Tax cuts for landlords will not reduce rents

Tax cuts for landlords will not reduce rents

Written By:

- Date published:

11:23 am, March 11th, 2024 - 127 comments

Categories: Christopher Luxon, cost of living, national, politicans, same old national, tenants' rights -

Tags: trickle down

Recently the Government has been working out how to cut funding for school lunches for poor kids while at the same time it has also announced that it will restore interest deductibility for landlords.

The interest deductibility changes are being pushed through by tweaking an existing bill when it is reported back to Parliament. The ability for the public to make submissions and to point out how bad the policy is will not be there.

The Government claims that the tax change is a return to conventional tax treatment of the business of being a landlord and will also mean that rents will reduce.

As to the former claim there is one difference. Landlords almost inevitably get into the rental business with the expectation that after a while they will be able to sell their property and make a significant tax gain. Rental income is not the primary driver.

As to the latter claim there is precious little proof that this will actually occur. When interest rates reduced there was no discernible reduction in rents.

This Treasury paper concludes that wage inflation and relative supply and demand of dwellings are the two key drivers of rent inflation for new tenancies at the national level. The paper also said that “[m]ortgage interest rates positively affect rents but relatively little, and the relationship is not robust across model specifications”.

Let’s think about one recent example which shows why the Government’s assumptions are overly optimistic.

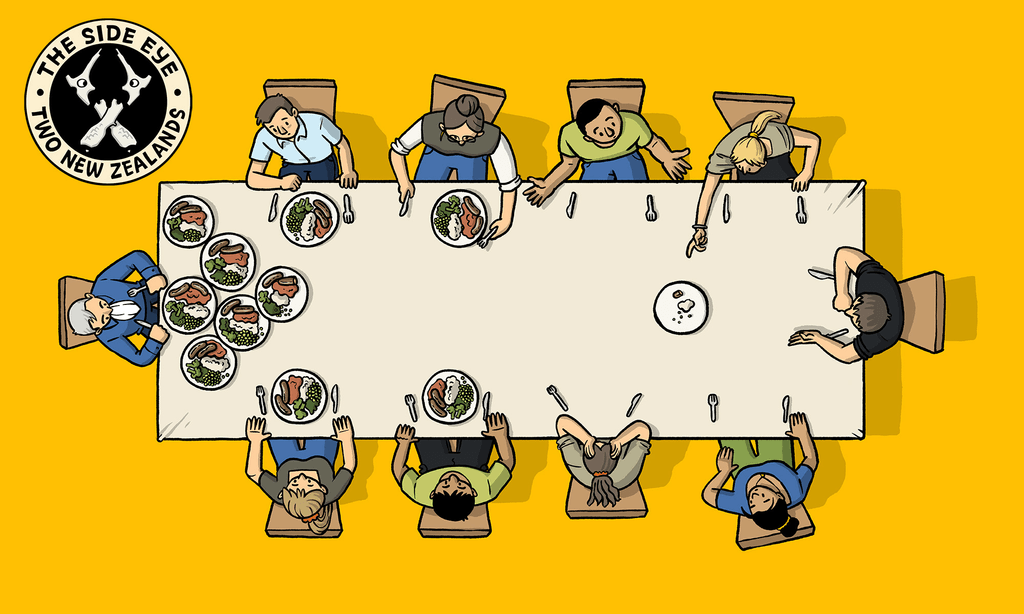

The subject person, who for present purposes will be called “Christopher” is the head of a large organisation. He also owns a property in Auckland that he rents out to his employer as an office. Rental for this property is determined by an independent valuation.

Along with five other properties he also owns a Wellington Apartment that is mortgage free. As part of his entitlements under his employment contract he also has the use of a large mansion in Wellington.

Instead of using the mansion he chose to maximise his return by electing to receive $1,000 a week so that he could continue to use his mortgage free apartment. Clearly maximising his wealth is more important than anything else.

Would giving him a tax return make him reduce the amount he claimed? This is unlikely as shown by his earlier behaviour.

And here is the thing, the tax rebate will not affect him at all as his apartment is mortgage free. Clearly he is maximised by personal gain and not by anything else. And he was asked if favourable tax treatment would cause him to reduce rentals on his properties and he said that he was not sure. I am confident that when push comes to shove he will rely on market forces to set rental levels for his properties, and not let some generally expressed desire to reduce his return

The group that are most likely to be affected by the change are the mega landlords. There are 346 in the country and they each own at least 200 properties. The CTU’s pre election analysis was that they would each save up to $1.3 million over five years thanks to this tax cut.

Ka Ching.

Can you imagine them agreeing to reduce the rentals they charge? Especially at a time that immigration is strong and there is increasing pressure on housing stock?

This is a classic example of the Government rewarding its funders. The policy will not work. All it will do is increase money for the wealthy and drive up house prices as landlords look to increase stock.

If you wanted to increase stock you would do what the last Government did, allow depreciation but only for new builds. Competing with first home buyers to purchase homes does not add one new house to existing housing stock. Offering incentives to landlords to buy new stock would, but that incentive will soon be gone.

This is yet more evidence free Government reckons. Clearly they think that trickle down works, and all that is needed is more, not less trickle down.

127 comments on “Tax cuts for landlords will not reduce rents ”

- Comments are now closed

- Comments are now closed

Recent Comments

- Luxon & Willis Double Down on Ferries Debacle

The day before today, Nicola Willis told the House that they would have to wait until the ferries announcement for the details about ferries cost etc. It was the same promise Luxon has been making in Parliament over the last weeks and months: the details are coming, the details are ...29 minutes ago

The day before today, Nicola Willis told the House that they would have to wait until the ferries announcement for the details about ferries cost etc. It was the same promise Luxon has been making in Parliament over the last weeks and months: the details are coming, the details are ...29 minutes ago - Luigi Mangione and Jury Nullification

Luigi Mangione, the shooter of the Ultimate Healthcare CEO, has been caught by the cops after a tip-off from a McDonalds worker. (A timely reminder, perhaps, that there is an official boycott against McDonalds for their profiting from and support of Israel’s occupation in Palestine, and it has been having ...2 hours ago

Luigi Mangione, the shooter of the Ultimate Healthcare CEO, has been caught by the cops after a tip-off from a McDonalds worker. (A timely reminder, perhaps, that there is an official boycott against McDonalds for their profiting from and support of Israel’s occupation in Palestine, and it has been having ...2 hours ago - Thursday 12 December

There has been widespread condemnation of the Government’s mishandling of the Cook Strait ferry replacements, including from unions, industry, and political parties. It has also led to public division among the coalition, with Winston Peters and David Seymour at odds regarding cost and privatisation. In other political news, Labour says ...4 hours ago

There has been widespread condemnation of the Government’s mishandling of the Cook Strait ferry replacements, including from unions, industry, and political parties. It has also led to public division among the coalition, with Winston Peters and David Seymour at odds regarding cost and privatisation. In other political news, Labour says ...4 hours ago - Foreshadowing HYEFU 2024

By way of prologue, the closest parallel to the current economic situation may be when Ruth Richardson became Minister of Finance in late 1990. The economy had been contracting, although there were signs of a fragile recovery. She was an Austerian and cut public spending savagely. The economy plunged a ...4 hours ago

By way of prologue, the closest parallel to the current economic situation may be when Ruth Richardson became Minister of Finance in late 1990. The economy had been contracting, although there were signs of a fragile recovery. She was an Austerian and cut public spending savagely. The economy plunged a ...4 hours ago - Nicky No Boats

I remember you by, thunderclap in the skyLightning flash, tempers flare'Round the horn if you dareI just spent six months in a leaky boatLucky just to keep afloatSongwriters: Brian Timothy FinnToday, a tale of such ineptitude, unwarranted confidence and underplanning that you will scarcely believe it. I can hear you ...5 hours ago

I remember you by, thunderclap in the skyLightning flash, tempers flare'Round the horn if you dareI just spent six months in a leaky boatLucky just to keep afloatSongwriters: Brian Timothy FinnToday, a tale of such ineptitude, unwarranted confidence and underplanning that you will scarcely believe it. I can hear you ...5 hours ago - Ferries delayed again, then handed to Peters, who hits out at Seymour

Willis wouldn’t give a cost estimate or confirm new ferries would be ‘rail enabled’ rather than ‘rail-compatible’, but Seymour has let slip the ferries and ‘landside’ development would cost around $1.5 billion. Photo: Lynn Grieveson / The KākāMōrena. Long stories short, the six things that matter in Aotearoa’s political economy ...6 hours ago

- When Should You Consider Retreat? – The Sooner the Better

This is a guest post by Waitematā local board member Dr Alex Bonham, about the Auckland Council’s Shoreline Adaption Plans. Currently consultation is open for the Auckland Central & Ōrākei to Karaka Bay SAPs until December 18th. If the sea bowls through your front door, through the house and ...6 hours ago

This is a guest post by Waitematā local board member Dr Alex Bonham, about the Auckland Council’s Shoreline Adaption Plans. Currently consultation is open for the Auckland Central & Ōrākei to Karaka Bay SAPs until December 18th. If the sea bowls through your front door, through the house and ...6 hours ago - Shameless advertising: Two days only — 50% off subscriptions, forever

But wait!! If you would like to pay me LESS, on Friday the discount will be bigger. Subscription benefits include my endless gratitude, warm fuzzy feelings, bragging rights, and a slight spring in your step. ...9 hours ago

But wait!! If you would like to pay me LESS, on Friday the discount will be bigger. Subscription benefits include my endless gratitude, warm fuzzy feelings, bragging rights, and a slight spring in your step. ...9 hours ago - Toot, toot, here comes Winston

The big question hanging over yesterday’s ferry announcement press conference was why Winston Peters was there at all. Finance Minister Willis went out of her way to tell a press conference yesterday afternoon that the Government had not decided whether to have rail-enabled ferries or even whether KiwiRail should run ...9 hours ago

The big question hanging over yesterday’s ferry announcement press conference was why Winston Peters was there at all. Finance Minister Willis went out of her way to tell a press conference yesterday afternoon that the Government had not decided whether to have rail-enabled ferries or even whether KiwiRail should run ...9 hours ago - Channelling Madame Defarge: Of Lampposts and CEOs

The recent shooting of that Health Insurance CEO in the USA has sparked quite the online furor. On one hand, one is confronted with a violent murder… on the other hand, many, many people think the victim was such a monster, he got what was coming to him. The result ...15 hours ago

The recent shooting of that Health Insurance CEO in the USA has sparked quite the online furor. On one hand, one is confronted with a violent murder… on the other hand, many, many people think the victim was such a monster, he got what was coming to him. The result ...15 hours ago - Ranking the New Zealand Prime Ministers since 1893

The New Zealand Listener has a poll of historians ranking Prime Ministers since Seddon (1893-1906): https://www.nzherald.co.nz/the-listener/politics/the-real-power-list-nzs-prime-ministers-rated/UEHAIM2NQRDKNPWR3HNKBLKK6Q/#google_vignette Alas, it’s behind a paywall. Bastards. So I thought I’d provide my own list as an exercise: Peter Fraser Richard Seddon Helen Clark Keith Holyoake (second term) M.J. Savage Gordon Coates Norman Kirk ...21 hours ago

The New Zealand Listener has a poll of historians ranking Prime Ministers since Seddon (1893-1906): https://www.nzherald.co.nz/the-listener/politics/the-real-power-list-nzs-prime-ministers-rated/UEHAIM2NQRDKNPWR3HNKBLKK6Q/#google_vignette Alas, it’s behind a paywall. Bastards. So I thought I’d provide my own list as an exercise: Peter Fraser Richard Seddon Helen Clark Keith Holyoake (second term) M.J. Savage Gordon Coates Norman Kirk ...21 hours ago - Wednesday 11 December

The Government has kicked the can down the road on the replacement Interislander ferries, by setting up a company to begin a procurement process, rather than making a decision. But they have made a decision when it comes to greyhound racing, banning the sport over the next 20 months. The ...22 hours ago

- It’s got to be good for you

One of my favourite Substackers had an intriguing question to ask this morning:Why was a British baby born after September 1953 significantly more likely to die from disease later in life than a British baby born before September 1953?I gave it a good try but I didn’t get it. Makes ...22 hours ago

One of my favourite Substackers had an intriguing question to ask this morning:Why was a British baby born after September 1953 significantly more likely to die from disease later in life than a British baby born before September 1953?I gave it a good try but I didn’t get it. Makes ...22 hours ago - NZCTU slams Government’s ferry fiasco

The NZCTU Te Kauae Kaimahi is slamming the Government for failing to show any leadership on infrastructure delivery after they revealed today that they have no plan to replace the Cook Strait ferries a year on from their decision to cancel the iReX project. “Today’s announcement by the Minister of ...22 hours ago

- Climate Change: Hope is not a plan

One of the purposes of the Zero Carbon Act was to break the bad old cycle of announcing targets and then doing nothing to meet them. Instead, governments would have regular carbon budgets with relatively short deadlines - meaning any failure would happen on their watch - and be required ...23 hours ago

One of the purposes of the Zero Carbon Act was to break the bad old cycle of announcing targets and then doing nothing to meet them. Instead, governments would have regular carbon budgets with relatively short deadlines - meaning any failure would happen on their watch - and be required ...23 hours ago - A bad joke

That's the only way to describe National's announcement today on replacement Cook Strait ferries. A year ago they cancelled iRex, which would have given us two new, rail-enabled ferries in January 2026 for $551 million (plus port costs). Today, they're promising two smaller, non-rail enabled ferries sometime in 2029, and ...1 day ago

- The Long Awaited Kiwirail Interislander Announcement

Complimentary:In July, Nicola Willis promised that her expensive Kiwirail Interislander “independent” advisory committee had finished their work - and an answer was due to the public imminently.That blew out to August, then September, October, November, before Winston Peters announced the government was definitely going to announce the decision on December ...1 day ago

Complimentary:In July, Nicola Willis promised that her expensive Kiwirail Interislander “independent” advisory committee had finished their work - and an answer was due to the public imminently.That blew out to August, then September, October, November, before Winston Peters announced the government was definitely going to announce the decision on December ...1 day ago - Does Luxon understand Keynesian economics?

Do our journalists? Do LabourDo we? John Maynard KeynesOh, I do so love New Zealand news, our left-leaning, deliberatively disinterested, striving-to-be-unbiased media. They are working so hard for us, doing the mundane jobs that I would hate to do. That’s why deliberatively never used my English degree to become a ...1 day ago

Do our journalists? Do LabourDo we? John Maynard KeynesOh, I do so love New Zealand news, our left-leaning, deliberatively disinterested, striving-to-be-unbiased media. They are working so hard for us, doing the mundane jobs that I would hate to do. That’s why deliberatively never used my English degree to become a ...1 day ago - Luigi Mangione’s Pain

This morning I followed a link to Luigi Mangione’s now defunct Substack He is the accused in the murder of US health insurance CEO Brian Thompson.And of course it must be noted that murder is not the right course of action, and there can only be condolences to Thompson’s family.But ...1 day ago

This morning I followed a link to Luigi Mangione’s now defunct Substack He is the accused in the murder of US health insurance CEO Brian Thompson.And of course it must be noted that murder is not the right course of action, and there can only be condolences to Thompson’s family.But ...1 day ago - Seymour’s Principles Rejected

Look inside, look inside your tiny mind, now look a bit harder'Cause we're so uninspiredSo sick and tired of all the hatred you harbourSo you say our treaty is not okay; well, I think you're just evilYou're just some racist who can't tie my lacesYour point of view is medievalFuck ...1 day ago

Look inside, look inside your tiny mind, now look a bit harder'Cause we're so uninspiredSo sick and tired of all the hatred you harbourSo you say our treaty is not okay; well, I think you're just evilYou're just some racist who can't tie my lacesYour point of view is medievalFuck ...1 day ago - Top 10: Ferries, $2.1 billion in fossil fuel related healthcare costs, Curia’s Problem & M...

1. Fast-Track projects: Speaker rules no private benefit in list (RNZ, Russell Palmer)In a fairly rare move, the Speaker of the House Garry Brownlee (National) overturned the ruling of the Clerk, David Wilson, and Assistant Speaker, Barbara Kuriger (National).The Clerk of the House of Representatives advises the speaker and members ...1 day ago

1. Fast-Track projects: Speaker rules no private benefit in list (RNZ, Russell Palmer)In a fairly rare move, the Speaker of the House Garry Brownlee (National) overturned the ruling of the Clerk, David Wilson, and Assistant Speaker, Barbara Kuriger (National).The Clerk of the House of Representatives advises the speaker and members ...1 day ago - Does AT misunderstand the government’s new PT targets?

A few weeks ago we revealed that a new policy from the NZTA is pushing for changes to the level of public transport costs covered by fares (and a few other things), which could potentially lead to fare hikes by as much as 70 percent or service cuts. While some ...1 day ago

- When haste makes waste & is risky, dangerous & mean

Mōrena. Long stories short, the six things that matter in Aotearoa’s political economy around housing, climate and poverty on Wednesday, December 11 in The Kākā’s Dawn Chorus and Pick ‘n’ Mix are:The National-ACT-NZ First Coalition Government is set to announce today it will spend $900 million on new ferries to ...1 day ago

- Gordon Campbell on the government’s ongoing ferries disaster

The Interislander ferry Aratere approaching the entrance to Wellington Harbour after crossing Cook Strait on the final ferry sailing of the day, due to large swells. 12 July 2017 New Zealand Herald Photograph by Mark MitchellI wouldn’t have picked Nicola Willis to be a big AC/DC fan, but “Dirty Deeds ...1 day ago

The Interislander ferry Aratere approaching the entrance to Wellington Harbour after crossing Cook Strait on the final ferry sailing of the day, due to large swells. 12 July 2017 New Zealand Herald Photograph by Mark MitchellI wouldn’t have picked Nicola Willis to be a big AC/DC fan, but “Dirty Deeds ...1 day ago - Sabin 33 #6 – Are solar projects harming biodiversity?

On November 1, 2024 we announced the publication of 33 rebuttals based on the report "Rebutting 33 False Claims About Solar, Wind, and Electric Vehicles" written by Matthew Eisenson, Jacob Elkin, Andy Fitch, Matthew Ard, Kaya Sittinger & Samuel Lavine and published by the Sabin Center for Climate Change Law at Columbia ...2 days ago

On November 1, 2024 we announced the publication of 33 rebuttals based on the report "Rebutting 33 False Claims About Solar, Wind, and Electric Vehicles" written by Matthew Eisenson, Jacob Elkin, Andy Fitch, Matthew Ard, Kaya Sittinger & Samuel Lavine and published by the Sabin Center for Climate Change Law at Columbia ...2 days ago - Submission on the NZ Post Deed of Understanding 2024 review

Postal services enable individuals, businesses, and communities to build and maintain social connections, and to participate economically, culturally, and politically. The NZCTU is concerned that the proposed changes in this MBIE consultation on postal services will further undermine the provision of this essential public service and have major social and economic ...2 days ago

- What I saw, sort of, at the emergency eye clinic

In a moment, the latest instalment of Once Again Dave Finds Himself in Hospital Even Though He Looks Quite Fit and Healthy Really, but first, a little bit of an insight into the way Ministers like Chris Penk and Casey Costello use data.Allow me to illustrate, using my own personal ...2 days ago

In a moment, the latest instalment of Once Again Dave Finds Himself in Hospital Even Though He Looks Quite Fit and Healthy Really, but first, a little bit of an insight into the way Ministers like Chris Penk and Casey Costello use data.Allow me to illustrate, using my own personal ...2 days ago - Bringing the House into disrepute

Last month we all thrilled to see Hana-Rawhiti Maipi-Clarke's haka in parliament in response to National's racist, anti-constitutional Treaty "Principles" Bill. Of course, the targets of that haka did not like someone speaking so forcefully and well against them - so they had Maipi-Clarke named and suspended from Parliament for ...2 days ago

- NZCTU urges political parties to vote down extreme anti-worker bill

NZCTU Te Kauae Kaimahi Acting President Rachel Mackintosh is calling on political parties to vote down Brooke van Velden’s Employment Relations (Pay Deductions for Partial Strikes) Amendment Bill, as it would undermine the ability of workers to engage in industrial action and may even lead to workers losing pay for ...2 days ago

- Atlas Network? Yawn.

One of the most compelling articles I’ve read about Atlas Network is from The Guardian columnist George Monbiot. His article is titled: “What links Rishi Sunak, Javier Milei and Donald Trump? The shadowy network behind their policies.”It’s an excellent summation outlining the strategies and modus operandi of the Atlas Network, ...2 days ago

One of the most compelling articles I’ve read about Atlas Network is from The Guardian columnist George Monbiot. His article is titled: “What links Rishi Sunak, Javier Milei and Donald Trump? The shadowy network behind their policies.”It’s an excellent summation outlining the strategies and modus operandi of the Atlas Network, ...2 days ago - Tuesday 10 December

Government has introduced legislation under urgency to allow employers to deduct workers pay for engaging in partial strikes, which will give further power to bosses to intimidate workers and will lead to the escalation of industrial disputes. NZNO workers begin rolling strikes in Auckland today, in their latest round of ...2 days ago

- As renewables rise, the world may be nearing a climate turning point

This is a re-post from Yale Climate Connections Climate pollution caused by burning fossil fuels hit a record 37.4 billion metric tons in 2024, marking a 0.8% rise from the previous year – and dashing hopes that a peak in global emissions might occur this year. That’s according to ...2 days ago

- Govt eyes ‘PPP-lite’ for health centres

Wellington’s Children’s Hospital under construction in 2018, largely funding by a philanthropic donation. Now there are fears of a type of creeping privatisation within the health system, starting with buildings. Photo: Lynn Grieveson Mōrena. Long stories short, the six things that matter in Aotearoa’s political economy around housing, climate and ...2 days ago

- Book Review: The Future Embraced

This is a guest post by George Weeks, reviewing a book called The Future Embraced by Kobus Mentz The Future Embraced is more than a book. It is an accumulation of 50 years of work, 13 years in the making. It takes the tone of a mentor, reflecting the accumulated ...2 days ago

- Dream Scenario

2023, directed by Kristoffer Borgli Dream Scenario is a movie about a mild-mannered (read: kind of pathetic and outright whiny) professor played by a nigh on unrecognisable to me Nicolas Cage who suddenly starts appearing in people’s dreams. At first he’s not doing anything other than just watching, failing to ...2 days ago

2023, directed by Kristoffer Borgli Dream Scenario is a movie about a mild-mannered (read: kind of pathetic and outright whiny) professor played by a nigh on unrecognisable to me Nicolas Cage who suddenly starts appearing in people’s dreams. At first he’s not doing anything other than just watching, failing to ...2 days ago - How Fed Farmers is driving Willis’s campaign against the banks

The pressure on the retail banks might only be just starting.Finance Minister Nicola Willis yesterday announced that she was changing the Reserve Bank remit to make it more pro-active in encouraging competition within the retail bank sector.And, Federated Farmers, who have been a major prod in the government’s side over ...2 days ago

- Poll number 4: Dead Govt Walking

..Thanks for reading Frankly Speaking ! Subscribe for free to receive new posts and support my work.RNZ reports the latest TVNZ/Verian Poll results:National: 37%, n/c (46 seats)Labour: 29%, n/c (36 seats)Greens: 10%, -2% points (12 seats)ACT: 8%, n/c (10 seats)Te Pāti Māori: 7%, up 3% (9 seats)NZ First: 6%, -1% ...3 days ago

..Thanks for reading Frankly Speaking ! Subscribe for free to receive new posts and support my work.RNZ reports the latest TVNZ/Verian Poll results:National: 37%, n/c (46 seats)Labour: 29%, n/c (36 seats)Greens: 10%, -2% points (12 seats)ACT: 8%, n/c (10 seats)Te Pāti Māori: 7%, up 3% (9 seats)NZ First: 6%, -1% ...3 days ago - Guest post!

David has, unfortunately, been losing pieces of himself and turns out it’s a bit hard to write a column when the affected parts are your eyeballs and it’s painful to read, so I offered to add to his pain by writing a guest column for him and the fool said ...3 days ago

David has, unfortunately, been losing pieces of himself and turns out it’s a bit hard to write a column when the affected parts are your eyeballs and it’s painful to read, so I offered to add to his pain by writing a guest column for him and the fool said ...3 days ago - Climate Change: An alternative plan

The government is supposed to release its second Emissions Reduction Plan any day now, and if its anything like the draft, it will be a pile of false accounting and wishful thinking, which will do nothing to actually reduce emissions. The central problem here is that national is legally required ...3 days ago

- Monday 9 December

The families of two workers killed in the forestry industry are pushing for a boss connected to both deaths to be pushed out of the industry, highlighting the need for corporate manslaughter legislation. Politicians are heading to Tokoroa to attend the Save Our Mill meeting regarding the significant proposed job ...3 days ago

- Climate Change: Sabotaging the Climate Commission

Throughout its term in government National has been annoyed by repeated unwelcome advice from He Pou a Rangi Climate Change Commission to move faster, do more, or even just do something. But Rod Carr's term as commission chair expired over the weekend, as did those of two other board members. ...3 days ago

- I Put A Spell On You

You know I can't stand itYou're running aroundYou know better, daddyI can't stand it 'cause you put me downOh, noI put a spell on youBecause you're mineSongwriter: Jay Hawkins.Please note that there is a paywall later in this newsletter, so before I begin, a reminder of my current offers and ...3 days ago

You know I can't stand itYou're running aroundYou know better, daddyI can't stand it 'cause you put me downOh, noI put a spell on youBecause you're mineSongwriter: Jay Hawkins.Please note that there is a paywall later in this newsletter, so before I begin, a reminder of my current offers and ...3 days ago - A Confession

Hi,I have a confession to make — I have been on holiday. I don’t really do holidays. They fill me with guilt. I need to be making something, or trying to make something. It’s all tied in with my sense of self worth, but we’ll get to that another day.I’ve ...3 days ago

Hi,I have a confession to make — I have been on holiday. I don’t really do holidays. They fill me with guilt. I need to be making something, or trying to make something. It’s all tied in with my sense of self worth, but we’ll get to that another day.I’ve ...3 days ago - Simeon Brown alienates another National electorate

Brown’s abrupt and ideological rulings have overturned locally driven plans and expectations and angered locals in yet another National electorate. Photo: Lynn GrievesonMōrena. Long stories short, the six things that matter in Aotearoa’s political economy around housing, climate and poverty on Monday, December 9 are:Warkworth residents are angry that Transport ...3 days ago

- Monday Wrap Up: Politics News

1. Anti-red tape ministry advises against anti-red tape bill (The Post, Andrea Vance)David Seymour's anti-red tape ministry says his new bill to slash red tape is unnecessary.An interim regulatory impact statement from [The Ministry of Regulation] said while it supports the overall objectives [of Seymour’s bill], it says the legislation ...3 days ago

1. Anti-red tape ministry advises against anti-red tape bill (The Post, Andrea Vance)David Seymour's anti-red tape ministry says his new bill to slash red tape is unnecessary.An interim regulatory impact statement from [The Ministry of Regulation] said while it supports the overall objectives [of Seymour’s bill], it says the legislation ...3 days ago - Simeon Brown’s fanaticism kills Warkworth intersection fix

I grew up in Warkworth, and the infamous Hill Street intersection has been an issue not just my whole life, but for decades before I was even born. My dad told me stories of how, back in the 80s, he’d set up seats overlooking the intersection and sit watching the ...3 days ago

- Gordon Campbell on the fall of Assad, and the new Dylan movie

Hold the champagne. Ugly and brutal as it was, the Assad regime may have been the lesser evil for Syria, the Middle East region and the rest of the world. The last time an extremist Sunni fighting force – called Islamic State (IS) – exerted control over large swathes of ...4 days ago

- 2024 SkS Weekly Climate Change & Global Warming News Roundup #49

A listing of 24 news and opinion articles we found interesting and shared on social media during the past week: Sun, December 1, 2024 thru Sat, December 7, 2024. Alternative listing prototype Instead of a "Story of the Week" we added a listing by assigned category, so this installment will ...4 days ago

- Mokopuna Thinking

Because the sky is blueIt makes me crySongwriters: Paul McCartney / John Lennon.This morning, I went along to the launch of the Greens’ alternative plan for emissions reduction. Contrasting the coalition’s approach of burying their head in the sand and glowering “thou shalt not” at others who try to stop ...4 days ago

Because the sky is blueIt makes me crySongwriters: Paul McCartney / John Lennon.This morning, I went along to the launch of the Greens’ alternative plan for emissions reduction. Contrasting the coalition’s approach of burying their head in the sand and glowering “thou shalt not” at others who try to stop ...4 days ago - Are Lester Levy and Shane Reti “cooking the books?”

This news piece is important enough it serves as a recap of events:Please consider supporting my work if you can afford to.In July, after most Health NZ Board members had already resigned – many without notice and it was starting to look embarrassing for the sitting Government - Shane Reti ...5 days ago

This news piece is important enough it serves as a recap of events:Please consider supporting my work if you can afford to.In July, after most Health NZ Board members had already resigned – many without notice and it was starting to look embarrassing for the sitting Government - Shane Reti ...5 days ago - Watching the Tide

So I'm just gonna sit on the dock of the bayWatching the tide roll awayI'm sittin' on the dock of the bayWastin' timeSongwriters: Stephen Lee Cropper / Otis ReddingChristmas PartiesAs you might recall from yesterday’s newsletter, last night was Christmas Party time for the Rockels.One of the younger members of ...5 days ago

So I'm just gonna sit on the dock of the bayWatching the tide roll awayI'm sittin' on the dock of the bayWastin' timeSongwriters: Stephen Lee Cropper / Otis ReddingChristmas PartiesAs you might recall from yesterday’s newsletter, last night was Christmas Party time for the Rockels.One of the younger members of ...5 days ago - My Saturday Soliloquy for Dec 7

Mōrena. Long stories short, the six things that mattered in Aotearoa’s political economy around housing, climate and poverty in this week were:PM Christopher Luxon said his Goverment was ‘re-learning’ the austerity-infused economic lessons taught by former National Finance Minister Ruth Richardson in 1991, when she slashed spending to reduce public ...5 days ago

- TKP 26/50 solutions: A new home without a power bill

As part of The Kākā Project of 2026 for 2050 (TKP 26/50) and When The Facts Change ,I interviewed Octopus Energy Zero Bills Technical Director Nigel Banks from the UK about this week's launch in New Zealand of a partnership with Classic Homes to build new homes in Auckland1 with ...5 days ago

- A wellbeing economy is the only option!

I recently attended a conference organised by WEALL (Wellbeing Economy Alliance) Aotearoa. WEALL defines 'economy' differently from the current neoliberal approach and that is simply 'the way that we produce and provide for one another'. Attending this conference made me even more aware of how far we have drifted away ...6 days ago

- Interview with John Cook about misinformation and artificial intelligence

In March, John Cook met with Adam Ford from Science, Technology & the Future to talk about his work researching misinformation and how to counter it. The interview - published on October 10 - explored the complex and evolving landscape of climate misinformation, covering a range of topics including the different types ...6 days ago

- Economic Progress May Not Add To Wellbeing

How the Prospect Theory of Behavioural Economics Makes Economic Analysis DifficultBehavioural economics has been described as the most revolutionary thing which has happened to economics for ages. The notion that people do not behave like ‘rational economic men’ (women are mainly ignored) undermines the microeconomic foundations of the subject. Not ...6 days ago

How the Prospect Theory of Behavioural Economics Makes Economic Analysis DifficultBehavioural economics has been described as the most revolutionary thing which has happened to economics for ages. The notion that people do not behave like ‘rational economic men’ (women are mainly ignored) undermines the microeconomic foundations of the subject. Not ...6 days ago - National finds out

Since coming to power last year, National has viciously cut the public service, sacking nearly 10,000 public servants (to date). Those people weren't just doing nothing, and it was obviously going to have an impact on something other than the government's books. But while National's over-paid, privately-insured, and DPS-guarded Ministers ...6 days ago

- Lockout of disability workers before Christmas unacceptable

NZCTU Te Kauae Kaimahi Acting President Rachel Mackintosh is condemning the actions of disability support provider Te Roopu Taurima o Manukau Trust in deciding to respond to legitimate strike action by locking out their workers with just a few weeks before Christmas. “The actions of Te Roopu Taurima are totally ...6 days ago

- Friday 6 December

In another blow to the media landscape, Māori TV’s daily news service is set to end after 20 years, following the announcement that they have cut 27 jobs. PSA members at MBIE have voted to initiate industrial action, after rejecting a pay offer because it failed to keep up with ...6 days ago

- An experiment and our Christmas offer to subscribe to The Kākā

Photo: Lynn Grieveson / The KākāIt’s that time of the year when we offer 50% off for a year to new subscribers for the next fortnight until December 21, which is ‘Gravy Day’1. It’s our version of a Christmas/Black Monday/Cyber Monday/Singles Day/Boxing Day offer. We call it the ‘Gravy Day ...6 days ago

- The State of David Seymour’s Shameless Condescension and Unbridled Arrogance

.Thanks for reading Frankly Speaking ! Subscribe for free to receive new posts and support my work..Setting the stageQuestion: How does one make money, when something stands in the way?Answer: Get rid of that thing. Or at least dilute it.Present Day, Aotearoa New ZealandIn his Beehive media statement, Seymour recently ...6 days ago

.Thanks for reading Frankly Speaking ! Subscribe for free to receive new posts and support my work..Setting the stageQuestion: How does one make money, when something stands in the way?Answer: Get rid of that thing. Or at least dilute it.Present Day, Aotearoa New ZealandIn his Beehive media statement, Seymour recently ...6 days ago - Weekly Roundup 06-December-2024

It’s another Friday and it has been a big week in Auckland. We hope everyone’s excited to be in the final stretch of the year! Here’s some of the stories that have caught our attention this week. This post, like all our work, is brought to you by a largely ...6 days ago

- The Days Go By

It must be your skin, I'm sinkin' inIt must be for real, 'cause now I can feelAnd I didn't mind, it's not my kindIt's not my time to wonder whySongwriter: Gavin Rossdale.As the year winds up, I’m feeling a bit mentally drained, so today’s newsletter is one of reminiscing. Today, ...6 days ago

It must be your skin, I'm sinkin' inIt must be for real, 'cause now I can feelAnd I didn't mind, it's not my kindIt's not my time to wonder whySongwriter: Gavin Rossdale.As the year winds up, I’m feeling a bit mentally drained, so today’s newsletter is one of reminiscing. Today, ...6 days ago - The Hoon around the week to December 6

The podcast above of the weekly ‘Hoon’ webinar for paying subscribers on Thursday night features co-hosts & talking about the week’s news with: on Trade and Agriculture Minister Todd McClay saying New Zealand would not buy emissions credits overseas, effectively admitting we’ll renege on our Paris commitments. (RNZ) ...6 days ago

- Paying for National’s roads

The Government has promised 17 Roads of National Significance, but the brutal truth is that it cannot afford them. So Transport Minister Simeon Brown yesterday announced that from now on, tolls and other user charges will be the way New Zealand pays for new roading infrastructure. Tolls are likely ...6 days ago

- Confession: Why Shane Reti & Ayesha Verrall’s Performance Helps Me

Video above. These videos are also designed for those not versed in the detailed subject matter so excuse any repeats of Health NZ facts you are aware of from reading Mountain Tui for too long!Recently, I read a Substack article which, on my brief skim, lamented the rise of critiquing ...6 days ago

- Skeptical Science New Research for Week #49 2024

Open access notables Global emergence of regional heatwave hotspots outpaces climate model simulations, Kornhuber et al., Proceedings of the National Academy of Sciences: Multiple recent record-shattering weather events raise questions about the adequacy of climate models to effectively predict and prepare for unprecedented climate impacts on human life, infrastructure, and ecosystems. Here, we ...7 days ago

- The Bewildering World of Chris Luxon – Three Bad Polls – Three Strikes for National?

.Thanks for reading Frankly Speaking ! Subscribe for free to receive new posts and support my work..As I wrote on 3 December:“One bad poll for a government can be dismissed as “rogue”. Two? That’s damaging.”Three bad polls? That is when Red Alert lights start flashing; klaxons start to blare; and ...7 days ago

.Thanks for reading Frankly Speaking ! Subscribe for free to receive new posts and support my work..As I wrote on 3 December:“One bad poll for a government can be dismissed as “rogue”. Two? That’s damaging.”Three bad polls? That is when Red Alert lights start flashing; klaxons start to blare; and ...7 days ago - Climate Change: More unwelcome advice

He Pou a Rangi / Climate Change Commission has just released its Review of the 2050 emissions target including whether emissions from international shipping and aviation should be included. After noting that there have been significant changes since the target was originally set in 2019 - stronger evidence that we ...7 days ago

- Join us at 5pm for The Hoon

7 days ago

7 days ago - No sweat

Let's say I want to run a marathon, but I’m not keen on all that running.At the registration desk I say, I want to start at the last kilometre. What's the fee for that?They tell me,We don't offer that option. You have to do the whole race.I reply,Yeah but I ...7 days ago

Let's say I want to run a marathon, but I’m not keen on all that running.At the registration desk I say, I want to start at the last kilometre. What's the fee for that?They tell me,We don't offer that option. You have to do the whole race.I reply,Yeah but I ...7 days ago - Climate Change: National wants to cheat on Paris II

Back in September, Climate Change Minister Simon Watts shocked us by suggesting that New Zealand could refuse to meet its international commitments under the Paris Agreement. Now Forestry Minister Todd McClay has echoed that position: Minister for Agriculture and Forestry Todd McClay says the Government won't be buying carbon ...7 days ago

- Marsden Fund changes will undermine prosperity and social cohesion

The Government’s rewrite of the Marsden Fund’s investment plan and terms of reference demonstrates a complete lack of understanding and risks undermining the breadth of research that is essential for the wellbeing and prosperity of New Zealanders, said NZCTU Te Kauae Kaimahi Acting President Rachel Mackintosh. “Humanities and social science ...1 week ago

- Thursday 5 December

The Government has announced further changes to the personal grievance regime that will make it even tougher for workers, and changes to the Marsden Fund investment plan to stop funding for humanities and social sciences research. Workers at Kinleith mill are worried that they will lose even more jobs. A ...1 week ago

- Can desalination quench agriculture’s thirst?

This article by Lela Nargi originally appeared in Knowable Magazine, a nonprofit publication dedicated to making scientific knowledge accessible to all. Sign up for Knowable Magazine’s newsletter. Ralph Loya was pretty sure he was going to lose the corn. His farm had been scorched by El Paso’s hottest-ever June and ...1 week ago

{kind=link}

- Release: National Party urged to support modern slavery legislation

Labour is urging the Prime Minister to walk the talk and support legislation combating modern slavery. ...6 hours ago

Labour is urging the Prime Minister to walk the talk and support legislation combating modern slavery. ...6 hours ago - Release: Labour has lost confidence in the Speaker

The Speaker of the New Zealand Parliament made an unprecedented decision on the government amendment to the Fast Track Approvals Bill last night. ...6 hours ago

- One year on, still no progress on new ferries

Today’s announcement from the Government on its plan for new ferries throws more uncertainty on the future of the country’s rail network. ...1 day ago

Today’s announcement from the Government on its plan for new ferries throws more uncertainty on the future of the country’s rail network. ...1 day ago - Release: Nicola Willis’ smaller ferries will cost more

After wasting a year, Nicola Willis has delivered a worse deal for the Cook Strait ferries that will end up being more expensive and take longer to arrive. ...1 day ago

- Bill to sanction unlawful occupation of Palestine

Green Party co-leader Chlöe Swarbrick has today launched a Member’s Bill to sanction Israel for its unlawful presence in the Occupied Palestinian Territory, as the All Out For Gaza rally reaches Parliament. ...1 day ago

- Release: Labour fully supports greyhound racing ban

The Government has done the right thing in moving to ban greyhound racing. ...2 days ago

- Greyhound racing industry ban marks new era for animal welfare

After years of advocacy, the Green Party is very happy to hear the Government has listened to our collective voices and announced the closure of the greyhound racing industry, by 1 August 2026. ...2 days ago

- Rangatahi voices must be centred in Government’s Relationship and Sexuality Education refresh

In response to a new report from ERO, the Government has acknowledged the urgent need for consistency across the curriculum for Relationship and Sexuality Education (RSE) in schools. ...2 days ago

- Govt introduces archaic anti-worker legislation

The Green Party is appalled at the Government introducing legislation that will make it easier to penalise workers fighting for better pay and conditions. ...3 days ago

- Winston Peters – Kinleith Mill Speech

Thank you for the invitation to speak with you tonight on behalf of the political party I belong to - which is New Zealand First. As we have heard before this evening the Kinleith Mill is proposing to reduce operations by focusing on pulp and discontinuing “lossmaking paper production”. They say that they are currently consulting on the plan to permanently shut ...3 days ago

Thank you for the invitation to speak with you tonight on behalf of the political party I belong to - which is New Zealand First. As we have heard before this evening the Kinleith Mill is proposing to reduce operations by focusing on pulp and discontinuing “lossmaking paper production”. They say that they are currently consulting on the plan to permanently shut ...3 days ago - Swarbrick calls on Auckland Mayor to end delay of revival of St James Theatre

Auckland Central MP, Chlöe Swarbrick, has written to Mayor Wayne Brown requesting he stop the unnecessary delays on St James Theatre’s restoration. ...4 days ago

- He Ara Anamata: Greens launch Emissions Reduction Plan

Today, the Green Party of Aotearoa proudly unveils its new Emissions Reduction Plan–He Ara Anamata–a blueprint reimagining our collective future. ...4 days ago

- Fossil fuel lobbyist appointment to EECA board called out

The Green Party condemns the Government’s appointment of a fossil fuel lobbyist to the Energy Efficiency & Conservation Authority Board. ...6 days ago

- Release: Boot camps must be shut down today

The Prime Minister has committed to shut down his government’s boot camps if there is evidence of harm to children – so he must do that today. ...6 days ago

- Greens echo OECD call for electricity market reform

The Green Party has welcomed the OECD urging the Government to re-examine separating ‘gentailers’ to make a fairer electricity market for New Zealanders. ...6 days ago

- Release: Govt breaks Auckland housing promise

Housing Minister Chris Bishop has confirmed National has broken yet another election promise. ...1 week ago

- Government smokescreen to downgrade climate ambition

Today the ACT-National Coalition Agreement pet project’s findings on “no additional warming” were released. ...1 week ago

- Release: Health NZ admits errors led to claimed deficit

Health New Zealand has exaggerated its deficit to justify job cuts. ...1 week ago

- Release: More cuts to research, science and innovation sector

The Government’s latest round of cuts to research and innovation targets the long-established and successful Marsden Fund. ...1 week ago

- Govt guts funding for social sciences and humanities

The Government’s decision to axe all Humanities and Social Science research funding through the Marsden Fund is a massive step backwards. ...1 week ago

- You can’t bank on pine trees in a climate crisis

Today’s Government announcement to limit farm forestry conversions tinkers around the edges, instead of focusing on the real problem and stopping pollution at the source. ...1 week ago

- Release: Nicola Willis being sneaky with new taxes

Nicola Willis is refusing to rule out putting sneaky new taxes on Kiwi households. ...1 week ago

- Release: Govt benefit target even further out of reach

Christopher Luxon has once again failed to read the room and claimed success while life gets harder for everyday Kiwis. ...1 week ago

- Govt continues to punch down

The Government’s new initiative to get people off the benefit won’t address the core drivers of poverty such as low incomes, lack of access to adequate housing and lack of employment opportunities. ...1 week ago

- Release: Labour urges ACC to pull investments in Israel’s illegal settlements

Labour is urging ACC to divest from companies identified by the United Nations as complicit in the building and maintenance of Israel’s illegal settlements in the Occupied Palestinian Territories. ...1 week ago

- Release: Further evidence to stop school lunch cuts

A new report provides further proof that David Seymour should not be messing with the free school lunch programme. ...1 week ago

- Jamie Arbuckle: Inquiry into Banking Competition

This week was the start of the bank inquiry hearings into banking competition. The inquiry was confirmed in the NZ First/National Coalition agreement. 140 submissions were received on the inquiry, and we will hear from over 60 submitters including all the major banks. ANZ, New Zealand's largest bank, was first ...1 week ago

- Casey Costello: What Once Was…

Entering politics is a privilege afforded to very few and, as the saying goes, with great power comes great responsibility. Being an MP is a call to service. Whatever your politics you have a duty to show up. Whatever your party's policy, you have made a promise to those who ...1 week ago

- Casey Costello: International Day of Older Persons

Throughout New Zealand it is difficult to think of a sports club, charity, church group, festival, foundation, or service organisation that does not owe its existence, effectiveness, or success to the contribution of older New Zealanders. October 1st is International Day of Older Persons so please take a moment to consider ...1 week ago

- NZ First Member’s Bill To Disestablish Auckland Transport

Today New Zealand First has introduced a Member’s Bill that will restore democratic control over transport management in Auckland City by disestablishing Auckland Transport (AT) and returning control to Auckland Council. The ‘Local Government (Auckland Council) (Disestablishment of Auckland Transport) Amendment Bill’ intends to restore democratic oversight, control, and accountability ...1 week ago

- Mark Patterson: Farmers understand we have their backs

Spring is here which means the start of the A&P show season. Those treasured community days where town meets country. There's no rural-urban divide here, just a chance to meet up with family and old friends and celebrate all things that make rural New Zealand so special. I'm embarking on ...1 week ago

- Tanya Unkovich: It’s time to start the debate on palliative care as a ‘right’

There is one topic that is the great human leveller, and that is of death and dying. One day, we will all have to face it, and I am of the belief that being able to pass away with grace and dignity is a vital, basic, human right. How we ...1 week ago

- Release: A Labour Government will not join AUKUS

New Zealand will not sign up to the nuclear-powered pillar one, or the pillar two of AUKUS under a Labour Government. ...2 weeks ago

- Release: Labour will build Dunedin Hospital

Labour will build Dunedin Hospital as it was committed to prior to election 2023. ...2 weeks ago

- Chris Hipkins: Speech to Labour Party Conference 2024

E ngā mana, e ngā reo, e ngā iwi, e rau rangatira ma Tena koutou tēnā koutou tēnā koutou katoa ...2 weeks ago

- Luxon Folds on ACT’s Treaty Principles Bill

Te Pāti Māori Co-Leader, Debbie Ngarewa-Packer, is calling Luxon’s leadership a joke after it was revealed this morning on Q+A that ACT’s Treaty Principles Bill was not a bottom line. "New Zealand officially has a laughing-stock Prime Minister whose leadership folded as he trades away the rights of tangata whenua ...2 weeks ago

- Prime Minister shirks responsibility on global climate commitment

In an interview with Q&A this morning, the Prime Minister refused to say whether he would commit to meeting the Paris Agreement, the international climate agreement which commits all countries to act locally to keep global warming below 1.5 degrees. ...2 weeks ago

- Release: All workers deserve fair treatment

The Government’s latest change to the Employment Relations Act has no justification apart from making it easier to sack employees without having to follow due process. ...2 weeks ago

- COURT OF APPEAL RULING: SFO METHODS “OVERREACH, UNLAWFUL, OPPRESSIVE”

Today the Court of Appeal has found the Serious Fraud Office has been acting indiscriminately and unlawfully throughout an eight year long investigation. The SFO has shown their incompetence and arrogance and shown to be abusing their authority to conduct its own overreaching and unlawful fishing expeditions. The Court of Appeal said the SFO has relied on its misuse of compulsory interview ...2 weeks ago

- Covid Inquiry report underlines need to invest in Health

The Green Party says the report from the Royal Commission of Inquiry into the Covid-19 Response underlines the need for proper investment in our health system so we are prepared for future pandemics. ...2 weeks ago

- Karen Walker and Keven Mealamu join CNZ Board

Fashion designer Karen Walker CNZM and former All Black Keven Mealamu MNZM have been appointed to the Creative New Zealand Board, Arts Minister Paul Goldsmith says. “I am excited to have these two highly respected individuals join Creative New Zealand, who will undoubtedly add great experience and perspectives to New ...1 hour ago

Fashion designer Karen Walker CNZM and former All Black Keven Mealamu MNZM have been appointed to the Creative New Zealand Board, Arts Minister Paul Goldsmith says. “I am excited to have these two highly respected individuals join Creative New Zealand, who will undoubtedly add great experience and perspectives to New ...1 hour ago - Health targets encouraging – work continues

New data shows that the Government’s focus on health targets is putting the brakes on the steep decline in delivery seen over the past five years. Health Minister Dr Shane Reti says while there is much more work to do, health target results in the three months to 30 September ...1 hour ago

- Independent review of ACC announced

ACC Minister Matt Doocey has today announced an independent review of ACC because of concerns about declining rehabilitation rates and increasing costs. “ACC provides critical support to New Zealanders in times of need, but I am concerned that ACC’s performance has been declining for a decade. Rehabilitation rates are down, ...3 hours ago

- New research to aid tourism and hospitality sector

Tourism and Hospitality Minister Matt Doocey today announced investment in a suite of new surveys and research which will help fill critical gaps in tourism and hospitality sector data. “Government investment totalling around $3 million will fund essential research including a domestic visitor survey, tourism sentiment survey, new research into ...5 hours ago

- Seafood sector a ‘Kiwi success story’

New Zealand’s seafood exports are set to hit a record $2.2 billion in the year to June 2025, and increase to $2.4b the following year, Oceans and Fisheries Minister Shane Jones says. “Our seafood sector is a Kiwi success story. The sector’s hard work, healthy demand, tight global supply and ...6 hours ago

- Food and Fibre sector set to break records

New Zealand’s food and fibre exports are forecast to hit $56.9 billion by 30 June 2025 and climb to a record $58.3 billion the following year, showcasing the strength and resilience of the sector, Agriculture and Forestry Minister Todd McClay announced today. “The hard work and innovation of our world ...8 hours ago

- Thai Foreign Minister to visit

Thailand’s Foreign Minister Maris Sangiampongsa will visit New Zealand this week, Foreign Minister Winston Peters has announced. “Thailand is an important economic and security partner for New Zealand in Southeast Asia,” Mr Peters says. “The visit is another important step as our two countries work to lift our relationship to a ...22 hours ago

- New ferries will ensure safe, resilient connection

The Government is establishing a new company to procure two new ferries to ensure a safe, reliable and commercially viable ferry service, Finance Minister Nicola Willis says. “This decision will ensure New Zealand has a safe, reliable and resilient service to move people and freight between the North and South ...1 day ago

- Milestone for Iwi Māori Partnership Boards

Health Minister Dr Shane Reti says Iwi Māori Partnership Boards have taken a major step as part of the Government’s commitment to the health of Māori communities. Minister Reti has now received 15 IMPB community health plans, representing the vision and plans of the boards for health and wellbeing in ...1 day ago

- New seafood processing factory opens in Porirua

A new seafood processing factory in Porirua north of Wellington will bring export revenue, jobs and opportunities for the community, Oceans and Fisheries Minister Shane Jones says. The Wellington Kaimoana Hub, a joint venture between Māori owned seafood companies Moana New Zealand and Port Nicholson Fisheries, was formally opened by ...1 day ago

- Gisborne receives mental health beds boost

Minister for Mental Health Matt Doocey today opened Gisborne Hospital’s new acute mental health unit, Te Whare Awhi Ora, and says the region will be better served by a bigger, more therapeutic acute mental health unit.“I have been clear that we need to build a strong mental health and addiction ...1 day ago

- Our journey towards net zero

The Government has unveiled its second Emissions Reduction Plan, outlining a path to keep New Zealand on track to meet its climate change targets while supporting the economy to thrive, Climate Change Minister Simon Watts says. “The plan sets the foundation to meet our net zero 2050 target as early ...1 day ago

- Repealing advertising restrictions for media

Legislation that will repeal all advertising restrictions for broadcasters on Sundays and public holidays has been introduced to Parliament today, Media Minister Paul Goldsmith says. “Traditional media outlets are operating in an extremely difficult environment and as the Government we must ensure regulatory settings are enabling the best chance of ...2 days ago

- Government announces future of greyhound racing in New Zealand

Racing Minister Winston Peters has announced the Government’s plans to end greyhound racing in New Zealand. “This is not a decision that is taken lightly but is ultimately driven by protecting the welfare of racing dogs. “Despite significant progress made by the greyhound racing industry in recent ...2 days ago

- Government cuts red tape for food exporters

The Government is delivering on its commitment to cut red tape and increase the value of exports by making it easier for exporters to deliver safe New Zealand food to more markets, says Food Safety Minister Andrew Hoggard. “Food exports are the bedrock of our economy, so when industry asked ...2 days ago

- Relationships & Sexuality Education refresh

The Government welcomes a new report which confirms the way Relationship and Sexuality Education (RSE) is taught in schools isn’t fit for purpose, Education Minister Erica Stanford says. “In a world that’s rapidly changing, young people deserve every opportunity to be equipped with the knowledge and skills they need to ...2 days ago

- Applications open for mental wellbeing campaigns

Mental Health Minister Matt Doocey announced that applications will open today for the $5 million Mental Health Promotion Fund for organisations to run campaigns that promote mental wellbeing while at the Digital Mental Health Summit. “Strengthening the focus on prevention and early intervention is one of my key priorities. Our ...2 days ago

- Raising the visibility of New Zealand’s ethnic communities

A first-of-its-kind report launched today lays the groundwork for growing the visibility of New Zealand’s ethnic communities through data, Ethnic Communities Minister Melissa Lee says. “Too often and for too long, ethnic communities have largely been invisible in public sector data. As a result, their voices have not always been ...3 days ago

- Pay deductions for partial strikes to be reintroduced

Changes to collective bargaining will help rebalance the rights and consequences of industrial action, Workplace Relations and Safety Minister Brooke van Velden says. A bill to allow for pay deductions in response to partial strikes will be introduced today. “Partial strikes are industrial actions that normally involve turning up to ...3 days ago

- Strategic leasing another tool in the infrastructure procurement belt

The Government is issuing strategic leasing guidance to agencies to ensure more efficient use of taxpayer dollars where the private sector is better placed to own and maintain infrastructure, Infrastructure Under-Secretary Simon Court says. “On a basic level, strategic leasing is like any other government leasing arrangement, where the government ...3 days ago

- Next steps for banking competition

The Government is pushing ahead with moves to increase banking competition by boosting Kiwibank and taking steps to ensure the Reserve Bank places greater importance on competition in the sector, Finance Minister Nicola Willis says. “The change will enable the New Zealand-owned bank to more vigorously compete against the ...3 days ago

- New campaign promotes alcohol-free pregnancies

Health Minister Dr Shane Reti has launched a new public health campaign to prevent fetal alcohol spectrum disorder by promoting alcohol-free pregnancies. FASD is the leading cause of preventable intellectual and neurodevelopmental disorders in New Zealand, causing lifelong physical, behavioural, learning and mental health problems. “The impact of FASD in ...3 days ago

- New Climate Change Commission Chair appointed

Rt Hon Dame Patsy Reddy has been appointed as the new chair of the Climate Change Commission, the independent Crown entity that provides the Government advice, monitoring and reporting to support New Zealand’s transition to a climate-resilient, low emissions future, Climate Change Minister Simon Watts says. “I’m pleased that Dame ...3 days ago

- Commonsense changes to insulation standards

The Government is proposing commonsense changes to reduce the upfront cost of building, while maintaining robust energy efficiency standards, Building and Construction Minister Chris Penk says. “We know from a social investment point of view that Kiwis do much better when they have access to affordable, insulated, secure housing. “However, ...3 days ago

- Racing Act changes to boost racing industry sustainability

Racing Minister Winston Peters has announced the introduction of legislation to amend the Racing Industry Act 2020 which will extend TAB NZ’s current land-based monopoly for sports and racing betting to online. The Racing Industry Act established TAB NZ for the purposes of funding the racing industry. It provides ...4 days ago

- New members appointed to EECA Board

Energy Minister Simeon Brown has today announced two new appointments to the Energy Efficiency & Conservation Authority (EECA) Board.John Carnegie and Vijay Goel have both been appointed as members for three-year terms which will begin on 6 January 2025 and end on 5 January 2028.“As Minister for Energy, my goal ...6 days ago

- JOINT STATEMENT ON AUSTRALIA-NEW ZEALAND FOREIGN AND DEFENCE MINISTERIAL CONSULTATIONS (ANZMIN) DECE...

1. Deputy Prime Minister and Minister of Foreign Affairs Rt Hon Winston Peters MP and Minister of Defence Hon Judith Collins KC MP hosted Australian Deputy Prime Minister and Minister for Defence the Hon Richard Marles MP and Minister for Foreign Affairs Senator the Hon Penny Wong on 6 December in ...6 days ago

- Swift avian influenza response in Otago on track

Biosecurity Minister Andrew Hoggard says good progress is being made in the response to the detection of high pathogenicity avian influenza (HPAI) in Otago, but there is more work to do. “Rigorous testing and monitoring continue to show no confirmed signs of the disease in chicken farms outside of Mainland ...6 days ago

- Funding for Hawke’s Bay water security project

Up to $3 million from the Regional Infrastructure Fund has been allocated for pre-construction development of the Tukituki Water Security Project in Hawke’s Bay, Regional Development Minister Shane Jones says. The grant for the project, which is being co-funded by the Tukituki Water Security Project, is limited to work to ...6 days ago

- Waimārama ban on taking pāua to continue

A two-year temporary closure banning the take of pāua from Waimārama south of Hastings will support efforts by local iwi to rebuild pāua stocks, Oceans and Fisheries Minister Shane Jones says. The closure includes Waimārama Beach and Ocean Beach, two beaches popular with holidaymakers and recreational fishers. Ngāi Hapū o ...6 days ago

- Appointments to the New Zealand Post board

Four new appointments have been made to the New Zealand Post Ltd (NZ Post) board, Acting State-Owned Enterprises Minister Chris Bishop says. “NZ Post is one of New Zealand’s largest State-owned enterprises with revenue of around $1.2 billion and total assets of around $1.5 billion. It is the designated universal ...6 days ago

- Government to partner with private sector to plant trees on low value Crown land

Ministers responsible for Climate Change, Forestry, Conservation and Land Information today announced that Cabinet has agreed to explore public-private partnerships to plant trees on Crown land, supporting New Zealand’s climate change targets and creating more jobs. Climate Change Minister Simon Watts says that nature-based solutions is a key part to ...7 days ago

- International data confirms maths transformation

New international data validates the Government’s plan to transform maths education in New Zealand, Education Minister Erica Stanford says. “The Trends in International Mathematics and Science Study (TIMSS) is the longest-running, large-scale international assessment of mathematics and science and takes place every four years. While 2023 results show an improved ...7 days ago

- Government partners to boost rural productivity in Hawke’s Bay

The Government is partnering with Hawke’s Bay farmers and the Regional Council to improve farm productivity and build resilience against adverse weather events, Minister of Agriculture Todd McClay announced today at a ceremony in Hawke’s Bay. “The Government is co-investing $995,000 to grow the Land for Life (LFL) pilot programme ...7 days ago

- Peters visit to New Caledonia concludes

Foreign Minister Winston Peters has completed his visit to New Caledonia, New Zealand’s closest neighbour. “Over the last few days, we have listened to and learned from a wide range of people in New Caledonia - so that we can better understand the acute challenges it faces,” Mr Peters says. ...7 days ago

- More charter schools to open Term 1 2025 announced

Associate Education Minister David Seymour has today announced that Christchurch North College, The BUSY School, Te Rito, Te Kura Taiao, Ecole Francaise Internationale Auckland and North West Creative Arts College will open in term one 2025 as charter schools. “This announcement is another significant step in the Government’s efforts to ...1 week ago

- New chair appointed to Heritage New Zealand

Dame Jo Brosnahan DNZM QSO has been appointed chair of the Heritage New Zealand Board, Arts Minister Paul Goldsmith says. “Dame Jo has extensive governance and business experience which has been recognised in various Honours, notably in 2023 when she was made a Dame Companion of the New Zealand Order ...1 week ago

- Survey results to drive change for tourism and hospitality workforce

Tourism and Hospitality Minister Matt Doocey has welcomed the data released today about the hospitality and tourism workforce. “Two of my key priorities include supporting the people who make up the tourism and hospitality workforce and growing the value of international tourism. In order to grow New Zealand’s international tourism ...1 week ago

- Upgrading substations to improve reliability for Wellington metro rail

Wellington commuters will benefit from a $137.2 million funding boost that will deliver long overdue upgrades to substations on the city’s metro rail network and improve the reliability of services, Transport Minister Simeon Brown says.“Our Government is committed to delivering infrastructure that reduces congestion, boosts productivity to support economic growth, ...1 week ago

- Record $434 million in community grants from Lotto NZ

Minister of Internal Affairs Brooke van Velden says Lotto NZ has granted $434 million to the community in the past financial year, an increase of 15 percent from the previous year. “It’s fantastic to see an increase in funding going to important community projects, providing opportunities for New Zealanders to ...1 week ago

- A love letter to community newspapers

Bethany Rolston looks back at the three years she wrote for the Te Awamutu Courier, one of the 14 NZME community newspapers set to close before Christmas. Looking back at the three years I was a journalist at the Te Awamutu Courier feels like a happy sort of fever ...29 minutes ago

Bethany Rolston looks back at the three years she wrote for the Te Awamutu Courier, one of the 14 NZME community newspapers set to close before Christmas. Looking back at the three years I was a journalist at the Te Awamutu Courier feels like a happy sort of fever ...29 minutes ago - Politics with Michelle Grattan: For Mark Dreyfus, antisemitism is very personal

Source: The Conversation (Au and NZ) – By Michelle Grattan, Professorial Fellow, University of Canberra The attack on the Adass Israel synagogue in Melbourne and another car torching in Sydney have dramatically heightened political tensions over antisemitism. Amid criticism the government has been too slow to act in the ...43 minutes ago

Source: The Conversation (Au and NZ) – By Michelle Grattan, Professorial Fellow, University of Canberra The attack on the Adass Israel synagogue in Melbourne and another car torching in Sydney have dramatically heightened political tensions over antisemitism. Amid criticism the government has been too slow to act in the ...43 minutes ago - Disaster happens when soldiers don’t act ethically. We can provide better training to support the...

Source: The Conversation (Au and NZ) – By Deane-Peter Baker, Associate Professor of Ethics, Director of UNSW Military Ethics Research Lab and Innovation Network (MERLIN), UNSW Sydney Recently, the government responded to the Royal Commission into Veteran Suicide. It adopted most of the recommendations designed to better support defence personnel. ...43 minutes ago

- Fiji government accused over human rights violations, free speech curb

By Apenisa Waqairadovu in Suva Fiji’s coalition government has come under scrutiny over allegations of human rights violations. Speaking at the commemoration of International Human Rights Day in Suva on Tuesday, the chair of the Coalition of NGOs, Shamima Ali, claimed that — like the previous FijiFirst administration — the ...1 hour ago

- Winston Peters says rail-enabled ferries are ‘no-brainer’ for Interislander replacements

"The overall cost in my view will be much less if it's rail-enabled," new Minister for Rail says, as he confirms there's no getting out of a break-fee for the iRex project. ...1 hour ago

"The overall cost in my view will be much less if it's rail-enabled," new Minister for Rail says, as he confirms there's no getting out of a break-fee for the iRex project. ...1 hour ago - Iwi leader ‘cuts out middle man’ with open letter to King Charles III

He said Charles is a direct descendant of Queen Victoria - the reigning monarch at the time the treaty was signed - and had the mana to intervene. ...2 hours ago

- Watch live: Christopher Luxon faces questions after ferry announcement

The Prime Minister's comments come a day after the government announced its alternative ferry replacement project, which has been criticised for a lack of specific detail. ...2 hours ago

- Solicitor-General reissues prosecution guidelines after backlash

"I realised that I could have done better with the way that I had worded that particular part," Solicitor-General Una Jagose told politicians after backlash. ...2 hours ago

- Review into ACC announced, levies to increase

The ACC minister announced an independent review, while levies are to rise by 5 percent a year for three years. ...2 hours ago

- Deliberate disinformation campaigns are a public health risk – but NZ has no effective strategy to...

Source: The Conversation (Au and NZ) – By Helen Petousis-Harris, Associate Professor in Vaccinology, University of Auckland, Waipapa Taumata Rau Shutterstock/Melnikov Dmitriy The recently released Royal Commission of Inquiry report about New Zealand’s COVID response highlights the harmful impact of misinformation and disinformation on public health. While ...2 hours ago

- The Spinoff’s best NZ book covers of 2024

In which Claire Mabey judges this year’s New Zealand books by their covers. Among a sea of books some are more alluring than others, like tropical fishes glinting. The art of the book cover is a serious matter: the cover has to help the book stand out as well as ...2 hours ago

- Will Taxpayer Bailouts Of Failing Skifield Never End?

“It’s time for the abuse of taxpayer money to stop, and start investing in things that will actually benefit hardworking Kiwis.” ...3 hours ago

“It’s time for the abuse of taxpayer money to stop, and start investing in things that will actually benefit hardworking Kiwis.” ...3 hours ago - Hundreds more jobs set to go at Health New Zealand

Two more units are facing major cuts, RNZ understands. ...3 hours ago

- Modern Slavery Legislation Drafted To Drive Cross Party Political Support For NZ Law

A team of independent experts has drafted legislation ready for immediate introduction to Parliament in a bid to fast-track progress on modern slavery laws with cross-party backing. ...4 hours ago

- A brief history of celebrity cameos on Shortland Street

Ahead of Conan O’Brien’s Shortland Street cameo tonight, Alex Casey looks back at some of the more memorable cameos to grace Ferndale. Nothing signals the festive season better than a tall redhead American late show host visiting our favourite fictional hospital. Tonight, Conan O’Brien will don a pair of grape ...4 hours ago

- Bypass property negotiation sours over price dispute

Paul Hoglund says he's been offered less than his property is worth and he isn't going anywhere. "I've got nothing to lose". ...4 hours ago

- David Seymour wrong on cost of ferry replacement project, says Winston Peters

"He's wrong on the figures that he's used, he's wrong on the question of privatisation and he's wrong on the question of what it's going to cost," the new rail minister says. ...5 hours ago

- ‘A virtual seat at the family table’: why older people are among the biggest users of social med...

Source: The Conversation (Au and NZ) – By Bernardo Figueiredo, Associate Professor of Marketing, RMIT University Andrii Iemelianenko/Shutterstock The Australian government’s recent decision to ban under 16s from social media has focused attention on the harms it can cause – especially for young people. But young people are ...5 hours ago

- These 3 simple actions can save you money and help make the most of your rooftop solar

Source: The Conversation (Au and NZ) – By Dani Alexander, CEO, UNSW Energy Institute, UNSW Sydney Shutterstock Four million Australian households and businesses have rooftop solar installed, making us the world leader in the technology. Much of the electricity generated is used to power our homes, and any ...5 hours ago

- Help Me Hera: How do I navigate Auckland traffic without going insane?

The selfishness of this city’s drivers never fails to ruin my day. How do I get from A to B without wishing punishment and retribution on my fellow commuters? Want Hera’s help? Email your problem to helpme@thespinoff.co.nz Help Me Hera! Why do I see Auckland driver behaviour (not letting people merge, tailgating, etc) ...5 hours ago

- Own goal? Govt sets new $4b goalpost for ferries

This new Number of the Day is based on 42 very, very costly words in an old Treasury report, and some ‘spotty’ costings out of China and Korea The post Own goal? Govt sets new $4b goalpost for ferries appeared first on Newsroom. ...5 hours ago

This new Number of the Day is based on 42 very, very costly words in an old Treasury report, and some ‘spotty’ costings out of China and Korea The post Own goal? Govt sets new $4b goalpost for ferries appeared first on Newsroom. ...5 hours ago - Family and sexual violence: Government’s action plan makes little progress

Nationwide efforts to combat family and sexual violence are not getting results, with government agencies blamed for poor access to services. ...6 hours ago

- Why Australian politicians are flocking to ‘Little Red Book’ to engage with Chinese voters

Source: The Conversation (Au and NZ) – By Wanning Sun, Professor of Media and Cultural Studies, University of Technology Sydney Runrun2/Shutterstock Wen Li, a graduate student living in Brisbane, ran for the seat of Mansfield as a Greens candidate in the recent Queensland election. Li promoted his policies on ...6 hours ago