Nats’ ACC plan only good for insurance companies and lawyers

Nats’ ACC plan only good for insurance companies and lawyers

Written By:

- Date published:

5:22 pm, July 16th, 2008 - 51 comments

Categories: national, workers' rights -

Tags: ACC

National has confirmed it intends to privatise the ACC scheme starting with opening the work account to private competition. This would see private insurers cream off large and low-risk employers with special deals, leaving the taxpayer to shoulder the burden of the rest (which would, in turn, be the basis for privatising of the remainder).

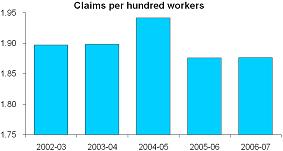

National says privatisation will somehow bring workplace accident rates down, which it claims are rising. Wrong: workplace accident rates are falling. It claims premiums will fall. Wrong: our premiums are already among the cheapest in the world, and we don’t have to pay anyone’s profits.

National says privatisation will somehow bring workplace accident rates down, which it claims are rising. Wrong: workplace accident rates are falling. It claims premiums will fall. Wrong: our premiums are already among the cheapest in the world, and we don’t have to pay anyone’s profits.

Australian insurance companies expect to make $200 million off this privatisation. These profits will be made not by higher premiums but by reduced pay-outs. As you know, that’s how private insurers make profits – by avoiding paying out whenever possible. In practice, that will mean Kiwis missing out on speedy treatment and income coverage, while Aussie insurers get rich.

Part of the genius of ACC is in decoupling blame from compensation. Occupational Safety and Health investigates accidents and holds businesses to health and safety regulations, ACC ensures the injured get treatment and income compensation, and businesses are incentivised to be safe because higher accident rates mean higher levies. Because of this administration of injury compensation leads the world in cheapness and efficiency and there are few court cases. Introducing competing profit-making insurers who are trying to minimise payouts would mean more expensive administration and law suits between individuals, businesses, and insurers tying up the already stretched court system. This was the case before ACC, it’s the case overseas, and it was beginning to happen again when National introduced competition in 1998. The efficiency of ACC is the envy of personal injury law experts around the world* but introducing private insurers will put an end to that.

Only two groups stand to gain from National privatising ACC. Not businesses and workers – insurers and lawyers.

[*I was in a personal injury lecture in Finland, our American professor was introducing the perplexed European students to the common law personal injury litigation system. He concluded that only one common law country had managed find a way to get rid of this resource consuming, lawyer-enriching system. No prizes for guessing which one.]51 comments on “Nats’ ACC plan only good for insurance companies and lawyers ”

- Comments are now closed

Links to post

- Comments are now closed

Recent Comments

- Resource Management and Property Rights

While there have been decades of complaints – from all sides – about the workings of the Resource Management Act (RMA), replacing is proving difficult. The Coalition Government is making another attempt.To help answer the question, I am going to use the economic lens of the Coase Theorem, set out ...2 hours ago

While there have been decades of complaints – from all sides – about the workings of the Resource Management Act (RMA), replacing is proving difficult. The Coalition Government is making another attempt.To help answer the question, I am going to use the economic lens of the Coase Theorem, set out ...2 hours ago - Bookshelf: the evolution and future of amphibious warfare

2027 may still not be the year of war it’s been prophesised as, but we only have two years left to prepare. Regardless, any war this decade in the Indo-Pacific will be fought with the ...2 hours ago

2027 may still not be the year of war it’s been prophesised as, but we only have two years left to prepare. Regardless, any war this decade in the Indo-Pacific will be fought with the ...2 hours ago - Parliament’s secret “transparency” regime

When the Parliament Bill Committee rejected calls for Parliamentary agencies to be subject to the Official Information Act last month, their excuse was interesting: Parliament didn't need the transparency of the OIA because it already had its own transparency regime! Which came as rather a surprise to everyone working in ...3 hours ago

When the Parliament Bill Committee rejected calls for Parliamentary agencies to be subject to the Official Information Act last month, their excuse was interesting: Parliament didn't need the transparency of the OIA because it already had its own transparency regime! Which came as rather a surprise to everyone working in ...3 hours ago - Centring people of colour to close the climate justice gap

Australia must do more to empower communities of colour in its response to climate change. In late February, the Multicultural Leadership Initiative hosted its Our Common Future summits in Sydney and Melbourne. These summits focused ...4 hours ago

- Presidency of doom

Questions 1. In his godawful decree, what tariff rate was imposed by Trump upon the EU?a. 10% same as New Zealandb. 20%, along with a sneer about themc. 40%, along with an outright lie about France d. 69% except for the town Melania comes from2. The justice select committee has ...5 hours ago

Questions 1. In his godawful decree, what tariff rate was imposed by Trump upon the EU?a. 10% same as New Zealandb. 20%, along with a sneer about themc. 40%, along with an outright lie about France d. 69% except for the town Melania comes from2. The justice select committee has ...5 hours ago - The ideology of grovelling to Trump

Yesterday the Trump regime in America began a global trade war, imposing punitive tariffs in an effort to extort political and economic concessions from other countries and US companies and constituencies. Trump's tariffs will make kiwis nearly a billion dollars poorer every year, but Luxon has decided to do nothing ...5 hours ago

- $6m later, 90% against, 8% for, Treaty Principles Bill Committee recommends Bill be shelved

Here’s 7 updates from this morning’s news:90% of submissions opposed the TPBNZ’s EV market tanked by Coalition policies, down ~70% year on yearTrump showFossil fuel money driving conservative policiesSimeon Brown won’t say that abortion is healthcarePhil Goff stands by comments and makes a case for speaking upBrian Tamaki cleared of ...6 hours ago

Here’s 7 updates from this morning’s news:90% of submissions opposed the TPBNZ’s EV market tanked by Coalition policies, down ~70% year on yearTrump showFossil fuel money driving conservative policiesSimeon Brown won’t say that abortion is healthcarePhil Goff stands by comments and makes a case for speaking upBrian Tamaki cleared of ...6 hours ago - Thanks, Folks: Mountain Tūī Hits A Milesone

7 hours ago

7 hours ago - The people have spoken

The Justice Committee has reported back on National's racist Principles of the Treaty of Waitangi Bill, and recommended by majority that it not proceed. So hopefully it will now rapidly go to second reading and be voted down. As for submissions, it turns out that around 380,000 people submitted on ...7 hours ago

- To fight disinformation, treat it as an insurgency

We need to treat disinformation as we deal with insurgencies, preventing the spreaders of lies from entrenching themselves in the host population through capture of infrastructure—in this case, the social media outlets. Combining targeted action ...7 hours ago

- The surprise of the Independent Intelligence Review: economic security

After copping criticism for not releasing the report for nearly eight months, Prime Minister Anthony Albanese released the Independent Intelligence Review on 28 March. It makes for a heck of a read. The review makes ...9 hours ago

- The surprise of the Independent Intelligence Review: economic security

After copping criticism for not releasing the report for nearly eight months, Prime Minister Anthony Albanese released the Independent Intelligence Review on 28 March. It makes for a heck of a read. The review makes ...9 hours ago

- Bernard’s Picks ‘n’ Mixes for Friday, April 4

In short this morning in our political economy:Donald Trump has shocked the global economy and markets with the biggest tariffs since the Smoot Hawley Act of 1930, which worsened the Great Depression.Global stocks slumped 4-5% overnight and key US bond yields briefly fell below 4% as investors fear a recession ...10 hours ago

In short this morning in our political economy:Donald Trump has shocked the global economy and markets with the biggest tariffs since the Smoot Hawley Act of 1930, which worsened the Great Depression.Global stocks slumped 4-5% overnight and key US bond yields briefly fell below 4% as investors fear a recession ...10 hours ago - I Hope I Never Send This Webworm

Hi,I’ve been imagining a scenario where I am walking along the pavement in the United States. It’s dusk, I am off to get a dirty burrito from my favourite place, and I see three men in hoodies approaching.Anther two men appear from around a corner, and this whole thing feels ...11 hours ago

Hi,I’ve been imagining a scenario where I am walking along the pavement in the United States. It’s dusk, I am off to get a dirty burrito from my favourite place, and I see three men in hoodies approaching.Anther two men appear from around a corner, and this whole thing feels ...11 hours ago - Australia’s plan for acquiring nuclear-powered submarines is on track

Since the announcement in September 2021 that Australia intended to acquire nuclear-powered submarines in partnership with Britain and the United States, the plan has received significant media attention, scepticism and criticism. There are four major ...12 hours ago

- Weekly Roundup 04-April-2025

On a very wet Friday, we hope you have somewhere nice and warm and dry to sit and catch up on our roundup of some of this week’s top stories in transport and urbanism. The header image shows Northcote Intermediate Students strolling across the Te Ara Awataha Greenway Bridge in ...12 hours ago

On a very wet Friday, we hope you have somewhere nice and warm and dry to sit and catch up on our roundup of some of this week’s top stories in transport and urbanism. The header image shows Northcote Intermediate Students strolling across the Te Ara Awataha Greenway Bridge in ...12 hours ago - Weekly Roundup 04-April-2025

On a very wet Friday, we hope you have somewhere nice and warm and dry to sit and catch up on our roundup of some of this week’s top stories in transport and urbanism. The header image shows Northcote Intermediate Students strolling across the Te Ara Awataha Greenway Bridge in ...12 hours ago

- The Hoon around the week to April 4

The podcast above of the weekly ‘Hoon’ webinar for paying subscribers on Thursday night features co-hosts & talking about the week’s news with regular and special guests, including: and Elaine Monaghan on the week in geopolitics and climate, including Donald Trump’s tariff shock yesterday; and,Labour’s Disarmament and Associate ...12 hours ago

The podcast above of the weekly ‘Hoon’ webinar for paying subscribers on Thursday night features co-hosts & talking about the week’s news with regular and special guests, including: and Elaine Monaghan on the week in geopolitics and climate, including Donald Trump’s tariff shock yesterday; and,Labour’s Disarmament and Associate ...12 hours ago - Stranger Days

I'm gonna try real goodSwear that I'm gonna try from now on and for the rest of my lifeI'm gonna power on, I'm gonna enjoy the highsAnd the lows will come and goAnd may your dreamsAnd may your dreamsAnd may your dreams never dieSongwriters: Ben Reed.These are Stranger Days than ...13 hours ago

I'm gonna try real goodSwear that I'm gonna try from now on and for the rest of my lifeI'm gonna power on, I'm gonna enjoy the highsAnd the lows will come and goAnd may your dreamsAnd may your dreamsAnd may your dreams never dieSongwriters: Ben Reed.These are Stranger Days than ...13 hours ago - Skeptical Science New Research for Week #14 2025

Open access notables A pronounced decline in northern vegetation resistance to flash droughts from 2001 to 2022, Zhang et al., Nature Communications: Here we show that vegetation resistance to flash droughts declines by up to 27% (±5%) over the Northern Hemisphere hotspots during 2001-2022, including eastern Asia, western North America, ...24 hours ago

Open access notables A pronounced decline in northern vegetation resistance to flash droughts from 2001 to 2022, Zhang et al., Nature Communications: Here we show that vegetation resistance to flash droughts declines by up to 27% (±5%) over the Northern Hemisphere hotspots during 2001-2022, including eastern Asia, western North America, ...24 hours ago - Trump’s tariffs: Australia’s worry is the effect on its trading partners

With the execution of global reciprocal tariffs, US President Donald Trump has issued his ‘declaration of economic independence for America’. The immediate direct effect on the Australian economy will likely be small, with more risk ...1 day ago

- In national security, governments still struggle to work with startups

AUKUS governments began 25 years ago trying to draw in a greater range of possible defence suppliers beyond the traditional big contractors. It is an important objective, and some progress has been made, but governments ...1 day ago

- What I saw at liberation day

I approach fresh Trump news reluctantly. It never holds the remotest promise of pleasure. I had the very, very least of expectations for his Rumble in the Jungle, his Thriller in Manila, his Liberation Day.God May 1945 is becoming the bitterest of jokes isn’t it?Whatever. Liberation Day he declared it ...1 day ago

I approach fresh Trump news reluctantly. It never holds the remotest promise of pleasure. I had the very, very least of expectations for his Rumble in the Jungle, his Thriller in Manila, his Liberation Day.God May 1945 is becoming the bitterest of jokes isn’t it?Whatever. Liberation Day he declared it ...1 day ago - Open Australia versus closed United States

Beyond trade and tariff turmoil, Donald Trump pushes at the three core elements of Australia’s international policy: the US alliance, the region and multilateralism. What Kevin Rudd called the ‘three fundamental pillars’ are the heart ...1 day ago

- The fix is in

So, having broken its promise to the nation, and dumped 85% of submissions on the Treaty Principles Bill in the trash, National's stooges on the Justice Committee have decided to end their "consideration" of the bill, and report back a full month early: Labour says the Justice Select Committee ...1 day ago

- Intelligence review is strong on workforce issues. Implementation may be harder

The 2024 Independent Intelligence Review offers a mature and sophisticated understanding of workforce challenges facing Australia’s National Intelligence Community (NIC). It provides a thoughtful roadmap for modernising that workforce and enhancing cross-agency and cross-sector collaboration. ...1 day ago

- Corruption Tsunami

OPINION AND ANALYSIS:Chief Ombudsman Peter Boshier’s comments singling out Health NZ for “acting contrary to the law” couldn’t be clearer. If you find my work of value, do consider subscribing and/or supporting me. Thank you.Health NZ has been acting a law unto itself. That includes putting its management under extraordinary ...1 day ago

OPINION AND ANALYSIS:Chief Ombudsman Peter Boshier’s comments singling out Health NZ for “acting contrary to the law” couldn’t be clearer. If you find my work of value, do consider subscribing and/or supporting me. Thank you.Health NZ has been acting a law unto itself. That includes putting its management under extraordinary ...1 day ago - Sharing security interests, ASEAN’s big three step up cooperation

Southeast Asia’s three most populous countries are tightening their security relationships, evidently in response to China’s aggression in the South China Sea. This is most obvious in increased cooperation between the coast guards of the ...1 day ago

- Technology can make Team Australia fit for strategic competition

In the late 1970s Australian sport underwent institutional innovation propelling it to new heights. Today, Australia must urgently adapt to a contested and confronting strategic environment. Contributing to this, a new ASPI research project will ...1 day ago

- Bernard’s Picks ‘n’ Mixes for Thursday, April 3

In short this morning in our political economy:The Nelson Hospital waiting list crisis just gets worse, including compelling interviews with an over-worked surgeon who is leaving, and a patient who discovered after 19 months of waiting for a referral that her bowel and ovaries were fused together with scar tissue ...2 days ago

In short this morning in our political economy:The Nelson Hospital waiting list crisis just gets worse, including compelling interviews with an over-worked surgeon who is leaving, and a patient who discovered after 19 months of waiting for a referral that her bowel and ovaries were fused together with scar tissue ...2 days ago - Gordon Campbell On The Clash Between Auckland Airport And Air New Zealand

Plainly, the claims being tossed around in the media last year that the new terminal envisaged by Auckland International Airport was a gold-plated “Taj Mahal” extravagance were false. With one notable exception, the Commerce Commission’s comprehensive investigation has ended up endorsing every other aspect of the airport’s building programme (and ...2 days ago

Plainly, the claims being tossed around in the media last year that the new terminal envisaged by Auckland International Airport was a gold-plated “Taj Mahal” extravagance were false. With one notable exception, the Commerce Commission’s comprehensive investigation has ended up endorsing every other aspect of the airport’s building programme (and ...2 days ago - Just what does drive so much of this global, Right-wing populism we all see at present?

Movements clustered around the Right, and Far Right as well, are rising globally. Despite the recent defeats we’ve seen in the last day or so with the win of a Democrat-backed challenger, Dane County Judge Susan Crawford, over her Republican counterpart, Waukesha County Judge Brad Schimel, in the battle for ...2 days ago

Movements clustered around the Right, and Far Right as well, are rising globally. Despite the recent defeats we’ve seen in the last day or so with the win of a Democrat-backed challenger, Dane County Judge Susan Crawford, over her Republican counterpart, Waukesha County Judge Brad Schimel, in the battle for ...2 days ago - Two-part webinar about the scientific consensus on human-caused global warming

In February 2025, John Cook gave two webinars for republicEN explaining the scientific consensus on human-caused climate change. 20 February 2025: republicEN webinar part 1 - BUST or TRUST? The scientific consensus on climate change In the first webinar, Cook explained the history of the 20-year scientific consensus on climate change. How do ...2 days ago

- Bookshelf: ‘Vampire state: The rise and fall of the Chinese economy’

After three decades of record-breaking growth, at about the same time as Xi Jinping rose to power in 2012, China’s economy started the long decline to its current state of stagnation. The Chinese Communist Party ...2 days ago

- Too complacent, too greedy

The Pike River Coal mine was a ticking time bomb.Ventilation systems designed to prevent methane buildup were incomplete or neglected.Gas detectors that might warn of danger were absent or broken.Rock bolting was skipped, old tunnels left unsealed, communication systems failed during emergencies.Employees and engineers kept warning management about the … ...2 days ago

The Pike River Coal mine was a ticking time bomb.Ventilation systems designed to prevent methane buildup were incomplete or neglected.Gas detectors that might warn of danger were absent or broken.Rock bolting was skipped, old tunnels left unsealed, communication systems failed during emergencies.Employees and engineers kept warning management about the … ...2 days ago - It’s time to imagine how China would act as regional hegemon

Regional hegemons come in different shapes and sizes. Australia needs to think about what kind of hegemon China would be, and become, should it succeed in displacing the United States in Asia. It’s time to ...2 days ago

- We don’t need the fast track to kill fossil fuels

RNZ has a story this morning about the expansion of solar farms in Aotearoa, driven by today's ground-breaking ceremony at the Tauhei solar farm in Te Aroha: From starting out as a tiny player in the electricity system, solar power generated more electricity than coal and gas combined for ...2 days ago

- How world order changes

After the Berlin Wall came down in 1989, and almost a year before the Soviet Union collapsed in late 1991, US President George H W Bush proclaimed a ‘new world order’. Now, just two months ...2 days ago

- Social Contracts Are Breaking

Warning: Some images may be distressing. Thank you for those who support my work. It means a lot.A shopfront in Australia shows Liberal leader Peter Dutton and mining magnate Gina Rinehart depicted with Nazi imageryUS Government Seeks Death Penalty for Luigi MangioneMangione was publicly walked in front of media in ...2 days ago

Warning: Some images may be distressing. Thank you for those who support my work. It means a lot.A shopfront in Australia shows Liberal leader Peter Dutton and mining magnate Gina Rinehart depicted with Nazi imageryUS Government Seeks Death Penalty for Luigi MangioneMangione was publicly walked in front of media in ...2 days ago - Wednesday 2 April

Aged care workers rallying against potential roster changes say Bupa, which runs retirement homes across the country, needs to focus on care instead of money. More than half of New Zealand workers wish they had chosen a different career according to a new survey. Consumers are likely to see a ...2 days ago

Aged care workers rallying against potential roster changes say Bupa, which runs retirement homes across the country, needs to focus on care instead of money. More than half of New Zealand workers wish they had chosen a different career according to a new survey. Consumers are likely to see a ...2 days ago - The Green’s Identity Bubble Problem.

The scurrilous attacks on Benjamin Doyle, a list Green MP, over his supposed inappropriate behaviour towards children has dominated headlines and social media this past week, led by frothing Rightwing agitators clutching their pearls and fanning the flames of moral panic over pedophiles and and perverts. Winston Peter decided that ...2 days ago

The scurrilous attacks on Benjamin Doyle, a list Green MP, over his supposed inappropriate behaviour towards children has dominated headlines and social media this past week, led by frothing Rightwing agitators clutching their pearls and fanning the flames of moral panic over pedophiles and and perverts. Winston Peter decided that ...2 days ago - Fabian Fundraiser – Twilight Time

Twilight Time Lighthouse Cuba, Wigan Street, Wellington, Sunday 6 April, 5:30pm for 6pm start. Twilight Time looks at the life and work of Desmond Ball, (1947-2016), a barefooted academic from ‘down under’ who was hailed by Jimmy Carter as “the man who saved the world”, as he proved the fallacy ...2 days ago

Twilight Time Lighthouse Cuba, Wigan Street, Wellington, Sunday 6 April, 5:30pm for 6pm start. Twilight Time looks at the life and work of Desmond Ball, (1947-2016), a barefooted academic from ‘down under’ who was hailed by Jimmy Carter as “the man who saved the world”, as he proved the fallacy ...2 days ago - That’s Democracy?

The landedAnd the wealthyAnd the piousAnd the healthyAnd the straight onesAnd the pale onesAnd we only mean the male ones!If you're all of the above, then you're ok!As we build a new tomorrow here today!Lyrics Glenn Slater and Allan Menken.Ah, Democracy - can you smell it?It's presently a sulphurous odour, ...2 days ago

The landedAnd the wealthyAnd the piousAnd the healthyAnd the straight onesAnd the pale onesAnd we only mean the male ones!If you're all of the above, then you're ok!As we build a new tomorrow here today!Lyrics Glenn Slater and Allan Menken.Ah, Democracy - can you smell it?It's presently a sulphurous odour, ...2 days ago - Think laterally: government air and shipping services can boost Australian defence

US President Donald Trump’s unconventional methods of conducting international relations will compel the next federal government to reassess whether the United States’ presence in the region and its security assurances provide a reliable basis for ...2 days ago

- Reserve Bank, bank capital etc

Things seem to be at a pretty low ebb in and around the Reserve Bank. There was, in particular, the mysterious, sudden, and as-yet unexplained resignation of the Governor (we’ve had four Governors since the Bank was given its operational autonomy 35 years ago, and only two have completed their ...2 days ago

Things seem to be at a pretty low ebb in and around the Reserve Bank. There was, in particular, the mysterious, sudden, and as-yet unexplained resignation of the Governor (we’ve had four Governors since the Bank was given its operational autonomy 35 years ago, and only two have completed their ...2 days ago - Luxon’s ‘going for growth’ actually means ‘going for debt reduction’

Long story short: PM Christopher Luxon said in January his Government was ‘going for growth’ and he wanted New Zealanders to develop a ‘culture of yes.’ Yet his own Government is constantly saying no, or not yet, to anchor investments that would unleash real private business investment and GDP growth. ...2 days ago

Long story short: PM Christopher Luxon said in January his Government was ‘going for growth’ and he wanted New Zealanders to develop a ‘culture of yes.’ Yet his own Government is constantly saying no, or not yet, to anchor investments that would unleash real private business investment and GDP growth. ...2 days ago - Luxon’s ‘going for growth’ actually means ‘going for debt reduction’

Long story short: PM Christopher Luxon said in January his Government was ‘going for growth’ and he wanted New Zealanders to develop a ‘culture of yes.’ Yet his own Government is constantly saying no, or not yet, to anchor investments that would unleash real private business investment and GDP growth. ...2 days ago

- Life after D-notices: Australia can learn from Britain’s updated system

For decades, Britain and Australia had much the same process for regulating media handling of defence secrets. It was the D-notice system, under which media would be asked not to publish. The two countries diverged ...2 days ago

- Life after D-notices: Australia can learn from Britain’s updated system

For decades, Britain and Australia had much the same process for regulating media handling of defence secrets. It was the D-notice system, under which media would be asked not to publish. The two countries diverged ...2 days ago

- Should Auckland demolish Spaghetti Junction?

This post by Nicolas Reid was originally published on Linked in. It is republished here with permission. In this article, I make a not-entirely-serious case for ripping out Spaghetti Junction in Auckland, replacing it with a motorway tunnel, and redeveloping new city streets and neighbourhoods above it instead. What’s ...2 days ago

- Should Auckland demolish Spaghetti Junction?

This post by Nicolas Reid was originally published on Linked in. It is republished here with permission. In this article, I make a not-entirely-serious case for ripping out Spaghetti Junction in Auckland, replacing it with a motorway tunnel, and redeveloping new city streets and neighbourhoods above it instead. What’s ...2 days ago

- Bernard’s Picks ‘n’ Mixes for Wednesday, April 2

In short this morning in our political economy:The Nelson Hospital crisis revealed by 1News’ Jessica Roden dominates the political agenda today. Yet again, population growth wasn’t planned for, or funded.Kāinga Ora is planning up to 900 house sales, including new ones, Jonathan Milne reports for Newsroom.One of New Zealand’s biggest ...3 days ago

In short this morning in our political economy:The Nelson Hospital crisis revealed by 1News’ Jessica Roden dominates the political agenda today. Yet again, population growth wasn’t planned for, or funded.Kāinga Ora is planning up to 900 house sales, including new ones, Jonathan Milne reports for Newsroom.One of New Zealand’s biggest ...3 days ago - Bernard’s Picks ‘n’ Mixes for Wednesday, April 2

In short this morning in our political economy:The Nelson Hospital crisis revealed by 1News’ Jessica Roden dominates the political agenda today. Yet again, population growth wasn’t planned for, or funded.Kāinga Ora is planning up to 900 house sales, including new ones, Jonathan Milne reports for Newsroom.One of New Zealand’s biggest ...3 days ago

- Diplomacy is the newest front in the Russia-Ukraine war

The war between Russia and Ukraine continues unabated. Neither side is in a position to achieve its stated objectives through military force. But now there is significant diplomatic activity as well. Ukraine has agreed to ...3 days ago

- The wettest choppiest part

This was my first thought about yesterday's announcement from Winston Peters, ferry-whisperer. Read more ...3 days ago

This was my first thought about yesterday's announcement from Winston Peters, ferry-whisperer. Read more ...3 days ago - How to deal with a kangaroo court

In November last year, Te Pāti Māori's Hana-Rawhiti Maipi-Clarke spoke for all of us when she led a haka against National's racist Treaty Principles Bill. National and its parliamentary patsies did not like that, so after kicking her out of the house for a day, they sought to drag her ...3 days ago

- AusAID can take USAID’s place in the Pacific islands

One of the first aims of the United States’ new Department of Government Efficiency was shutting down USAID. By 6 February, the agency was functionally dissolved, its seal missing from its Washington headquarters. Amid the ...3 days ago

- The US alliance is precious, but Australia should plan for more self-reliance

If our strategic position was already challenging, it just got worse. Reliability of the US as an ally is in question, amid such actions by the Trump administration as calling for annexation of Canada, threating ...3 days ago

- Monday 1 April

Small businesses will be exempt from complying with some of the requirements of health and safety legislation under new reforms proposed by the Government. The living wage will be increased to $28.95 per hour from September, a $1.15 increase from the current $27.80. A poll has shown large opposition to ...3 days ago

- Not Aprils’ Fools: Government Prioritises Road Cones Over Health & Safety, 6 Nelson Senior...

Summary A group of senior doctors in Nelson have spoken up, specifically stating that hospitals have never been as bad as in the last year.Patients are waiting up to 50 hours and 1 death is directly attributable to the situation: "I've never seen that number of patients waiting to be ...3 days ago

- The US has many chip vulnerabilities

Although semiconductor chips are ubiquitous nowadays, their production is concentrated in just a few countries, and this has left the US economy and military highly vulnerable at a time of rising geopolitical tensions. While the ...3 days ago

- Health and Safety changes driven by ACT party ideology

Health and Safety changes driven by ACT party ideology, not evidence said NZCTU Te Kauae Kaimahi President Richard Wagstaff. Changes to health and safety legislation proposed by the Minister for Workplace Relations and Safety Brooke van Velden today comply with ACT party ideology, ignores the evidence, and will compound New ...3 days ago

- Bernard’s Picks ‘n’ Mixes for Tuesday, April 1

In short in our political economy this morning:Fletcher Building is closing its pre-fabricated house-building factory in Auckland due to a lack of demand, particularly from the Government.Health NZ is sending a crisis management team to Nelson Hospital after a 1News investigation exposed doctors’ fears that nearly 500 patients are overdue ...3 days ago

In short in our political economy this morning:Fletcher Building is closing its pre-fabricated house-building factory in Auckland due to a lack of demand, particularly from the Government.Health NZ is sending a crisis management team to Nelson Hospital after a 1News investigation exposed doctors’ fears that nearly 500 patients are overdue ...3 days ago - Looking back to look forward, 10 years after the First Principles Review

Exactly 10 years ago, the then minister for defence, Kevin Andrews, released the First Principles Review: Creating One Defence (FPR). With increasing talk about the rising possibility of major power-conflict, calls for Defence funding to ...3 days ago

- The Government accidentally added us to their group chat

In events eerily similar to what happened in the USA last week, Greater Auckland was recently accidentally added to a group chat between government ministers on the topic of transport. We have no idea how it happened, but luckily we managed to transcribe most of what transpired. We share it ...4 days ago

- Dylan Attempts to Stop a Pig Butchering

Hi,When I look back at my history with Dylan Reeve, it’s pretty unusual. We first met in the pool at Kim Dotcom’s mansion, as helicopters buzzed overhead and secret service agents flung themselves off the side of his house, abseiling to the ground with guns drawn.Kim Dotcom was a German ...4 days ago

Hi,When I look back at my history with Dylan Reeve, it’s pretty unusual. We first met in the pool at Kim Dotcom’s mansion, as helicopters buzzed overhead and secret service agents flung themselves off the side of his house, abseiling to the ground with guns drawn.Kim Dotcom was a German ...4 days ago - Luxon Calls Snap Election!

Come around for teaDance me round and round the kitchenBy the light of my T.VOn the night of the electionAncient stars will fall into the seaAnd the ocean floor sings her sympathySongwriter: Bic Runga.The Prime Minister stared into the camera, hot and flustered despite the predawn chill. He looked sadly ...4 days ago

Come around for teaDance me round and round the kitchenBy the light of my T.VOn the night of the electionAncient stars will fall into the seaAnd the ocean floor sings her sympathySongwriter: Bic Runga.The Prime Minister stared into the camera, hot and flustered despite the predawn chill. He looked sadly ...4 days ago - Gordon Campbell On The Government’s Latest Ferries Scam

Has Winston Peters got a ferries deal for you! (Buyer caution advised.) Unfortunately, the vision that Peters has been busily peddling for the past 24 hours – of several shipyards bidding down the price of us getting smaller, narrower, rail-enabled ferries – looks more like a science fiction fantasy. One ...4 days ago

- 2025 Reading List: March

Completed reads for March: The Heart of the Antarctic [1907-1909], by Ernest Shackleton South [1914-1917], by Ernest Shackleton Aurora Australis (collection), edited by Ernest Shackleton The Book of Urizen (poem), by William Blake The Book of Ahania (poem), by William Blake The Book of Los (poem), by William Blake ...4 days ago

Completed reads for March: The Heart of the Antarctic [1907-1909], by Ernest Shackleton South [1914-1917], by Ernest Shackleton Aurora Australis (collection), edited by Ernest Shackleton The Book of Urizen (poem), by William Blake The Book of Ahania (poem), by William Blake The Book of Los (poem), by William Blake ...4 days ago - The Attacks on Benjamin Doyle are Depraved

First - A ReminderBenjamin Doyle Doesn’t Deserve ThisI’ve been following posts regarding Green MP Benjamin Doyle over the last few days, but didn’t want to amplify the abject nonsense.This morning, Winston Peters, New Zealand’s Deputy Prime Minister, answered the alt-right’s prayers - guaranteeing amplification of the topic, by going on ...4 days ago

First - A ReminderBenjamin Doyle Doesn’t Deserve ThisI’ve been following posts regarding Green MP Benjamin Doyle over the last few days, but didn’t want to amplify the abject nonsense.This morning, Winston Peters, New Zealand’s Deputy Prime Minister, answered the alt-right’s prayers - guaranteeing amplification of the topic, by going on ...4 days ago - The world can still keep Trump in check

US President Donald Trump has shown a callous disregard for the checks and balances that have long protected American democracy. As the self-described ‘king’ makes a momentous power grab, much of the world watches anxiously, ...4 days ago

- Febrile elaborate fantasies

They can be the very same words. And yet their meaning can vary very much.You can say I'll kill him about your colleague who accidentally deleted your presentation the day before a big meeting.You can say I'll kill him to — or, for that matter, about — Tony Soprano.They’re the ...4 days ago

They can be the very same words. And yet their meaning can vary very much.You can say I'll kill him about your colleague who accidentally deleted your presentation the day before a big meeting.You can say I'll kill him to — or, for that matter, about — Tony Soprano.They’re the ...4 days ago - National’s ghost ships

Back in 2020, the then-Labour government signed contracted for the construction and purchase of two new rail-enabled Cook Strait ferries, to be operational from 2026. But when National took power in 2023, they cancelled them in a desperate effort to make the books look good for a year. And now ...4 days ago

- Red tape that tears us apart: regulation fragments Indo-Pacific cyber resilience

The fragmentation of cyber regulation in the Indo-Pacific is not just inconvenient; it is a strategic vulnerability. In recent years, governments across the Indo-Pacific, including Australia, have moved to reform their regulatory frameworks for cyber ...4 days ago

- Economic Bulletin March 2025

Welcome to the March 2025 Economic Bulletin. The feature article examines what public private partnerships (PPPs) are. PPPs have been a hot topic recently, with the coalition government signalling it wants to use them to deliver infrastructure. However, experience with PPPs, both here and overseas, indicates we should be wary. ...4 days ago

- Te Pāti Māori Urges Governor-General to Block Repeal of 7AA

Today, the Oranga Tamariki (Repeal of Section 7AA) Amendment Bill has passed its third and final reading, but there is one more stage before it becomes law. The Governor-General must give their ‘Royal assent’ for any bill to become legally enforceable. This means that, even if a bill gets voted ...21 hours ago

- Release: Abortion care quietly shelved amid staff shortage

Abortion care at Whakatāne Hospital has been quietly shelved, with patients told they will likely have to travel more than an hour to Tauranga to get the treatment they need. ...1 day ago

Abortion care at Whakatāne Hospital has been quietly shelved, with patients told they will likely have to travel more than an hour to Tauranga to get the treatment they need. ...1 day ago - Release: Govt guts Kāinga Ora, third of workforce under axe

The gutting of Kāinga Ora shows public housing is not a priority for this Government as it removes a third of the roles at the housing agency. ...1 day ago

- Release: Thousands of submissions excluded from Treaty Principles Bill report

Thousands of New Zealanders’ submissions are missing from the official parliamentary record because the National-dominated Justice Select Committee has rushed work on the Treaty Principles Bill. ...1 day ago

- Release: Uncertainty remains over the impact of tariffs

Today’s announcement of 10 percent tariffs for New Zealand goods entering the United States is disappointing for exporters and consumers alike, with the long-lasting impact on prices and inflation still unknown. ...1 day ago

- Release: Worst February for building consents in over a decade

The National Government’s choices have contributed to a slow-down in the building sector, as thousands of people have lost their jobs in construction. ...2 days ago

- Release: Labour supports Willie Apiata’s selfless act

Willie Apiata’s decision to hand over his Victoria Cross to the Minister for Veterans is a powerful and selfless act, made on behalf of all those who have served our country. ...2 days ago

- Te Pāti Māori MPs Denied Fundamental Rights in Privileges Committee Hearing

The Privileges Committee has denied fundamental rights to Debbie Ngarewa-Packer, Rawiri Waititi and Hana-Rawhiti Maipi-Clarke, breaching their own standing orders, breaching principles of natural justice, and highlighting systemic prejudice and discrimination within our parliamentary processes. The three MPs were summoned to the privileges committee following their performance of a haka ...3 days ago

- Release: Govt health and safety changes put workers at risk

Changes to New Zealand’s health and safety laws will strip back key protections for small businesses and put working Kiwis at greater risk. ...4 days ago

- Release: Kiwis worse off this April thanks to Govt choices

April 1 used to be a day when workers could count on a pay rise with stronger support for those doing it tough, but that’s not the case under this Government. ...4 days ago

- Release: Three more years for Interislander ferries

Winston Peters is shopping for smaller ferries after Nicola Willis torpedoed the original deal, which would have delivered new rail enabled ferries next year. ...4 days ago

- Release: Myanmar junta must stop the airstrikes

The Government should work with other countries to press the Myanmar military regime to stop its bombing campaign especially while the country recovers from the devastating earthquake. ...4 days ago

- Release: National failing to deliver on supermarkets

National is paying lip service to its promises to bring down the cost of living, failing to make any meaningful change in the grocery sector. ...4 days ago

- Release: Labour backs farmers’ call for better process on GE

Labour shares farmers’ concerns that the Gene Technology Bill is moving too fast. ...1 week ago

- Release: Bar still too high for small mental health providers

Small mental health providers will still be locked out of co-funding from the Mental Health Innovation Fund despite a lower threshold. ...1 week ago

- Greens call for Govt to scrap proposed ECE changes

The Green Party is calling for the Government to scrap proposed changes to Early Childhood Care, after attending a petition calling for the Government to ‘Put tamariki at the heart of decisions about ECE’. ...1 week ago

The Green Party is calling for the Government to scrap proposed changes to Early Childhood Care, after attending a petition calling for the Government to ‘Put tamariki at the heart of decisions about ECE’. ...1 week ago - NZ First Introduces Bill That Gives Democracy Back To The People

New Zealand First has introduced a Member’s Bill today that will remove the power of MPs conscience votes and ensure mandatory national referendums are held before any conscience issues are passed into law. “We are giving democracy and power back to the people”, says New Zealand First Leader Winston Peters. ...1 week ago

New Zealand First has introduced a Member’s Bill today that will remove the power of MPs conscience votes and ensure mandatory national referendums are held before any conscience issues are passed into law. “We are giving democracy and power back to the people”, says New Zealand First Leader Winston Peters. ...1 week ago - Speech: Navigating the New World (Dis)order in Turbulent Times

Welcome to members of the diplomatic corp, fellow members of parliament, the fourth estate, foreign affairs experts, trade tragics, ladies and gentlemen. ...1 week ago

- Te Pāti Māori Call for Mandatory Police Body Cameras

In recent weeks, disturbing instances of state-sanctioned violence against Māori have shed light on the systemic racism permeating our institutions. An 11-year-old autistic Māori child was forcibly medicated at the Henry Bennett Centre, a 15-year-old had his jaw broken by police in Napier, kaumātua Dean Wickliffe went on a hunger ...1 week ago

- Release: Kiwis lose faith in job market

Confidence in the job market has continued to drop to its lowest level in five years as more New Zealanders feel uncertain about finding work, keeping their jobs, and getting decent pay, according to the latest Westpac-McDermott Miller Employment Confidence Index. ...1 week ago

- Greens question Govt commitment to environmental protection with RMA reform

The Greens are calling on the Government to follow through on their vague promises of environmental protection in their Resource Management Act (RMA) reform. ...2 weeks ago

- Release: Govt must tackle meth use crisis

New data shows methamphetamine use is spiralling out of control while the Government sits on its hands. ...2 weeks ago

- “Make New Zealand First Again”

“Make New Zealand First Again” Ladies and gentlemen, First of all, thank you for being here today. We know your lives are busy and you are working harder and longer than you ever have, and there are many calls on your time, so thank you for the chance to speak ...2 weeks ago

- Release: Govt’s continued lack of action on Gaza condemned

Hundreds more Palestinians have died in recent days as Israel’s assault on Gaza continues and humanitarian aid, including food and medicine, is blocked. ...2 weeks ago

- Release: National at sea over Defence jobs

National is looking to cut hundreds of jobs at New Zealand’s Defence Force, while at the same time it talks up plans to increase focus and spending in Defence. ...2 weeks ago

- Release: National standards returning by stealth

It’s been revealed that the Government is secretly trying to bring back a ‘one-size fits all’ standardised test – a decision that has shocked school principals. ...2 weeks ago

- Release: Kiwis still struggling as economy stumbles along

Kiwis aren’t feeling any better off despite figures showing a very slight growth in GDP in the December quarter. ...2 weeks ago

- Greens call for compassionate release of Dean Wickliffe

The Green Party is calling for the compassionate release of Dean Wickliffe, a 77-year-old kaumātua on hunger strike at the Spring Hill Corrections Facility, after visiting him at the prison. ...2 weeks ago

- Another failed ETS auction, another indictment on the Govt’s climate credibility

The ETS auction’s failure today is yet another clear sign that the Government is failing us all on climate action. ...2 weeks ago

- Release: Luxon quick to give away principled position on nukes

Christopher Luxon seems to have thrown New Zealand’s principled anti-nuclear advocacy under a bus. ...2 weeks ago

- NZ must act on Israel’s slaughter of children

The Green Party is calling on Government MPs to support Chlöe Swarbrick’s Member’s Bill to sanction Israel for its unlawful presence and illegal actions in Palestine, following another day of appalling violence against civilians in Gaza. ...2 weeks ago

- Release: Still no certainty for disability communities

One year on from the Government’s abrupt and callous changes to disability funding, the community still has no idea what the future holds. ...2 weeks ago

- Green Party backs volunteer firefighters in their call for ACC recognition

The Green Party stands in support of volunteer firefighters petitioning the Government to step up and change legislation to provide volunteers the same ACC coverage and benefits as their paid counterparts. ...2 weeks ago

- Stand Up for Palestine: A Call to Action Against Israels Treacherous Attack

At 2.30am local time, Israel launched a treacherous attack on Gaza killing more than 300 defenceless civilians while they slept. Many of them were children. This followed a more than 2 week-long blockade by Israel on the entry of all goods and aid into Gaza. Israel deliberately targeted densely populated ...2 weeks ago

- MP Views: Living Strong, The Economy, Servicing Our Nation, The Golden Egg, and 4 Year Terms

Living Strong, Aging Well There is much discussion around the health of our older New Zealanders and how we can age well. In reality, the delivery of health services accounts for only a relatively small percentage of health outcomes as we age. Significantly, dry warm housing, nutrition, exercise, social connection, ...3 weeks ago

- Shane Jones has no shame

Shane Jones’ display on Q&A showed how out of touch he and this Government are with our communities and how in sync they are with companies with little concern for people and planet. ...3 weeks ago

- New planning laws to end the culture of ‘no’

The Government’s new planning legislation to replace the Resource Management Act will make it easier to get things done while protecting the environment, say Minister Responsible for RMA Reform Chris Bishop and Under-Secretary Simon Court. “The RMA is broken and everyone knows it. It makes it too hard to build ...2 weeks ago

The Government’s new planning legislation to replace the Resource Management Act will make it easier to get things done while protecting the environment, say Minister Responsible for RMA Reform Chris Bishop and Under-Secretary Simon Court. “The RMA is broken and everyone knows it. It makes it too hard to build ...2 weeks ago - New Zealand & India Comprehensive FTA consultation begins

Trade and Investment Minister Todd McClay has today launched a public consultation on New Zealand and India’s negotiations of a formal comprehensive Free Trade Agreement. “Negotiations are getting underway, and the Public’s views will better inform us in the early parts of this important negotiation,” Mr McClay says. We are ...2 weeks ago

- Cost of living support coming for 1.5 million New Zealanders

More than 900 thousand superannuitants and almost five thousand veterans are among the New Zealanders set to receive a significant financial boost from next week, an uplift Social Development and Employment Minister Louise Upston says will help support them through cost-of-living challenges. “I am pleased to confirm that from 1 ...2 weeks ago

- Iwi join discussion on geothermal potential

Progressing a holistic strategy to unlock the potential of New Zealand’s geothermal resources, possibly in applications beyond energy generation, is at the centre of discussions with mana whenua at a hui in Rotorua today, Resources and Regional Development Minister Shane Jones says. The Coalition Government is in the early stages ...2 weeks ago

- Building consent data shows need for bold reforms

New annual data has exposed the staggering cost of delays previously hidden in the building consent system, Building and Construction Minister Chris Penk says. “I directed Building Consent Authorities to begin providing quarterly data last year to improve transparency, following repeated complaints from tradespeople waiting far longer than the statutory ...2 weeks ago

- Reining in water price increases for Aucklanders

Increases in water charges for Auckland consumers this year will be halved under the Watercare Charter which has now been passed into law, Local Government Minister Simon Watts and Auckland Minister Simeon Brown say. The charter is part of the financial arrangement for Watercare developed last year by Auckland Council ...2 weeks ago

- Strong interest in modernising biosecurity law

There is wide public support for the Government’s work to strengthen New Zealand’s biosecurity protections, says Biosecurity Minister Andrew Hoggard. “The Ministry for Primary Industries recently completed public consultation on proposed amendments to the Biosecurity Act and the submissions show that people understand the importance of having a strong biosecurity ...2 weeks ago

- New independent review function for civil aviation decisions

A new independent review function will enable individuals and organisations to seek an expert independent review of specified civil aviation regulatory decisions made by, or on behalf of, the Director of Civil Aviation, Acting Transport Minister James Meager has announced today. “Today we are making it easier and more affordable ...2 weeks ago

- Enhanced urgent care service for Napier

The Government will invest in an enhanced overnight urgent care service for the Napier community as part of our focus on ensuring access to timely, quality healthcare, Health Minister Simeon Brown has today confirmed. “I am delighted that a solution has been found to ensure Napier residents will continue to ...2 weeks ago

- Construction begins on new adult mental health building in Christchurch

Health Minister Simeon Brown and Mental Health Minister Matt Doocey attended a sod turning today to officially mark the start of construction on a new mental health facility at Hillmorton Campus. “This represents a significant step in modernising mental health services in Canterbury,” Mr Brown says. “Improving health infrastructure is ...2 weeks ago

- It’s official: Kiwis can look forward to better days

Finance Minister Nicola Willis has welcomed confirmation the economy has turned the corner. Stats NZ reported today that gross domestic product grew 0.7 per cent in the three months to December following falls in the June and September quarters. “We know many families and businesses are still suffering the after-effects ...2 weeks ago

- Sealing improves safety on Forgotten World Highway

The sealing of a 12-kilometre stretch of State Highway 43 (SH43) through the Tangarakau Gorge – one of the last remaining sections of unsealed state highway in the country – has been completed this week as part of a wider programme of work aimed at improving the safety and resilience ...2 weeks ago

- NZ – US relations on strong footing

Deputy Prime Minister and Foreign Minister Winston Peters says relations between New Zealand and the United States are on a strong footing, as he concludes a week-long visit to New York and Washington DC today. “We came to the United States to ask the new Administration what it wants from ...2 weeks ago

- International Anti-Money Laundering rule changes support government reforms

Associate Justice Minister Nicole McKee has welcomed changes to international anti-money laundering standards which closely align with the Government’s reforms. “The Financial Action Taskforce (FATF) last month adopted revised standards for tackling money laundering and the financing of terrorism to allow for simplified regulatory measures for businesses, organisations and sectors ...2 weeks ago

- New electronic system to support pharmacy efficiency

Associate Health Minister David Seymour says he welcomes Medsafe’s decision to approve an electronic controlled drug register for use in New Zealand pharmacies, allowing pharmacies to replace their physical paper-based register. “The register, developed by Kiwi brand Toniq Limited, is the first of its kind to be approved in New ...2 weeks ago

- RIF delivering for regional NZ, more to come

The Coalition Government’s drive for regional economic growth through the $1.2 billion Regional Infrastructure Fund is on track with more than $550 million in funding so far committed to key infrastructure projects, Regional Development Minister Shane Jones says. “To date, the Regional Infrastructure Fund (RIF) has received more than 250 ...2 weeks ago

- Comments following bilateral with US Secretary of State Rubio

[Comments following the bilateral meeting with United States Secretary of State, Marco Rubio; United States State Department, Washington D.C.] * We’re very pleased with our meeting with Secretary of State Marco Rubio this afternoon. * We came here to listen to the new Administration and to be clear about what ...2 weeks ago

- New State Highway 2 roundabout to improve road safety in Eastern Bay of Plenty

The intersection of State Highway 2 (SH2) and Wainui Road in the Eastern Bay of Plenty will be made safer and more efficient for vehicles and freight with the construction of a new and long-awaited roundabout, says Transport Minister Chris Bishop. “The current intersection of SH2 and Wainui Road is ...2 weeks ago

- Ocean Race returning to Auckland

The Ocean Race will return to the City of Sails in 2027 following the Government’s decision to invest up to $4 million from the Major Events Fund into the international event, Auckland Minister Simeon Brown says. “New Zealand is a proud sailing nation, and Auckland is well-known internationally as the ...2 weeks ago

- New associate psychology role to grow the mental health workforce

Improving access to mental health and addiction support took a significant step forward today with Mental Health Minister Matt Doocey announcing that the University of Canterbury have been the first to be selected to develop the Government’s new associate psychologist training programme. “I am thrilled that the University of Canterbury ...2 weeks ago

- First stage of Manukau Health Park expansion open to patients

Health Minister Simeon Brown has today officially opened the new East Building expansion at Manukau Health Park. “This is a significant milestone and the first stage of the Grow Manukau programme, which will double the footprint of the Manukau Health Park to around 30,000m2 once complete,” Mr Brown says. “Home ...2 weeks ago

- Proceeds of crime to fund safety measures in central Auckland

The Government will boost anti-crime measures across central Auckland with $1.3 million of funding as a result of the Proceeds of Crime Fund, Auckland Minister Simeon Brown and Associate Justice Minister Nicole McKee say. “In recent years there has been increased antisocial and criminal behaviour in our CBD. The Government ...2 weeks ago

- Consultation on options to strengthen food waste for pigs regulations

The Government is moving to strengthen rules for feeding food waste to pigs to protect New Zealand from exotic animal diseases like foot and mouth disease (FMD), says Biosecurity Minister Andrew Hoggard. ‘Feeding untreated meat waste, often known as "swill", to pigs could introduce serious animal diseases like FMD and ...2 weeks ago

- PMs Luxon & Modi deepen NZ-India ties

Prime Minister Christopher Luxon and Indian Prime Minister Narendra Modi held productive talks in New Delhi today. Fresh off announcing that New Zealand and India would commence negotiations towards a Comprehensive Free Trade Agreement, the two Prime Ministers released a joint statement detailing plans for further cooperation between the two countries across ...3 weeks ago

- New Zealand & India strengthen forestry ties

Agriculture and Trade Minister Todd McClay signed a new Memorandum of Cooperation (MOC) today during the Prime Minister’s Indian Trade Mission, reinforcing New Zealand’s commitment to enhancing collaboration with India in the forestry sector. “Our relationship with India is a key priority for New Zealand, and this agreement reflects our ...3 weeks ago

- New Zealand & India strengthen horticultural ties

Agriculture and Trade Minister Todd McClay signed a new Memorandum of Cooperation (MOC) today during the Prime Minister’s Indian Trade Mission, reinforcing New Zealand’s commitment to enhancing collaboration with India in the horticulture sector. “Our relationship with India is a key priority for New Zealand, and this agreement reflects our ...3 weeks ago

- Family Court Judges appointed

Attorney-General Judith Collins today announced the appointment of two new Family Court Judges. The new Judges will take up their roles in April and May and fill Family Court vacancies at the Auckland and Manukau courts. Annette Gray Ms Gray completed her law degree at Victoria University before joining Phillips ...3 weeks ago

- New High Dependency Unit will expand critical care services in Wellington

Health Minister Simeon Brown has today officially opened Wellington Regional Hospital’s first High Dependency Unit (HDU). “This unit will boost critical care services in the lower North Island, providing extra capacity and relieving pressure on the hospital’s Intensive Care Unit (ICU) and emergency department. “Wellington Regional Hospital has previously relied ...3 weeks ago

- RAISINA DIALOGUE 2025: KĀLACHAKRA – PEOPLE, PEACE AND PLANET

Namaskar, Sat Sri Akal, kia ora and good afternoon everyone. What an honour it is to stand on this stage - to inaugurate this august Dialogue - with none other than the Honourable Narendra Modi. My good friend, thank you for so generously welcoming me to India and for our ...3 weeks ago

- Rejecting Apologies: Human Rights Commissioner Must Be Held Accountable

We stand in solidarity with all communities impacted by Islamophobia, racism, and discrimination. We call for genuine accountability, not empty apologies. It is imperative that the government takes decisive action to restore integrity to the Human Rights ...2 hours ago

We stand in solidarity with all communities impacted by Islamophobia, racism, and discrimination. We call for genuine accountability, not empty apologies. It is imperative that the government takes decisive action to restore integrity to the Human Rights ...2 hours ago - Government Is Misleading Public Over Labelling Of GMO Food

"This is a broken promise to the public. People demand the right to choose and want products from gene editing to be labelled,” said Jon Carapiet, spokesman for GE-Free New Zealand (in Food and Environment). ...2 hours ago

- The parliamentary processes behind the missing submissions story

Public submissions potentially ignored and unrecorded were a focus this week. We background how the process usually works and what will happen now. ...2 hours ago

Public submissions potentially ignored and unrecorded were a focus this week. We background how the process usually works and what will happen now. ...2 hours ago - Work safety expert critical of Minister Brooke van Velden’s workplace ‘myths’

"The things that she is recommending won't actually do anything much to address critical risks." ...2 hours ago

- If a child has extra needs, support can be hard to find. This new approach can help make it easier a...

Source: The Conversation (Au and NZ) – By David Trembath, Professor of Speech Pathology, Griffith University Lukas/Pexels If your child is struggling with certain everyday activities – such as playing with other kids, getting dressed or paying attention – you might want to get them assessed to see if ...2 hours ago

Source: The Conversation (Au and NZ) – By David Trembath, Professor of Speech Pathology, Griffith University Lukas/Pexels If your child is struggling with certain everyday activities – such as playing with other kids, getting dressed or paying attention – you might want to get them assessed to see if ...2 hours ago - Complaint over teaching tikanga Māori in law schools rejected

But the select committee also put a limit on how much cultural education was required. ...3 hours ago

- Daylight saving time ends Sunday. Why do we change our clocks? And how does it affect our bodies?

Source: The Conversation (Au and NZ) – By Meltem Weger, Research Fellow, Institute for Molecular Bioscience, The University of Queensland Kampus Productions/Pexels As summer fades into autumn, most Australian states and territories will set their clocks back an hour as daylight saving time ends and standard time resumes. ...3 hours ago

- ‘Not an extension of Australia’ – Trump’s tariffs ‘reinforces’ Norfolk Island’s indepe...

By Caleb Fotheringham, RNZ Pacific journalist Norfolk Island sees its United States tariff as an acknowledgment of independence from Australia. Norfolk Island, despite being an Australian territory, has been included on Trump’s tariff list. The territory has been given a 29 percent tariff, despite Australia getting only 10 percent. It ...4 hours ago

- Nurses’ Union Backs Call To Scrap Anti-Treaty Bill

Parliament's Justice Committee has released its report into the Principles of the Treaty of Waitangi Bill and has recommended it does not proceed. ...4 hours ago

- Heroin found in cocaine and ‘ice’, and snorting a line can be lethal

Source: The Conversation (Au and NZ) – By Darren Roberts, Conjoint Associate Professor in Clinical Pharmacology and Toxicology, St Vincent’s Healthcare Clinical Campus, UNSW Sydney Skrypnykov Dmytro/Shutterstock Authorities in New South Wales and Victoria have been warning the public about worrying cases of heroin overdoses after people thought ...4 hours ago

- Labour, Te Pāti Māori lose ground – April Taxpayers Union-Curia poll

Labour and Te Pāti Māori have lost support, the latest Taxpayers Union-Curia poll suggests. ...5 hours ago

- Crew on Manawanui during sinking were under-trained, ship not up to task – report

A damning report explains how the disaster on a Samoan reef happened, including a full transcript of the dramatic night. ...5 hours ago

- Transcript: What happened when the Manawanui Navy ship grounded off Samoa

A witness is heard calling for calm, before a mayday is put out and crew are ordered to abandon ship. Here is how the grounding played out. ...5 hours ago

- Trump tariffs: Trade Minister Todd McClay gets clarification on how the United States’ new reg...

The flat 10 percent duty being applied to US imports will apply on top of any existing tariffs, but there are some exceptions. ...5 hours ago

- Justice Committee Presents Report To The House On The Principles Of The Treaty Of Waitangi Bill

This is a Final Report of the Justice Committee. ...6 hours ago

- It’s not easy being a street tree, but this heroic eucalypt withstands everything we throw at it

Source: The Conversation (Au and NZ) – By Gregory Moore, Senior Research Associate, School of Agriculture, Food and Ecosystem Sciences, The University of Melbourne alybaba/Shutterstock Street trees usually grow in appalling soils, have little space for their roots, are rarely watered and often get aggressively trimmed by road authorities ...6 hours ago

- The Friday Poem: ‘reluctant heterosexual’ by Amanda Faye Martin

A new poem by Amanda Faye Martin. reluctant heterosexual one time i got snowed in with a guy i thought i didn’t want to sleep with but then he said something that felt true like clarity could be simple like things could be known like picking fruit in warm weather ...6 hours ago

A new poem by Amanda Faye Martin. reluctant heterosexual one time i got snowed in with a guy i thought i didn’t want to sleep with but then he said something that felt true like clarity could be simple like things could be known like picking fruit in warm weather ...6 hours ago - The Unity Books bestseller chart for the week ending April 4

The only published and available best-selling indie book chart in New Zealand is the top 10 sales list recorded every week at Unity Books’ stores in High St, Auckland, and Willis St, Wellington. AUCKLAND 1 Sunrise on the Reaping by Suzanne Collins (Scholastic, $30) More of that good Hunger Games stuff: ...6 hours ago

- Pupil off to the dentist after biting into hard plastic in school lunch

A Palmerston North school wants to change school lunch providers after a child bit into a hard piece of plastic in their lunch. ...6 hours ago

- Pupil off the to the dentist after biting into hard plastic in school lunch

A Palmerston North school wants to change school lunch providers after a child bit into a hard piece of plastic in their lunch. ...6 hours ago

- Watch live: Crew on Manawanui during sinking were under-trained, ship not up to task – report

A damning report explains how the disaster on a Samoan reef happened, including a full transcript of the dramatic night. ...6 hours ago

- Review: New Zealand’s first musical sitcom Happiness hums with charm and joy

Three’s new local comedy is definitely not the same old song and dance, writes Tara Ward. This is an excerpt from our weekly pop culture newsletter Rec Room. Sign up here. Charlie Summers has barely set foot on New Zealand soil before the flash mob begins. As he glides down the ...6 hours ago

- Labor leads in three recent national polls, four weeks from the election

Source: The Conversation (Au and NZ) – By Adrian Beaumont, Election Analyst (Psephologist) at The Conversation; and Honorary Associate, School of Mathematics and Statistics, The University of Melbourne The federal election will be held in four weeks. A national YouGov poll, conducted March 28 to April 3 from a sample ...7 hours ago

- Law Commission Recommends New Legislation For Managing High-Risk Offenders

The Commission makes 149 reform recommendations to the Government. They include a new Act to replace the current law governing preventive detention, extended supervision orders and public protection orders. ...7 hours ago

- Justice Select committee calls for Treaty Principles Bill to be scrapped

Parliament's Justice Committee has recommended the Treaty Principles Bill go no further. ...7 hours ago

- Ancient Rome used high tariffs to raise money too – and created other economic problems along the ...

Source: The Conversation (Au and NZ) – By Peter Edwell, Associate Professor in Ancient History, Macquarie University Nuntiya/Shutterstock Tariffs are back in the headlines this week, with United States President Donald Trump introducing sweeping new tariffs of at least 10% on a vast range of goods imported to the ...8 hours ago

- ‘Curiosity-driven research’ led to a recent major medical breakthrough. But it’s under threat

Source: The Conversation (Au and NZ) – By Sean Coakley, Senior Research Fellow, School of Biomedical Sciences, The University of Queensland Hakase_420/Shutterstock Earlier this year news broke about doctors in London curing blindness in children with a rare genetic condition. The genetic condition was a severe, albeit rare, ...8 hours ago

- Russia and China both want influence over Central Asia. Could it rupture their friendship?

Source: The Conversation (Au and NZ) – By Dilnoza Ubaydullaeva, Lecturer in Government, Flinders University As he looks to solidify his territorial gains in Ukraine in a potential ceasefire deal, Russian President Vladimir Putin has one eye trained on Russia’s southern border – and boosting Russian influence in Central Asia. ...8 hours ago

- New laws needed for high-risk offenders, Law Commission says

The country needs an entirely new set of laws to manage high-risk offenders safely and more humanely, the Law Commission says. ...8 hours ago

- Yes, data can produce better policy – but it’s no substitute for real-world experience

Source: The Conversation (Au and NZ) – By Anna Matheson, Associate Professor in Public Health and Policy, Te Herenga Waka — Victoria University of Wellington Shutterstock Governments like to boast that “data-driven” policies are the best way to make fair, efficient decisions. They collect statistics, set targets and adjust ...8 hours ago

- Select committee recommends scrapping Treaty principles bill amid huge opposition

Delivering the report 40 days ahead of schedule, the justice committee has recommended, by majority, that the bill not proceed. The justice select committee has reported back on the Principles of the Treaty of Waitangi Bill, recommending it to not proceed following one of the most polarising consultation periods in ...9 hours ago

- Review: A former Minecraft superfan’s verdict on A Minecraft Movie

Much of Thomas Giblin’s childhood was spent playing Minecraft. Does the new movie adaptation do it justice? I’ve adored Minecraft, the open-world sandbox video game where you can build whatever you want, ever since I was a speckly-faced, spikey-haired, socially-awkward kid. I spent all my lunchtimes and countless late nights ...9 hours ago

- Review: A former Minecraft superfan’s verdict on A Minecraft Movie

Much of Thomas Giblin’s childhood was spent playing Minecraft. Does the new movie adaptation do it justice? I’ve adored Minecraft, the open-world sandbox video game where you can build whatever you want, ever since I was a speckly-faced, spikey-haired, socially-awkward kid. I spent all my lunchtimes and many late nights ...9 hours ago

- Cost of Lower Hutt’s Riverlink project doubles to $1.5 billion

Big roadworks on State Highway 2 through Lower Hutt, called Riverlink, are going to cost more than twice as much as originally said. ...10 hours ago

- Cost of Lower Hutt’s Riverlink project doubles to $1.5 billion

Big roadworks on State Highway 2 through Lower Hutt, called Riverlink, are going to cost more than twice as much as originally said. ...10 hours ago

- If it walks like a penguin, and talks like a penguin…

Analysis: From China to the uninhabited subantarctic islands, Trump’s problem is not that other countries are imposing big trade barriers. His problem is this: American. Consumers. Want. Our. Stuff. The post If it walks like a penguin, and talks like a penguin… appeared first on Newsroom. ...10 hours ago

Analysis: From China to the uninhabited subantarctic islands, Trump’s problem is not that other countries are imposing big trade barriers. His problem is this: American. Consumers. Want. Our. Stuff. The post If it walks like a penguin, and talks like a penguin… appeared first on Newsroom. ...10 hours ago - Hospital’s faulty pipe upgrade marked as complete, when it wasn’t

Health New Zealand has admitted it marked an upgrade to faulty pipes at Auckland City Hospital as complete when in fact it was not. ...10 hours ago

- An exotic escape, or empty illusion? How The White Lotus exposes the contradictions of luxury travel

Source: The Conversation (Au and NZ) – By Anita Manfreda, Senior Lecturer in Tourism, Torrens University Australia Warner Bros The White Lotus season three returns to familiar territory: an exotic escape, privileged and powerful guests, the supposed heights of luxury. But beneath this lies a satirical critique of ...11 hours ago

- A day at Polyfest 2025: food, fits and fades

It takes a small village to put together the world’s largest Polynesian cultural festival. We met a few of the people who make it happen. Yes there’s six stages, a tonne of kai trucks and stalls, but it’s all the people at ASB Polyfest that you notice first. They’re thronged ...11 hours ago

- Third of emergency housing applications being rejected by MSD

The Ministry of Social Development is declining more than 90 emergency housing applications a month because people have "caused or contributed to their immediate need". ...11 hours ago

Using speedy in the same sentence as ACC is laughable.

You do realise that privitise and open to competition are two diferent things. Example, Telecom has been privitised and NZ Post has been opened to competition.

Just because workplace accident rates are comming down it doesn’t mean that they can’t come down further or faster.

If private insurers offer incentives to make workplaces safer then they will become safer, though almost every workplace accident I’ve witnessed has come from stupidity or laziness rather than fundamental safety issues.

As for ACC efficiency, pull the other one, I’ve dealt with more of their absurdly inefficient clusterfucks than I care to mention.

[it seems Oliver knows better than PriceWaterhouseCoopers who carried out a study of ACC and concluded it was very efficient compared to cover in other countries. Next, Oliver denies the IPCC’s findings on climate change because sometimes he’s cold. SP]

Now’s a good time to reiterate my challenge to anyone who thinks this isn’t the first step in a privatisation plan, which would ultimately result in the scheme being no longer free to users or universal.

Anyone?

Edit: Oh, Oliver! Care to have a crack?

L

workplace accident rates are falling

No, Steve, workplace claims are falling. Some large employers are now effectively self-insured, remember?

our premiums are already among the cheapest in the world

This is a common misunderstanding. Our premiums are, in fact, heavily subsidized. Where do you think the ACC levy on petrol is going?

Part of the genius of ACC is in decoupling blame from compensation

Agreed. And this did not change when National allowed competition into workplace insurance. ACC and the workplace insurer had to sort out exactly what a “workplace accident” was, but this is fairly well defined and caused little disagreement and little use of lawyers. Remember the guy who got stabbed in the company car park in a gang altercation? That is how precise the law is – cause is virtually irrelevant, place of accident is paramount.

In short, all that happened last time was that we all paid substantially less premium. None of the problems you are suggesting eventuated – and they should have happened within six months of the change, if they were going to.

Lew

ACC is not free if you are an employer or an employee.

Of course it’s about privatisation. Opening Post up to competition wasn’t because post has a great big infrastructure and a monopoly position. ACC has an infrastructure that could easily be replicated by pumping up the size of current private health care providers or handled by accident insurers over the ditch. I would imagine that a combination of national government led increased ACC premiums and undercutting competition would see it gone pretty quickly. then the real games could begin…

Oh and hi blar – why are you posting as oliver now?