at risk

Changes to New Zealand’s health and safety laws will strip back key protections for small businesses and put working Kiwis at greater risk. ...2 weeks ago

- Release: Kiwis worse off this April thanks to Govt choices

April 1 used to be a day when workers could count on a pay rise with stronger support for those doing it tough, but that’s not the case under this Government. ...2 weeks ago

- Release: Three more years for Interislander ferries

Winston Peters is shopping for smaller ferries after Nicola Willis torpedoed the original deal, which would have delivered new rail enabled ferries next year. ...2 weeks ago

- Release: Myanmar junta must stop the airstrikes

The Government should work with other countries to press the Myanmar military regime to stop its bombing campaign especially while the country recovers from the devastating earthquake. ...2 weeks ago

- Release: National failing to deliver on supermarkets

National is paying lip service to its promises to bring down the cost of living, failing to make any meaningful change in the grocery sector. ...2 weeks ago

- Release: Labour backs farmers’ call for better process on GE

Labour shares farmers’ concerns that the Gene Technology Bill is moving too fast. ...2 weeks ago

- Release: Bar still too high for small mental health providers

Small mental health providers will still be locked out of co-funding from the Mental Health Innovation Fund despite a lower threshold. ...2 weeks ago

- Greens call for Govt to scrap proposed ECE changes

The Green Party is calling for the Government to scrap proposed changes to Early Childhood Care, after attending a petition calling for the Government to ‘Put tamariki at the heart of decisions about ECE’. ...2 weeks ago

- NZ First Introduces Bill That Gives Democracy Back To The People

New Zealand First has introduced a Member’s Bill today that will remove the power of MPs conscience votes and ensure mandatory national referendums are held before any conscience issues are passed into law. “We are giving democracy and power back to the people”, says New Zealand First Leader Winston Peters. ...2 weeks ago

New Zealand First has introduced a Member’s Bill today that will remove the power of MPs conscience votes and ensure mandatory national referendums are held before any conscience issues are passed into law. “We are giving democracy and power back to the people”, says New Zealand First Leader Winston Peters. ...2 weeks ago - Speech: Navigating the New World (Dis)order in Turbulent Times

Welcome to members of the diplomatic corp, fellow members of parliament, the fourth estate, foreign affairs experts, trade tragics, ladies and gentlemen. ...2 weeks ago

- Te Pāti Māori Call for Mandatory Police Body Cameras

In recent weeks, disturbing instances of state-sanctioned violence against Māori have shed light on the systemic racism permeating our institutions. An 11-year-old autistic Māori child was forcibly medicated at the Henry Bennett Centre, a 15-year-old had his jaw broken by police in Napier, kaumātua Dean Wickliffe went on a hunger ...2 weeks ago

- Release: Kiwis lose faith in job market

Confidence in the job market has continued to drop to its lowest level in five years as more New Zealanders feel uncertain about finding work, keeping their jobs, and getting decent pay, according to the latest Westpac-McDermott Miller Employment Confidence Index. ...3 weeks ago

- ER Report: A Roundup of Significant Articles on EveningReport.nz for April 13, 2025

ER Report: Here is a summary of significant articles published on EveningReport.nz on April 13, 2025. ‘Trump fatigue’ is putting Kiwis off the news, with trust in media still low – new reportSource: The Conversation (Au and NZ) – By Merja Myllylahti, Senior Lecturer, Co-Director Research Centre for Journalism, Media ...3 hours ago

ER Report: Here is a summary of significant articles published on EveningReport.nz on April 13, 2025. ‘Trump fatigue’ is putting Kiwis off the news, with trust in media still low – new reportSource: The Conversation (Au and NZ) – By Merja Myllylahti, Senior Lecturer, Co-Director Research Centre for Journalism, Media ...3 hours ago - Winston Peters says talk of ‘trade war’ is ‘hysterical’, ‘short-sighte...

The foreign minister has taken another veiled swing at the prime minister's phone call to world leaders over US tariffs. ...7 hours ago

The foreign minister has taken another veiled swing at the prime minister's phone call to world leaders over US tariffs. ...7 hours ago - ‘Trump fatigue’ is putting Kiwis off the news, with trust in media still low – new report

Source: The Conversation (Au and NZ) – By Merja Myllylahti, Senior Lecturer, Co-Director Research Centre for Journalism, Media & Democracy, Auckland University of Technology Getty Images The news media is doing its best to keep everyone up to speed with the pace of Donald Trump’s radical changes to the ...9 hours ago

- An Ode to .. Admiral Judith

War and PeaceMinister of Peace, Lady Crusher of Oravida,accesorised with an ammo belt and camouflage face paint, addresses the press conference.The two remaining Scribes who still have jobs huddle in the front row.“We are preparing for peace!,” barks Admiraless Crusher.“To whom do we go to peace against?,” asks a Scribe.“Our ...12 hours ago

War and PeaceMinister of Peace, Lady Crusher of Oravida,accesorised with an ammo belt and camouflage face paint, addresses the press conference.The two remaining Scribes who still have jobs huddle in the front row.“We are preparing for peace!,” barks Admiraless Crusher.“To whom do we go to peace against?,” asks a Scribe.“Our ...12 hours ago - Anti-women views aren’t confined to the manosphere

Opinion: Jamie whimpers for his dad, wets his pants and looks frightened and bewildered in the opening scenes of Adolescence. Just as we’d imagine a little 13-year-old boy might react to a swarm of masked, helmeted, armed police confronting him in his bed in the early morning. A vulnerable and ...12 hours ago

- Health workers call for NZ government to join global demands for ambulance massacre inquiry

Asia Pacific Report Health workers spoke out at a rally condemning Israel’s genocide in Gaza and the latest atrocity against Palestinian aid workers today, calling on the New Zealand government to join global demands for an independent investigation. They were protesting over last month’s massacre of 15 Palestinian rescue workers ...17 hours ago

- Albanese pitches to aspiring home buyers with $10 billion plan and removal of means test on deposit ...

Source: The Conversation (Au and NZ) – By Michelle Grattan, Professorial Fellow, University of Canberra Anthony Albanese will promise a $10 billion scheme to facilitate the building of up to 100,000 homes that would be earmarked for sale to first home buyers. To be unveiled at Labor’s formal campaign launch ...17 hours ago

- Dutton to offer targeted income tax offset of up to $1,200

Source: The Conversation (Au and NZ) – By Michelle Grattan, Professorial Fellow, University of Canberra Peter Dutton at his party launch on Sunday will offer a “cost of living tax offset” of up to $1,200 to more than 10 million taxpayers. The one-off offset would go to taxpayers earning up ...17 hours ago

- Caitlin Johnstone: Israel’s innocent oopsie-poopsie medical massacre mistake

Report by Dr David Robie – Café Pacific. – COMMENTARY: By Caitlin Johnstone The Israeli military changed its story many times about why its forces killed 15 medical workers and then buried them and their vehicles to hide the evidence. After their initial claim that the medical vehicles were ...20 hours ago

- Foreign Minister wraps up Tonga visit, heading to Hawai’i

Immigration, maritime safety and a $13.8m Landcare Research programme were on the cards as Winston Peters completed the first leg of his Pacific tour. ...1 day ago

- ER Report: A Roundup of Significant Articles on EveningReport.nz for April 12, 2025

ER Report: Here is a summary of significant articles published on EveningReport.nz on April 12, 2025. Pacific climate activists join 180+ groups calling on COP30 hosts Brazil to end fossil fuel dependenceRNZ Pacific Pacific climate activists this week handed a letter from civil society to this year’s United Nations climate ...1 day ago

- Pacific climate activists join 180+ groups calling on COP30 hosts Brazil to end fossil fuel dependen...

RNZ Pacific Pacific climate activists this week handed a letter from civil society to this year’s United Nations climate conference hosts, Brazil, emphasising their demands for the end of fossil fuels and transition to renewable energy. More than 180 indigenous, youth, and environmental organisations from across the world have signed ...1 day ago

- Let’s get physical: a smashing finale for women’s Super Rugby

When the Blues beat Matatū in their first encounter this season, halfback Tara Turner memorably told Sky Sport afterward that the Blues’ “Mongrel Dogs” had come out to play. Matatū was battered into submission, 28-7. But in late March, the tables turned and Matatū stunned the physical northerners, inflicting the first ...1 day ago

- Short story: Old dogs, by Jackie Davis

Penny can see it all from here. The lawn that needs mowing, the gardens, once a riot of colour, her pride and joy she says when she describes it to the book club ladies, is now over-run with dandelions and ragwort. In the paddock beyond, she can see the sheep ...2 days ago

- New Zealand’s estuaries ‘in hot water’

Wading in among scratchy branches, sticky mud and ocean water might not be everyone’s cup of tea, but for Karin Bryan it’s a favourite pastime.Estuaries are her happy place.“I wouldn’t have said that 15 years ago. Fifteen years ago I had never walked in a mangrove in my life,” she ...2 days ago

- ‘I’ve watched them all’: David Lomas on his soft spot for rom coms

The host of David Lomas Investigates takes us through his life in TV, including the power of the Chesdale Cheese ad and his passion for 90s romantic comedies. It’s hard to imagine these days, but David Lomas never actually wanted to be on television. “Oh, I had no ambition to ...2 days ago

The host of David Lomas Investigates takes us through his life in TV, including the power of the Chesdale Cheese ad and his passion for 90s romantic comedies. It’s hard to imagine these days, but David Lomas never actually wanted to be on television. “Oh, I had no ambition to ...2 days ago - The Weekend: The lone wolf rarely triumphs

Madeleine Chapman reflects on the week that was. This week I found myself surrounded by collective action in all its forms. I watched the Auckland Philharmonia perform Hans Zimmer’s greatest hits to a packed out Aotea Centre for Art of the Score last weekend. It was incredible and rare to ...2 days ago

- Why I defended the men who hurt me

Allegations of sexual assault against Neil Gaiman have led the author to present texts from Scarlett Pavlovich that he says ‘demonstrate’ their relationship was consensual. One woman explains why she sent similar messages to men who hurt her. Sarah Grace is a pseudonym. When the story first broke to my ...2 days ago

- Can books change the world? A writer makes the case

Emma Sidnam debates with herself, and with friends, the value of writing with political purpose versus writing for entertainment. In the first real conversation I had with a friend, who is also a writer, we argued about art’s political power. He said that while an artless world is a depressing one, ...2 days ago

- The Secret Diary of .. Dirty Politics

A bedroom in MosgielSolid information is coming to light that Green MP and stain on the human race Benjamin Doyle wants to infiltrate a crèche so he can subject children to depraved sexual practises.The police need to be warned – and so do parents.A basement in HamiltonI told Mum that ...2 days ago

- The multibillion-dollar boost for New Zealand’s military: What you need to know

Explainer - $12 billion sounds like a lot to spend on the military. But is it, really? ...2 days ago

- Election Diary: Labor breaks practice of preferencing Greens to protect Jewish MP Josh Burns

Source: The Conversation (Au and NZ) – By Michelle Grattan, Professorial Fellow, University of Canberra It takes a bit for Labor not to preference the Greens but on Friday it was announced that in the Melbourne seat of Macnamara, where Jewish MP Josh Burns is embattled, the ALP will run ...2 days ago

- ‘Delusional’ Treaty Principles Bill scrapped but fight for Te Tiriti just beginning, say lawyers...

By Layla Bailey-McDowell, RNZ Māori news journalist Legal experts and Māori advocates say the fight to protect Te Tiriti is only just beginning — as the controversial Treaty Principles Bill is officially killed in Parliament. The bill — which seeks to redefine the principles of Te Tiriti o Waitangi — ...2 days ago

- Coalition plan to dump fuel efficiency penalties would make Australia a global outlier

Source: The Conversation (Au and NZ) – By Anna Mortimore, Lecturer, Griffith Business School, Griffith University The Coalition has announced it would, if elected to government, weaken a scheme aimed at cutting car emissions. The scheme, known as the New Vehicle Efficiency Standard (NVES), was introduced by the Albanese government ...2 days ago

- Peter Dutton’s climate policy backslide threatens Australia’s clout in the Pacific – right whe...

Source: The Conversation (Au and NZ) – By Wesley Morgan, Research Associate, Institute for Climate Risk and Response, UNSW Sydney Australia’s relationship with its regional neighbours could be in doubt under a Coalition government after two Pacific leaders challenged Opposition Leader Peter Dutton over his weak climate stance. This week, ...2 days ago

- Trade Minister Todd McClay writes to US counterparts over ‘harmful’ tariffs

An additional tariff by the US on New Zealand exporters is harmful and the Minister of Trade has written to his American counterparts to tell them that. ...2 days ago

- Could changing your diet improve endometriosis pain? A recent study suggests it’s possible

Source: The Conversation (Au and NZ) – By Evangeline Mantzioris, Program Director of Nutrition and Food Sciences, Accredited Practising Dietitian, University of South Australia ovchinnikova_ksenya/Shutterstock Endometriosis affects around 10% of women of reproductive age. It’s a chronic inflammatory condition that occurs when tissue similar to the lining of the ...2 days ago

- Kids cheering ‘chicken jockey!’ at A Minecraft Movie isn’t antisocial – it creates a chance ...

Source: The Conversation (Au and NZ) – By Sophia Staite, Lecturer in Humanities, University of Tasmania Courtesy of Warner Bros. Pictures Social media is ablaze with reports of kids going wild at screenings of A Minecraft Movie. Some cinemas are cracking down. There are reports of cinemas calling ...2 days ago

- ‘Call me next time’: Peters disparages Luxon’s tariff talks

Winston Peters told RNZ the prime minister had not consulted with him ahead of the calls. ...2 days ago

- Manaia House opens in Whangārei after $21.6 million interior upgrades

Services scattered Whangārei are combining under one roof called Manaia House. ...2 days ago

- The unusual death of the Treaty Principles Bill

The Treaty Principles Bill has been brutally defeated in Parliament. We have highlights from key speeches, and explain why its demise is so unusual. ...2 days ago

- Traded like assets, expected to be loyal: the unique double standard of being an Australian footy pl...

Source: The Conversation (Au and NZ) – By Hunter Fujak, Senior Lecturer in Sport Management, Deakin University Few issues in Australian sport generate as much media noise or emotional fan reactions as player movement, especially in our major winter codes the National Rugby League (NRL) and Australian Football League (AFL). ...2 days ago

- ‘It’s over’: Luxon rules out entertaining another iteration of Treaty Principles B...

It comes as ACT leader David Seymour vows to keep fighting the cause. ...2 days ago

- Christopher Luxon on the Treaty bill, new veteran’s day and trade wars

The Prime Minister faces questions after a week of chaos on markets at home and abroad. ...2 days ago

- Ministry of Foreign Affairs job relisted without ‘tikanga’ title after Winston Peters as...

The foreign minister is comfortable with the new role, after the word 'protocol' was used instead. ...2 days ago

- We study ‘planktivores’ – and found an amazing diversity of shapes among plankton-feeding fish...

Source: The Conversation (Au and NZ) – By Isabelle Ng, PhD candidate, College of Science and Engineering, James Cook University A couple of whip coral goby (_Bryaninops yongei_). randi_ang/Shutterstock Swim along the edge of a coral reef and you’ll often see schools of sleek, torpedo-shaped fishes gliding through the currents, ...2 days ago

- Government launches partnership to combat domestic violence in Auckland

Prevention of Family and Sexual Violence Minister Karen Chhour made the announcement at Ngāti Whātua Ōrākei. ...2 days ago

- ER Report: A Roundup of Significant Articles on EveningReport.nz for April 11, 2025

ER Report: Here is a summary of significant articles published on EveningReport.nz on April 11, 2025. Do Inuit languages really have many words for snow? The most interesting finds from our study of 616 languagesSource: The Conversation (Au and NZ) – By Charles Kemp, Professor, School of Psychological Sciences, The ...2 days ago

- Do Inuit languages really have many words for snow? The most interesting finds from our study of 616...

Source: The Conversation (Au and NZ) – By Charles Kemp, Professor, School of Psychological Sciences, The University of Melbourne Shutterstock Languages are windows into the worlds of the people who speak them – reflecting what they value and experience daily. So perhaps it’s no surprise different languages highlight different ...2 days ago

- The Friday Poem: ‘Pale Straw’ by Daniel Frears

A new poem by Daniel Frears. Pale Straw this season’s colour is pale straw a revelatory colour for an oh so special season it might mess with your head, or mine you can rub my belly like I was a dog. all actions are allowed in this .. phase. if ...2 days ago

Onya Steve.

For a moment I thought you writing in support of the position!

All good points. That aside though, I think until house prices correct (say a couple of years) people probably ARE better off renting.

But yes, the PIF are being total wankers and hiding many benefits. And some costs.

For example

1) they say 90% of a $345k house, yet ignore the cost of capital on the $34k deposit they’re implying.

2) They ignore the effect of inflation. Rents will increase with inflation, but mortgage payments will remain fixed.

3) They use 10.4% interest. I don’t imagine anyone in the country is stupid enough to get a floating rate loan right now. 9% would be a far more realistic figure, yet they haven’t used it for obvious reasons.

See Trav, the world is full of lying bastards who are out to screw people, you don’t have to believe in invisible unicorns to find them.

edit: I think the biggest reason not to buy a house right now under the circumstances they describe is that if (cough – when) values do drop, you could very easily wind up with negative equity if your deposit is only 10%. Negative equity = foreclosure = bad.

T-Rex

Agreed.

Caveat emptor ……. that being said there will always be good deals and bad deals regardless of whether the market is buoyant or depressed.

Absolutely – course, it’s a lot harder to approach things with due caution when all media, REINZ, and agents are peddling the “buy now or be forever in poverty” line. f*ckers.

On an unrelated note, GOD I hate our sensationalist media.

Headline: ‘Batman Star Denies Attack on Mum, Sister‘.

The article then mentions that no charges were made.

The article completely fails to mention that the charges under consideration were verbal assault class 4/5. What a f*cking beat-up!

Thanks for posting this story Steve. I will play the devils advocate to your position. The PIF do have a point, many of their own members are renters themselves. So in some cases their suggestion does make very good economic sense. Landlording is not an entirely risk free business, times like these it requires testicular fortitude that not everyone has.

I know I have covered the Govt suggestion to build affordable housing for HNZ tenants. A good idea in principle, as many of the existing HNZ buildings are not up to standard. However I stand by my opinion, that building sufficient centrally located affordable huosing is a virtually impossible suggestion. Ask anyone who has built in the last couple of years if you don’t believe me. The emphasis is on the “affordability” If an equal sum was spent renting existing buildings off the private sector the Govt could house perhaps ten times as many tenants. In fact HNZ, to their credit, already lease many such homes for their clients.

All good points. Plus 10.4% interest is fairly high, and all signs are that it’ll be coming down in the future. So assuming 10.4% over 25 years is a nice way of significantly increasing the cost of the house.

Indeed the print media is asinine all to often.

You seem a bit depressed lately – if you need a smile take a look at this for another spin on world news.

http://uncyclopedia.org/wiki/UnNews:Main_Page

Ha!

Awesome! Thanks

Yeah, I’ll get over it. ‘Interesting times’ at present. Interesting in an awesome way, but still raised stress.

Secondly and most importantly, if you’re buying the house at the end of 25 years, you own a house. If you rent, at the end of 25 years you have nothing

Actually, if you put the extra $440.00 into an interest-bearing account, you will have about 1.7 million in 25 years.

Actually, if you put the extra $440.00 into an interest-bearing account, you will have about 1.7 million in 25 years

Aye. It’s still a poor comparison though. Especially since it wouldn’t be $440 for 25 years, as inflation would force the rent up over time. Swings and roundabouts, ups and downs, and in the long run it’s likely not all that different. In the short run, I’m with the “don’t buy a house” option. Sorry people who bought houses, that’s what you get for believing in the perpetual 12% capital gain fairy.

I think the reason people who buy houses appear to end up more wealthy is that they’re forced to be. Your scenario is good in theory MD, but the reality seems to be that people put the 1.7 million into consumer products that end up worthless.

MacDr. but, as T-Rex points out and I didn’t mention because the numbers get awfully complicated and too many assumptions are needed to model it, rents will be going up over those 5 years, the mortgage payments won’t – so the difference won’t be anything like that amount.

Good spotting Mac – Steve talks about ‘apples with apples’ and then ignores his own advice.

I suspect he is right about rental properties being on average of lower quality. However the extent to which they are is debatable – I think the difference, on average, is going to be less that Steve’s implicitily assumed.

A comparison of rental vs sale property on Trademe would be a good start for anyone with the time and inclination.

“suggesting renting is cheap just as the Government appears to be developing a housing affordability policy. Funny coincidence that”

The only funny part to the whole post is that you think this is new. One of the primary underpinning reasons we’ve been talking about housing affordability for the last, oh, lets say 4 YEARS, is because this type of analysis shows just how badly the investment doesn’t stack up.

“rents will be going up over those 5 years, the mortgage payments won’t”

But the insurance component of ownership probably will as the value of the property increases. The maintenance will too as the house ages, and rates will continue ever upward.

Rent will be hardly moving in the next 5 years. Also, your first point is wrong. I rent a very nice 3brdm house with double garage 5mins from work. It costs me $220 a week. It’s value is over $350k. GG assumptions.

infused – Then your landlord is either a saint or a fool.

There is undeniably a house affordability crisis.

Without doubt, in the short term, renting is a far better option and all obligations and risks fall on the landlord eg think leaky buildings.

Over the long term, house values tend to rise, mortgage payments remain static and bingo you have equity. As our Rachel says, it won’t happen over night but it will happen.

I’m sure statistics support the view that people living in their own home tend to have better indicators of a more productive and happier, healthy life.

However, I would like to see some robust debate around a couple of related points.

First, the crazy tax laws that make owning a rental property so attractive (thereby increasing demand for entry level properties). I get benefits from owning a second home that I don’t get from owning my family home.

Linked to this the fact that the Boomers have benefitted from the housing boom and have effectively cut many of the younger generation out. Add to this the generous super and we have upwards intergenerational transfers.

Aaaaaarghhh! He said “youse” again! Steve, please stop murdering the English language!

[I choose to use youse as a humourous rhetorical tool, not out of ignorance. Go have a cry about it on your blog, someone might read it some day. SP]

If you put the difference between renting and paying mortgage into the sharemarket, or even Kiwisaver, you might end up with far more than what your freehold house is worth after 25 years. and then you still need a place to live when you want to realise that capital. And you have to consider all the other costs associated with ownership too which don’t stay constant either. And you still need an extra $1.7m to fill your house up with worthless consumer products!

This obsession with home ownership can only be remedied by a proper capital gains tax on ownership of homes other than your residence, to level the investment playing field. Interest rates may come down sooner too then.

The only reason that I bothered to buy a place was because of Telecom and landlords cashing up.

Had this little problem in the mid-90’s where I had quite a few phone lines including a couple of ISDN lines to get the kind of bandwidth I needed. ADSL was just starting to be talked about (and in a very expensive way). Then I had to move a couple of times mainly because of landlords. Each time cost a bundle to get the phone lines moved.

There are quite a lot of hidden problems with renting. What I want to see is more of a lease based system where I can get a lease for say 5 years.

The figures are actually too low for a lot of cases- once body corporate fees ($2500), property management fees ($2000+), accountant fees ($1500+) are taken into account.

However, the flipside is the massive amount of tax that can be rebated.

Nominal or Real interest rates? What was the interest rate you used? What is the chance that the interest rates will stay the same over the next 25 years?

Basically, don’t expect to get any richer renting for the next 25 years over buying a house. And, as has already been said, people who own their own house tend to be happier and more productive than those renting.

As long as you invest the difference between buying and renting you will be far more wealthy than if you just paid off a home.

I mean, how many people had that plan – with the money tied up in real estate and will be retiring on falling house prices?

It’s a lot easier to cut your losses when you have more liquid investments versus an illiquid family house or rental property at 4% gross yield lol.

And how paying off a home with an 80% mortgage could possibly be construed as productive when that capital could be going into a business, farm or share investment is beyond me…

writeups:

Things don’t stay the same. In the next 25 years interest rates will come down, house prices will drop in real terms and then they’ll probably reverse again. It’s probably not a great idea to buy a house ATM but that will change in the next few years. Rent now, buy when house prices are depressed and interest rates are low and in 25 years there’s a good chance that you will be better off than if you just tried to rent for the next 25 years.

The tax laws treat residential rental property EXACTLY the same as for all other business. If you think the law crazy for this purpose, then it is equally crazy for all other business purposes.

The Americans addressed this issue years ago by making all mortgage interest costs tax deductable regardless if it was on your home of residence or not.

A little thing called risk.

The risk is very high in residential property investment, just ask anyone who bought a blue chip apartment!

Seriously, anyone in their 50s/60s should have most of their savings in term deposits and government bonds. Anything else, you’re running the risk of having nothing to retire on.

The risk is very high in residential property investment, just ask anyone who bought a blue chip apartment!

Blue Chip was not an investment, it was a scam pyramid scheme… a fact that should have been obvious to anyone who thought about it for more than 2 seconds.

I agree that a balanced portfolio is sound practice, but even in this market… as soft as it is I made a $200k equity gain this week. Well it took me and my partner six months of careful planning and a lot hard work to do it, but it was still possible. No amount of term deposit or bonds will do that for you.

It is of course just a paper gain. But if I keep the property long enough (and it is cash flow neutral at present) then I should eventually be in a position to cash it out… but that might be 10-20 years out.

The fundamentals of the NZ property market are still sound. Demand will in the medium term exceed demand. More especially the demand for quality properties most definitely exceeds supply. Eventually the equity markets will hopefully rebalance themselves and the business cycle will start over again. (If it doesn’t then who cares? It’s Armageddon anyhow.)

The calculation of whether it makes more economic sense to buy or rent involves lots of calculations involving the growth of house prices versus the interest one can earn on money saved through renting. Empirically, however, one would expect renting to make more sense from a purely fiscal perspective.

The simple fact is that people prefer buying their own house, instead of renting, for at least two non-fiscal reasons that I can think of. One is that people like the security of owning their own home. They have an emotional investment in a particular house. The other is that a mortgage enforces fiscal discipline. It?s easy to talk of saving money in lieu of mortgage payments. But I think that many people are aware that if they weren?t forced to pay the money to the bank it would end up getting spent instead of saved.

Since people like owning their own home, it increases the demand for houses. It also reduces the pool of renters, resulting in lower market rents. The upshot of this is that buying a house is relatively expensive and renting is relatively cheap. Thus I would be extraordinarily surprised if renting didn?t make more sense, purely in terms of a household?s bottom line.

The security of owning a home is really a non-tangible asset. The price of this asset is the difference between the money saved by renting a home versus the money that would be spent paying off a mortgage. And I think if people value security, then it is perfectly rational for them to make the decision to purchase their own home.

The calculation of whether it makes more economic sense to buy or rent involves lots of calculations involving the growth of house prices versus the interest one can earn on money saved through renting. Empirically, however, one would expect renting to make more sense from a purely fiscal perspective.

The simple fact is that people prefer buying their own house, instead of renting, for at least two non-fiscal reasons that I can think of. One is that people like the security of owning their own home. They have an emotional investment in a particular house. The other is that a mortgage enforces fiscal discipline. It’s easy to talk of saving money in lieu of mortgage payments. But I think that many people are aware that if they weren’t forced to pay the money to the bank it would end up getting spent instead of saved.

Since people like owning their own home, it increases the demand for houses. It also reduces the pool of renters, resulting in lower market rents. The upshot of this is that buying a house is relatively expensive and renting is relatively cheap. Thus I would be extraordinarily surprised if renting didn’t make more sense, purely in terms of a household’s bottom line.

The security of owning a home is really a non-tangible asset. The price of this asset is the difference between the money saved by renting a home versus the money that would be spent paying off a mortgage. And I think if people value security, then it is perfectly rational for them to make the decision to purchase their own home.