Nats’ ACC plan only good for insurance companies and lawyers

Nats’ ACC plan only good for insurance companies and lawyers

Written By:

- Date published:

5:22 pm, July 16th, 2008 - 51 comments

Categories: national, workers' rights -

Tags: ACC

National has confirmed it intends to privatise the ACC scheme starting with opening the work account to private competition. This would see private insurers cream off large and low-risk employers with special deals, leaving the taxpayer to shoulder the burden of the rest (which would, in turn, be the basis for privatising of the remainder).

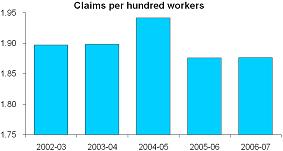

National says privatisation will somehow bring workplace accident rates down, which it claims are rising. Wrong: workplace accident rates are falling. It claims premiums will fall. Wrong: our premiums are already among the cheapest in the world, and we don’t have to pay anyone’s profits.

National says privatisation will somehow bring workplace accident rates down, which it claims are rising. Wrong: workplace accident rates are falling. It claims premiums will fall. Wrong: our premiums are already among the cheapest in the world, and we don’t have to pay anyone’s profits.

Australian insurance companies expect to make $200 million off this privatisation. These profits will be made not by higher premiums but by reduced pay-outs. As you know, that’s how private insurers make profits – by avoiding paying out whenever possible. In practice, that will mean Kiwis missing out on speedy treatment and income coverage, while Aussie insurers get rich.

Part of the genius of ACC is in decoupling blame from compensation. Occupational Safety and Health investigates accidents and holds businesses to health and safety regulations, ACC ensures the injured get treatment and income compensation, and businesses are incentivised to be safe because higher accident rates mean higher levies. Because of this administration of injury compensation leads the world in cheapness and efficiency and there are few court cases. Introducing competing profit-making insurers who are trying to minimise payouts would mean more expensive administration and law suits between individuals, businesses, and insurers tying up the already stretched court system. This was the case before ACC, it’s the case overseas, and it was beginning to happen again when National introduced competition in 1998. The efficiency of ACC is the envy of personal injury law experts around the world* but introducing private insurers will put an end to that.

Only two groups stand to gain from National privatising ACC. Not businesses and workers – insurers and lawyers.

[*I was in a personal injury lecture in Finland, our American professor was introducing the perplexed European students to the common law personal injury litigation system. He concluded that only one common law country had managed find a way to get rid of this resource consuming, lawyer-enriching system. No prizes for guessing which one.]51 comments on “Nats’ ACC plan only good for insurance companies and lawyers ”

- Comments are now closed

Links to post

- Comments are now closed

Recent Comments

- Fact brief – Are we heading into an ‘ice age’?

Skeptical Science is partnering with Gigafact to produce fact briefs — bite-sized fact checks of trending claims. This fact brief was written by Sue Bin Park from the Gigafact team in collaboration with members from our team. You can submit claims you think need checking via the tipline. Are we heading ...4 hours ago

Skeptical Science is partnering with Gigafact to produce fact briefs — bite-sized fact checks of trending claims. This fact brief was written by Sue Bin Park from the Gigafact team in collaboration with members from our team. You can submit claims you think need checking via the tipline. Are we heading ...4 hours ago - As Our Power Lessens: Published

So the Solstice has arrived – Summer in this part of the world, Winter for the Northern Hemisphere. And with it, the publication my new Norse dark-fantasy piece, As Our Power Lessens at Eternal Haunted Summer: https://eternalhauntedsummer.com/issues/winter-solstice-2024/as-our-power-lessens/ As previously noted, this one is very ‘wyrd’, and Northern Theory of Courage. ...9 hours ago

So the Solstice has arrived – Summer in this part of the world, Winter for the Northern Hemisphere. And with it, the publication my new Norse dark-fantasy piece, As Our Power Lessens at Eternal Haunted Summer: https://eternalhauntedsummer.com/issues/winter-solstice-2024/as-our-power-lessens/ As previously noted, this one is very ‘wyrd’, and Northern Theory of Courage. ...9 hours ago - By Any Other Name.

The Natural Choice: As a starter for ten percent of the Party Vote, “saving the planet” is a very respectable objective. Young voters, in particular, raised on the dire (if unheeded) warnings of climate scientists, and the irrefutable evidence of devastating weather events linked to global warming, vote Green. After ...14 hours ago

The Natural Choice: As a starter for ten percent of the Party Vote, “saving the planet” is a very respectable objective. Young voters, in particular, raised on the dire (if unheeded) warnings of climate scientists, and the irrefutable evidence of devastating weather events linked to global warming, vote Green. After ...14 hours ago - Bernard’s last Saturday Soliloquy for 2024

The Government cancelled 60% of Kāinga Ora’s new builds next year, even though the land for them was already bought, the consents were consented and there are builders unemployed all over the place. Photo: Lynn Grieveson / The KākāMōrena. Long stories short, the six things that mattered in Aotearoa’s political ...15 hours ago

The Government cancelled 60% of Kāinga Ora’s new builds next year, even though the land for them was already bought, the consents were consented and there are builders unemployed all over the place. Photo: Lynn Grieveson / The KākāMōrena. Long stories short, the six things that mattered in Aotearoa’s political ...15 hours ago - Bernard’s Picks ‘n’ Mixes for Saturday, December 21

Photo by CHUTTERSNAP on UnsplashEvery morning I get up at 3am to go around the traps of news sites in Aotearoa and globally. I pick out the top ones from my point of view and have been putting them into my Dawn Chorus email, which goes out with a podcast. ...19 hours ago

Photo by CHUTTERSNAP on UnsplashEvery morning I get up at 3am to go around the traps of news sites in Aotearoa and globally. I pick out the top ones from my point of view and have been putting them into my Dawn Chorus email, which goes out with a podcast. ...19 hours ago - 2024 OIA stats

Over on Kikorangi Newsroom's Marc Daalder has published his annual OIA stats. So I thought I'd do mine: 82 OIA requests sent in 2024 7 posts based on those requests 20 average working days to receive a response Ministry of Justice was my most-requested entity, ...1 day ago

Over on Kikorangi Newsroom's Marc Daalder has published his annual OIA stats. So I thought I'd do mine: 82 OIA requests sent in 2024 7 posts based on those requests 20 average working days to receive a response Ministry of Justice was my most-requested entity, ...1 day ago - Climate Change: A perverse incentive

The government published its first Biennial Transparency Report under the Paris Agreement yesterday, and the media has correctly noted that it is missing any plan to actually meet our target. While it hypes domestic emissions reductions so far - which have been good, but will likely get worse thanks to ...1 day ago

- Economic Bulletin December 2024

Welcome to the December 2024 Economic Bulletin. We have two monthly features in this edition. In the first, we discuss what the Half Year Economic and Fiscal Update from Treasury and the Budget Policy Statement from the Minister of Finance tell us about the fiscal position and what to ...2 days ago

Welcome to the December 2024 Economic Bulletin. We have two monthly features in this edition. In the first, we discuss what the Half Year Economic and Fiscal Update from Treasury and the Budget Policy Statement from the Minister of Finance tell us about the fiscal position and what to ...2 days ago - NZCTU make submission in opposition to Treaty Principles Bill

The NZCTU Te Kauae Kaimahi have submitted against the controversial Treaty Principles Bill, slamming the Bill as a breach of Te Tiriti o Waitangi and an attack on tino rangatiratanga and the collective rights of Tangata Whenua. “This Bill seeks to legislate for Te Tiriti o Waitangi principles that are ...2 days ago

- ZB’s Power Couple

I don't knowHow to say what's got to be saidI don't know if it's black or whiteThere's others see it redI don't get the answers rightI'll leave that to youIs this love out of fashionOr is it the time of yearAre these words distraction?To the words you want to hearSongwriters: ...2 days ago

I don't knowHow to say what's got to be saidI don't know if it's black or whiteThere's others see it redI don't get the answers rightI'll leave that to youIs this love out of fashionOr is it the time of yearAre these words distraction?To the words you want to hearSongwriters: ...2 days ago - Austerity thumps GDP most since 1991

Our economy has experienced its worst recession since 1991. Photo: Lynn Grieveson / The KākāMōrena. Long stories short, the six things that matter in Aotearoa’s political economy around housing, climate and poverty on Friday, December 20 in The Kākā’s Dawn Chorus podcast above and the daily Pick ‘n’ Mix below ...2 days ago

- Weekly Roundup 20-December-2024

Twas the Friday before Christmas and all through the week we’ve been collecting stories for our final roundup of the year. As we start to wind down for the year we hope you all have a safe and happy Christmas and new year. If you’re travelling please be safe on ...2 days ago

Twas the Friday before Christmas and all through the week we’ve been collecting stories for our final roundup of the year. As we start to wind down for the year we hope you all have a safe and happy Christmas and new year. If you’re travelling please be safe on ...2 days ago - The Hoon around the year to December 20, 2024

The podcast above of the weekly ‘Hoon’ webinar for paying subscribers on Thursday night features co-hosts & talking about the year’s news with: on climate. Her book of the year was Tim Winton’s cli-fi novel Juice and she also mentioned Mike Joy’s memoir The Fight for Fresh Water. ...2 days ago

- The baby-boomers’ last gasp

The Government can head off to the holidays, entitled to assure itself that it has done more or less what it said it would do. The campaign last year promised to “get New Zealand back on track.” When you look at the basic promises—to trim back Government expenditure, toughen up ...2 days ago

The Government can head off to the holidays, entitled to assure itself that it has done more or less what it said it would do. The campaign last year promised to “get New Zealand back on track.” When you look at the basic promises—to trim back Government expenditure, toughen up ...2 days ago - Skeptical Science New Research for Week #51 2024

Open access notables An intensification of surface Earth’s energy imbalance since the late 20th century, Li et al., Communications Earth & Environment: Tracking the energy balance of the Earth system is a key method for studying the contribution of human activities to climate change. However, accurately estimating the surface energy balance ...2 days ago

- Join us at 5pm for 2024’s last Hoon

Photo by Mauricio Fanfa on UnsplashKia oraCome and join us for our weekly ‘Hoon’ webinar with paying subscribers to The Kākā for an hour at 5 pm today.Jump on this link on YouTube Livestream for our chat about the week’s news with myself , plus regular guests and , ...2 days ago

Photo by Mauricio Fanfa on UnsplashKia oraCome and join us for our weekly ‘Hoon’ webinar with paying subscribers to The Kākā for an hour at 5 pm today.Jump on this link on YouTube Livestream for our chat about the week’s news with myself , plus regular guests and , ...2 days ago - Christmas Gifts: Ageing Boomers, Laurie & Les, Talk Politics.

“Like you said, I’m an unreconstructed socialist. Everybody deserves to get something for Christmas.”“ONE OF THOSE had better be for me!” Hannah grinned, fascinated, as Laurie made his way, gingerly, to the bar, his arms full of gift-wrapped packages.“Of course!”, beamed Laurie. Depositing his armful on the bar-top and selecting ...3 days ago

- GDP Figures No Christmas Present for New Zealand

Data released by Statistics New Zealand today showed a significant slowdown in the economy over the past six months, with GDP falling by 1% in September, and 1.1% in June said CTU Economist Craig Renney. “The data shows that the size of the economy in GDP terms is now smaller ...3 days ago

- Cheeseburgers and Stunt Monkeys

One last thing before I quitI never wanted any moreThan I could fit into my headI still remember every single word you saidAnd all the shit that somehow came along with itStill, there's one thing that comforts meSince I was always caged and now I'm freeSongwriters: David Grohl / Georg ...3 days ago

One last thing before I quitI never wanted any moreThan I could fit into my headI still remember every single word you saidAnd all the shit that somehow came along with itStill, there's one thing that comforts meSince I was always caged and now I'm freeSongwriters: David Grohl / Georg ...3 days ago - MSD rejecting 220 pleas for food grants each day

Sparse offerings outside a Te Kauwhata church. Meanwhile, the Government is cutting spending in ways that make thousands of hungry children even hungrier, while also cutting funding for the charities that help them. It’s also doing that while winding back new building of affordable housing that would allow parents to ...3 days ago

- The Wing Parties’ Economic Policies.

It is difficult to make sense of the Luxon Coalition Government’s economic management.This end-of-year review about the state of economic management – the state of the economy was last week – is not going to cover the National Party contribution. Frankly, like every other careful observer, I cannot make up ...3 days ago

It is difficult to make sense of the Luxon Coalition Government’s economic management.This end-of-year review about the state of economic management – the state of the economy was last week – is not going to cover the National Party contribution. Frankly, like every other careful observer, I cannot make up ...3 days ago - Back on Track

This morning I awoke to the lovely news that we are firmly back on track, that is if the scale was reversed.NZ ranks low in global economic comparisonsNew Zealand's economy has been ranked 33rd out of 37 in an international comparison of which have done best in 2024.Economies were ranked ...3 days ago

This morning I awoke to the lovely news that we are firmly back on track, that is if the scale was reversed.NZ ranks low in global economic comparisonsNew Zealand's economy has been ranked 33rd out of 37 in an international comparison of which have done best in 2024.Economies were ranked ...3 days ago - Book Review: How Big Things Get Done

This is a guest post by George Weeks, reviewing a book called How Big Things Get Done by Bent Flyvbjerg and Dan Gardner Want to know how to do something big? Ask someone who has done it before! Professor Bent Flyvbjerg has spent his career studying megaprojects. In 2023, ...3 days ago

- Gordon Campbell On Why We Can’t Survive Two More Years Of This

Remember those silent movies where the heroine is tied to the railway tracks or going over the waterfall in a barrel? Finance Minister Nicola Willis seems intent on portraying herself as that damsel in distress. According to Willis, this country’s current economic problems have all been caused by the spending ...3 days ago

Remember those silent movies where the heroine is tied to the railway tracks or going over the waterfall in a barrel? Finance Minister Nicola Willis seems intent on portraying herself as that damsel in distress. According to Willis, this country’s current economic problems have all been caused by the spending ...3 days ago - Dragging our way towards the finish line, the end of this year can’t come soon enough for many…

Similar to the cuts and the austerity drive imposed by Ruth Richardson in the 1990’s, an era which to all intents and purposes we’ve largely fiddled around the edges with fixing in the time since – over, to be fair, several administrations – whilst trying our best it seems to ...3 days ago

Similar to the cuts and the austerity drive imposed by Ruth Richardson in the 1990’s, an era which to all intents and purposes we’ve largely fiddled around the edges with fixing in the time since – over, to be fair, several administrations – whilst trying our best it seems to ...3 days ago - Handling Democracy.

String-Pulling in the Dark: For the democratic process to be meaningful it must also be public. WITH TRUST AND CONFIDENCE in New Zealand’s politicians and journalists steadily declining, restoring those virtues poses a daunting challenge. Just how daunting is made clear by comparing the way politicians and journalists treated New Zealanders ...3 days ago

- Open letter to the Minister of Dwindling Finances

Dear Nicola Willis, thank you for letting us know in so many words that the swingeing austerity hasn't worked.By in so many words I mean the bit where you said, Here is a sea of red ink in which we are drowning after twelve months of savage cost cutting and ...3 days ago

Dear Nicola Willis, thank you for letting us know in so many words that the swingeing austerity hasn't worked.By in so many words I mean the bit where you said, Here is a sea of red ink in which we are drowning after twelve months of savage cost cutting and ...3 days ago - Open Government: The joke ends

The Open Government Partnership is a multilateral organisation committed to advancing open government. Countries which join are supposed to co-create regular action plans with civil society, committing to making verifiable improvements in transparency, accountability, participation, or technology and innovation for the above. And they're held to account through an Independent ...3 days ago

- An unusual sort of press conference

Today I tuned into something strange: a press conference that didn’t make my stomach churn or the hairs on the back of my neck stand on end. Which was strange, because it was about the torture of children. It was the announcement by Erica Stanford — on her own, unusually ...3 days ago

Today I tuned into something strange: a press conference that didn’t make my stomach churn or the hairs on the back of my neck stand on end. Which was strange, because it was about the torture of children. It was the announcement by Erica Stanford — on her own, unusually ...3 days ago - This substack has talked about this government’s seeming corruption & pro-corporate issues...

This is a must watch, and puts on brilliant and practical display the implications and mechanics of fast-track law corruption and weakness.CLICK HERE: LINK TO WATCH VIDEOOur news media as it is set up is simply not equipped to deal with the brazen disinformation and corruption under this right wing ...3 days ago

This is a must watch, and puts on brilliant and practical display the implications and mechanics of fast-track law corruption and weakness.CLICK HERE: LINK TO WATCH VIDEOOur news media as it is set up is simply not equipped to deal with the brazen disinformation and corruption under this right wing ...3 days ago - NZCTU: Minister needs to listen to the evidence on engineered stone ban

NZCTU Te Kauae Kaimahi Acting Secretary Erin Polaczuk is welcoming the announcement from Minister of Workplace Relations and Safety Brooke van Velden that she is opening consultation on engineered stone and is calling on her to listen to the evidence and implement a total ban of the product. “We need ...3 days ago

- Wednesday 18 December

The Government has announced a 1.5% increase in the minimum wage from 1 April 2025, well below forecast inflation of 2.5%. Unions have reacted strongly and denounced it as a real terms cut. PSA and the CTU are opposing a new round of staff cuts at WorkSafe, which they say ...4 days ago

- Can the government change its mind on the ferries?

The decision to unilaterally repudiate the contract for new Cook Strait ferries is beginning to look like one of the stupidest decisions a New Zealand government ever made. While cancelling the ferries and their associated port infrastructure may have made this year's books look good, it means higher costs later, ...4 days ago

- Notes from Afar: Will Luxon Attend Waitangi Day? And Opposition Calls Out Nicola Willis for “C...

Hi there! I’ve been overseas recently, looking after a situation with a family member. So apologies if there any less than focused posts! Vanuatu has just had a significant 7.3 earthquake. Two MFAT staff are unaccounted for with local fatalities.It’s always sad to hear of such things happening.I think of ...4 days ago

Hi there! I’ve been overseas recently, looking after a situation with a family member. So apologies if there any less than focused posts! Vanuatu has just had a significant 7.3 earthquake. Two MFAT staff are unaccounted for with local fatalities.It’s always sad to hear of such things happening.I think of ...4 days ago - Member’s morning

Today is a special member's morning, scheduled to make up for the government's theft of member's days throughout the year. First up was the first reading of Greg Fleming's Crimes (Increased Penalties for Slavery Offences) Amendment Bill, which was passed unanimously. Currently the House is debating the third reading of ...4 days ago

- Going Backwards

We're going backwardsIgnoring the realitiesGoing backwardsAre you counting all the casualties?We are not there yetWhere we need to beWe are still in debtTo our insanitiesSongwriter: Martin Gore Read more ...4 days ago

We're going backwardsIgnoring the realitiesGoing backwardsAre you counting all the casualties?We are not there yetWhere we need to beWe are still in debtTo our insanitiesSongwriter: Martin Gore Read more ...4 days ago - Blaming Treasury & Labour, Willis looks for even more Austerity

Willis blamed Treasury for changing its productivity assumptions and Labour’s spending increases since Covid for the worsening Budget outlook. Photo: Getty ImagesMōrena. Long stories short, the six things that matter in Aotearoa’s political economy around housing, climate and poverty on Wednesday, December 18 in The Kākā’s Dawn Chorus podcast above ...4 days ago

- December-24 AT Board Meeting

Today the Auckland Transport board meet for the last time this year. For those interested (and with time to spare), you can follow along via this MS Teams link from 10am. I’ve taken a quick look through the agenda items to see what I think the most interesting aspects are. ...4 days ago

- The Making of a Mental Health Rockstar

Hi,If you’re a New Zealander — you know who Mike King is. He is the face of New Zealand’s battle against mental health problems. He can be loud and brash. He raises, and is entrusted with, a lot of cash. Last year his “I Am Hope” charity reported a revenue ...4 days ago

Hi,If you’re a New Zealander — you know who Mike King is. He is the face of New Zealand’s battle against mental health problems. He can be loud and brash. He raises, and is entrusted with, a lot of cash. Last year his “I Am Hope” charity reported a revenue ...4 days ago - It could have been worse

Probably about the only consolation available from yesterday’s unveiling of the Half-Yearly Economic and Fiscal Update (HYEFU) is that it could have been worse. Though Finance Minister Nicola Willis has tightened the screws on future government spending, she has resisted the calls from hard-line academics, fiscal purists and fiscal hawks ...4 days ago

- The Deep Divisions of Local Government

The right have a stupid saying that is only occasionally true:When is democracy not democracy? When it hasn’t been voted on.While not true in regards to branches of government such as the judiciary, it’s a philosophy that probably should apply to recently-elected local government councillors. Nevertheless, this concept seemed to ...4 days ago

The right have a stupid saying that is only occasionally true:When is democracy not democracy? When it hasn’t been voted on.While not true in regards to branches of government such as the judiciary, it’s a philosophy that probably should apply to recently-elected local government councillors. Nevertheless, this concept seemed to ...4 days ago - Willis’ austerity strategy just isn’t working

Long story short: the Government’s austerity policy has driven the economy into a deeper and longer recession that means it will have to borrow $20 billion more over the next four years than it expected just six months ago. Treasury’s latest forecasts show the National-ACT-NZ First Government’s fiscal strategy of ...4 days ago

- Sabin 33 #7 – Are solar projects hurting farmers and rural communities?

On November 1, 2024 we announced the publication of 33 rebuttals based on the report "Rebutting 33 False Claims About Solar, Wind, and Electric Vehicles" written by Matthew Eisenson, Jacob Elkin, Andy Fitch, Matthew Ard, Kaya Sittinger & Samuel Lavine and published by the Sabin Center for Climate Change Law at Columbia ...4 days ago

- Join us for a pop-up Hoon at 5pm on HYEFU

4 days ago

4 days ago - ‘Ideas Worth Saving’: A Call for Papers

Some years ago, I found myself pondering the power of literature to endure. Or at least the power of some of it to endure, while the rest vanishes in mere decades: https://phuulishfellow.wordpress.com/2019/08/07/look-on-my-works-ye-mighty-and-despair-the-literary-future/. I have similarly had fun with the subject in some of my short stories, such as Another Alexandria ...4 days ago

Some years ago, I found myself pondering the power of literature to endure. Or at least the power of some of it to endure, while the rest vanishes in mere decades: https://phuulishfellow.wordpress.com/2019/08/07/look-on-my-works-ye-mighty-and-despair-the-literary-future/. I have similarly had fun with the subject in some of my short stories, such as Another Alexandria ...4 days ago - Corrections is torturing prisoners again

In 1998, in the wake of the Paremoremo Prison riot, the Department of Corrections established the "Behaviour Management Regime". Prisoners were locked in their cells for 22 or 23 hours a day, with no fresh air, no exercise, no social contact, no entertainment, and in some cases no clothes and ...4 days ago

- HYEFU and BPS data shows New Zealand is way off track

New data released by the Treasury shows that the economic policies of this Government have made things worse in the year since they took office, said NZCTU Economist Craig Renney. “Our fiscal indicators are all heading in the wrong direction – with higher levels of debt, a higher deficit, and ...4 days ago

- “Better economic management”

At the 2023 election, National basically ran on a platform of being better economic managers. So how'd that turn out for us? In just one year, they've fucked us for two full political terms: The government's books are set to remain deeply in the red for the near term ...4 days ago

- Shameless, clueless

AUSTERITYText within this block will maintain its original spacing when publishedMy spreadsheet insists This pain leads straight to glory (File not found) Read more ...5 days ago

AUSTERITYText within this block will maintain its original spacing when publishedMy spreadsheet insists This pain leads straight to glory (File not found) Read more ...5 days ago - Minimum wage ‘increase’ is an effective cut

The NZCTU Te Kauae Kaimahi are saying that the Government should do the right thing and deliver minimum wage increases that don’t see workers fall further behind, in response to today’s announcement that the minimum wage will only be increased by 1.5%, well short of forecast inflation. “With inflation forecast ...5 days ago

- Crazy ’bout a Sharp-dressed Man

Oh, I weptFor daysFilled my eyesWith silly tearsOh, yeaBut I don'tCare no moreI don't care ifMy eyes get soreSongwriters: Paul Rodgers / Paul Kossoff. Read more ...5 days ago

Oh, I weptFor daysFilled my eyesWith silly tearsOh, yeaBut I don'tCare no moreI don't care ifMy eyes get soreSongwriters: Paul Rodgers / Paul Kossoff. Read more ...5 days ago - How much should you worry about a collapse of the Atlantic conveyor belt?

This is a re-post from Yale Climate Connections by Bob Henson In this aerial view, fingers of meltwater flow from the melting Isunnguata Sermia glacier descending from the Greenland Ice Sheet on July 11, 2024, near Kangerlussuaq, Greenland. According to the Programme for Monitoring of the Greenland Ice Sheet (PROMICE), the ...5 days ago

- 8% ACT Party Creates One Ring To Rule Them All

In August, I wrote an article about David Seymour1 with a video of his testimony, to warn that there were grave dangers to his Ministry of Regulation:David Seymour's Ministry of Slush Hides Far Greater RisksWhy Seymour's exorbitant waste of taxpayers' money could be the least of concernThe money for Seymour ...5 days ago

In August, I wrote an article about David Seymour1 with a video of his testimony, to warn that there were grave dangers to his Ministry of Regulation:David Seymour's Ministry of Slush Hides Far Greater RisksWhy Seymour's exorbitant waste of taxpayers' money could be the least of concernThe money for Seymour ...5 days ago - When austerity worsens public debt & cuts GDP

Willis is expected to have to reveal the bitter fiscal fruits of her austerity strategy in the HYEFU later today. Photo: Lynn Grieveson/TheKakaMōrena. Long stories short, the six things that matter in Aotearoa’s political economy around housing, climate and poverty on Tuesday, December 17 in The Kākā’s Dawn Chorus podcast ...5 days ago

- Govt to double number of toll roads

On Friday the government announced it would double the number of toll roads in New Zealand as well as make a few other changes to how toll roads are used in the country. The real issue though is not that tolling is being used but the suggestion it will make ...5 days ago

- Luxon’s pre-emptive strike

The Prime Minister yesterday engaged in what looked like a pre-emptive strike designed to counter what is likely to be a series of depressing economic statistics expected before the end of the week. He opened his weekly post-Cabinet press conference with a recitation of the Government’s achievements. “It certainly has ...5 days ago

- Gordon Campbell On The Coalition’s Empty Gestures, And Abortion Refusal As The New Slavery

This whooping cough story from south Auckland is a good example of the coalition government’s approach to social need – spend money on urging people to get vaccinated but only after you’ve cut the funding to where they could get vaccinated. This has been the case all year with public ...5 days ago

- More public service contempt of parliament

Back in 2023 the New Zealand Council for Civil Liberties raised concerns about the inherent conflict of interest involved in public service agencies supporting parliamentary select committees. Our parliament is run on a shoestring, so depends on the public service for advice. But public service agencies work for Ministers, not ...5 days ago

- If There Is A God

And if there is a GodI know he likes to rockHe likes his loud guitarsHis spiders from MarsAnd if there is a GodI know he's watching meHe likes what he seesBut there's trouble on the breezeSongwriter: William Patrick Corgan Read more ...6 days ago

And if there is a GodI know he likes to rockHe likes his loud guitarsHis spiders from MarsAnd if there is a GodI know he's watching meHe likes what he seesBut there's trouble on the breezeSongwriter: William Patrick Corgan Read more ...6 days ago - A Lipstick Government

Here’s a quick round up of today’s political news:1. MORE FOOD BANKS, CHARITIES, DOMESTIC VIOLENCE SHELTERS AND YOUTH SOCIAL SERVICES SET TO CLOSE OR SCALE BACK AROUND THE COUNTRY AS GOVT CUTS FUNDINGSome of Auckland's largest foodbanks are warning they may need to close or significantly reduce food parcels after ...6 days ago

Here’s a quick round up of today’s political news:1. MORE FOOD BANKS, CHARITIES, DOMESTIC VIOLENCE SHELTERS AND YOUTH SOCIAL SERVICES SET TO CLOSE OR SCALE BACK AROUND THE COUNTRY AS GOVT CUTS FUNDINGSome of Auckland's largest foodbanks are warning they may need to close or significantly reduce food parcels after ...6 days ago - NZCTU open letter to Treasury on undue restrictions on restricted briefings

Iain Rennie, CNZMSecretary and Chief Executive to the TreasuryDear Secretary, Undue restrictions on restricted briefings This week, the Treasury barred representatives from four organisations, including the New Zealand Council of Trade Unions Te Kauae Kaimahi, from attending the restricted briefing for the Half-Year Economic and Fiscal Update. We had been ...6 days ago

- Why you won’t hear me advocate for electric cars

This is a guest post by Tim Adriaansen, a community, climate, and accessibility advocate. I won’t shut up about climate breakdown, and whenever possible I try to shift the focus of a climate conversation towards solutions. But you’ll almost never hear me give more than a passing nod to ...6 days ago

- Coalition forced to back down on tolling Pahiatua track

A grassroots backlash has forced a backdown from Brown, but he is still eyeing up plenty of tolls for other new roads. And the pressure is on Willis to ramp up the Government’s austerity strategy. Photo: Getty ImagesMōrena. Long stories short, the six things that matter in Aotearoa’s political economy ...6 days ago

- Thank You

Hi all,I'm pretty overwhelmed by all your messages and emails today; thank you so very much.As much as my newsletter this morning was about money, and we all need to earn money, it was mostly about world domination if I'm honest. 😉I really hate what’s happening to our country, and ...6 days ago

Hi all,I'm pretty overwhelmed by all your messages and emails today; thank you so very much.As much as my newsletter this morning was about money, and we all need to earn money, it was mostly about world domination if I'm honest. 😉I really hate what’s happening to our country, and ...6 days ago - 2024 SkS Weekly Climate Change & Global Warming News Roundup #50

A listing of 23 news and opinion articles we found interesting and shared on social media during the past week: Sun, December 8, 2024 thru Sat, December 14, 2024. Listing by Category Like last week's summary this one contains the list of articles twice: based on categories and based on ...6 days ago

- Making Gravy

I started writing this morning about Hobson’s Pledge, examining the claims they and their supporters make, basically ripping into them. But I kept getting notifications coming through, and not good ones.Each time I looked up, there was another un-subscription message, and I felt a bit sicker at the thought of ...7 days ago

I started writing this morning about Hobson’s Pledge, examining the claims they and their supporters make, basically ripping into them. But I kept getting notifications coming through, and not good ones.Each time I looked up, there was another un-subscription message, and I felt a bit sicker at the thought of ...7 days ago - Nothing here but the shadows

Once, long before there was Harry and Meghan and Dodi and all those episodes of The Crown, they came to spend some time with us, Charles and Diana. Was there anyone in the world more glamorous than the Princess of Wales?Dazzled as everyone was by their company, the leader of ...7 days ago

Once, long before there was Harry and Meghan and Dodi and all those episodes of The Crown, they came to spend some time with us, Charles and Diana. Was there anyone in the world more glamorous than the Princess of Wales?Dazzled as everyone was by their company, the leader of ...7 days ago - The United Right: the FSU’s Continued Efforts to Undermine Academia

The collective right have a problem.The entire foundation for their world view is antiscientific. Their preferred economic strategies have been disproven. Their whole neoliberal model faces accusations of corporate corruption and worsening inequality. Climate change not only definitely exists, its rapid progression demands an immediate and expensive response in order ...1 week ago

- Showing the Americans how to do it

Just ten days ago, South Korea's president attempted a self-coup, declaring martial law and attempting to have opposition MPs murdered or arrested in an effort to seize unconstrained power. The attempt was rapidly defeated by the national assembly voting it down and the people flooding the streets to defend democracy. ...1 week ago

- 2 Men, 1 Haircut

Hi,“What I love about New Zealanders is that sometimes you use these expressions that as Americans we have no idea what those things mean!"I am watching a 30-something year old American ramble on about how different New Zealanders are to Americans. It’s his podcast, and this man is doing a ...1 week ago

Hi,“What I love about New Zealanders is that sometimes you use these expressions that as Americans we have no idea what those things mean!"I am watching a 30-something year old American ramble on about how different New Zealanders are to Americans. It’s his podcast, and this man is doing a ...1 week ago - Chris Penk’s Hate Parade

What Chris Penk has granted holocaust-denier and equal-opportunity-bigot Candace Owens is not “freedom of speech”. It’s not even really freedom of movement, though that technically is the right she has been granted. What he has given her is permission to perform. Freedom of SpeechIn New Zealand, the right to freedom ...1 week ago

What Chris Penk has granted holocaust-denier and equal-opportunity-bigot Candace Owens is not “freedom of speech”. It’s not even really freedom of movement, though that technically is the right she has been granted. What he has given her is permission to perform. Freedom of SpeechIn New Zealand, the right to freedom ...1 week ago - Tell me a story

All those tears on your cheeksJust like deja vu flow nowWhen grandmother speaksSo tell me a story (I'll tell you a story)Spell it out, I can't hear (What do you want to hear?)Why you wear black in the morning?Why there's smoke in the air? Songwriter: Greg Johnson.Mōrena all ☀️Something a ...1 week ago

All those tears on your cheeksJust like deja vu flow nowWhen grandmother speaksSo tell me a story (I'll tell you a story)Spell it out, I can't hear (What do you want to hear?)Why you wear black in the morning?Why there's smoke in the air? Songwriter: Greg Johnson.Mōrena all ☀️Something a ...1 week ago - As Our Power Lessens: Accepted

2024 is now officially my best-ever year for short stories. My 1,850-word dark fantasy piece, As Our Power Lessens, has been accepted for the upcoming solstice edition of Eternal Haunted Summer (https://eternalhauntedsummer.com/), thereby making that six published short stories for the calendar year. As always, see the Bibliography page for ...1 week ago

- Six years of work wasted – Holidays Act reform now years away

Brooke van Velden has wasted six years of work from businesses, unions, and government by binning planned Holidays Act reforms, said Acting CTU President Rachel Mackintosh in response to today’s announcement from Minister for Workplace Relations and Safety. “The Minister has cynically kicked the can on Holiday Act reform even ...1 week ago

- Come Undone?

Words, playing me deja vuLike a radio tune, I swear I've heard beforeChill, is it something real?Or the magic I'm feeding off your fingersWho do you need?Who do you love?When you come undoneSongwriters: John Taylor / Simon Le Bon / Nick Rhodes / Warren Cuccurullo.When this three-way coalition was being ...1 week ago

Words, playing me deja vuLike a radio tune, I swear I've heard beforeChill, is it something real?Or the magic I'm feeding off your fingersWho do you need?Who do you love?When you come undoneSongwriters: John Taylor / Simon Le Bon / Nick Rhodes / Warren Cuccurullo.When this three-way coalition was being ...1 week ago

{kind=link}

{kind=link}

{kind=link}

- National’s Greatest Misses 2023-4

National has only been in power for a year, but everywhere you look, its choices are taking New Zealand a long way backwards. In no particular order, here are the National Government's Top 50 Greatest Misses of its first year in power. ...1 day ago

National has only been in power for a year, but everywhere you look, its choices are taking New Zealand a long way backwards. In no particular order, here are the National Government's Top 50 Greatest Misses of its first year in power. ...1 day ago - Release: Minister’s plan for tertiary sector a backwards step

Returning to the model that was failing for most polytechnics and Institutes of Technology is not the answer. ...2 days ago

- Release: National buries 1019 planned homes

It’s been revealed that National has cancelled 60 percent of its housing projects planned before mid-2025 amidst housing woes. ...2 days ago

- Release: Rule-Czar bill a right-wing power grab

The Government is quietly undertaking consultation on the dangerous Regulatory Standards Bill over the Christmas period to avoid too much attention. ...2 days ago

- Release: Why not both? Luxon shuns Waitangi celebrations

Prime Minister Christopher Luxon is running away from problems of his own creation, with his decision not to go to Waitangi. ...2 days ago

- Govt’s ‘free speech’ legislation stokes fear, not freedom

The Government’s planned changes to the freedom of speech obligations of universities is little more than a front for stoking the political fires of disinformation and fear, placing teachers and students in the crosshairs. ...2 days ago

The Government’s planned changes to the freedom of speech obligations of universities is little more than a front for stoking the political fires of disinformation and fear, placing teachers and students in the crosshairs. ...2 days ago - Release: Nicola Willis spirals country deeper into recession

The economy shrank 1% this quarter and New Zealand has tumbled into the depths of a recession of Nicola Willis’ making. ...3 days ago

- Release: Hikes for company directors but not ordinary Kiwis

Working people are going backwards while company directors are being given huge pay hikes. ...3 days ago

- ECE no place to cut corners

The Ministry of Regulation’s report into Early Childhood Education (ECE) in Aotearoa raises serious concerns about the possibility of lowering qualification requirements, undermining quality and risking worse outcomes for tamariki, whānau, and kaiako. ...4 days ago

- Release: Strengthening Justice Services for New Zealanders

A Bill to modernise the role of Justices of the Peace (JP), ensuring they remain active in their communities and connected with other JPs, has been put into the ballot. ...4 days ago

- Release: Labour will continue fight against destructive projects

Labour will continue to fight unsustainable and destructive projects that are able to leap-frog environment protection under National’s Fast-track Approvals Bill. ...4 days ago

- Green Government will revoke dodgy fast-track projects

The Green Party has warned that a Green Government will revoke the consents of companies who override environmental protections as part of Fast-Track legislation being passed today. ...4 days ago

- Government for the wealthy keeps pushing austerity

The Green Party says the Half Year Economic and Fiscal Update shows how the Government is failing to address the massive social and infrastructure deficits our country faces. ...4 days ago

- Release: Visa changes let migrant workers be paid less

The Government’s latest move to reduce the earnings of migrant workers will not only hurt migrants but it will drive down the wages of Kiwi workers. ...4 days ago

- Release: Nightmare before Christmas for Nicola Willis

With more debt and a larger deficit, Nicola Willis’ reputation is in tatters after her failure to return the Government’s books to surplus. ...4 days ago

- Warning to Fast-Track Applicants – ‘Exploit the Whenua, Face the Consequences’

Te Pāti Māori has this morning issued a stern warning to Fast-Track applicants with interests in mining, pledging to hold them accountable through retrospective liability and to immediately revoke Fast-Track consents under a future Te Pāti Māori government. This warning comes ahead of today’s third reading of the Fast-Track Approvals ...4 days ago

- Release: Govt cuts wages for lowest paid NZers… again

For the second year running, the government has effectively cut wages for the lowest paid workers in New Zealand. ...5 days ago

- Govt’s miserly 1.5% minimum wage will take workers backwards

The Government’s announcement today of a 1.5 per cent increase to minimum wage is another blow for workers, with inflation projected to exceed the increase, meaning it’s a real terms pay reduction for many. ...5 days ago

- Release: Govt shirking responsibility for rate hikes

All the Government has achieved from its announcement today is to continue to push responsibility back on councils for its own lack of action to help bring down skyrocketing rates. ...5 days ago

- Luxon’s ‘localism’ strikes again

The Government has used its final post-Cabinet press conference of the year to punch down on local government without offering any credible solutions to the issues our councils are facing. ...5 days ago

- Release: Govt breaks promise on EV chargers

The Government has failed to keep its promise to ‘super charge’ the EV network, delivering just 292 chargers - less than half of the 670 chargers needed to meet its target. ...5 days ago

- Greens call for end to subsidies for Methanex

The Green Party is calling for the Government to stop subsidising the largest user of the country’s gas supplies, Methanex, following a report highlighting the multi-national’s disproportionate influence on energy prices in Aotearoa. ...6 days ago

- Govt child poverty targets allow for increase in poverty

The Green Party is appalled with the Government’s new child poverty targets that are based on a new ‘persistent poverty’ measure that could be met even with an increase in child poverty. ...1 week ago

- Release: Four weeks annual leave under threat

The Government’s attack on workers continues with news it is scrapping work on the Holidays Act. ...1 week ago

- Govt’s emissions plan for measly 1% reduction

New independent analysis has revealed that the Government’s Emissions Reduction Plan (ERP) will reduce emissions by a measly 1 per cent by 2030, failing to set us up for the future and meeting upcoming targets. ...1 week ago

- Greens stand in solidarity with Whakaata Māori on sad day

The loss of 27 kaimahi at Whakaata Māori and the end of its daily news bulletin is a sad day for Māori media and another step backwards for Te Tiriti o Waitangi justice. ...1 week ago

- Sanctions regime to create more hardship for families

Yesterday the Government passed cruel legislation through first reading to establish a new beneficiary sanction regime that will ultimately mean more households cannot afford the basic essentials. ...1 week ago

- Govt gifts renters housing anxiety for Christmas

Today's passing of the Government's Residential Tenancies Amendment Bill–which allows landlords to end tenancies with no reason–ignores the voice of the people and leaves renters in limbo ahead of the festive season. ...1 week ago

- Release: National Party urged to support modern slavery legislation

Labour is urging the Prime Minister to walk the talk and support legislation combating modern slavery. ...1 week ago

- Release: Labour has lost confidence in the Speaker

The Speaker of the New Zealand Parliament made an unprecedented decision on the government amendment to the Fast Track Approvals Bill last night. ...1 week ago

- One year on, still no progress on new ferries

Today’s announcement from the Government on its plan for new ferries throws more uncertainty on the future of the country’s rail network. ...2 weeks ago

- Release: Nicola Willis’ smaller ferries will cost more

After wasting a year, Nicola Willis has delivered a worse deal for the Cook Strait ferries that will end up being more expensive and take longer to arrive. ...2 weeks ago

- Bill to sanction unlawful occupation of Palestine

Green Party co-leader Chlöe Swarbrick has today launched a Member’s Bill to sanction Israel for its unlawful presence in the Occupied Palestinian Territory, as the All Out For Gaza rally reaches Parliament. ...2 weeks ago

- Release: Labour fully supports greyhound racing ban

The Government has done the right thing in moving to ban greyhound racing. ...2 weeks ago

- Greyhound racing industry ban marks new era for animal welfare

After years of advocacy, the Green Party is very happy to hear the Government has listened to our collective voices and announced the closure of the greyhound racing industry, by 1 August 2026. ...2 weeks ago

- Rangatahi voices must be centred in Government’s Relationship and Sexuality Education refresh

In response to a new report from ERO, the Government has acknowledged the urgent need for consistency across the curriculum for Relationship and Sexuality Education (RSE) in schools. ...2 weeks ago

- Govt introduces archaic anti-worker legislation

The Green Party is appalled at the Government introducing legislation that will make it easier to penalise workers fighting for better pay and conditions. ...2 weeks ago

- Winston Peters – Kinleith Mill Speech

Thank you for the invitation to speak with you tonight on behalf of the political party I belong to - which is New Zealand First. As we have heard before this evening the Kinleith Mill is proposing to reduce operations by focusing on pulp and discontinuing “lossmaking paper production”. They say that they are currently consulting on the plan to permanently shut ...2 weeks ago

Thank you for the invitation to speak with you tonight on behalf of the political party I belong to - which is New Zealand First. As we have heard before this evening the Kinleith Mill is proposing to reduce operations by focusing on pulp and discontinuing “lossmaking paper production”. They say that they are currently consulting on the plan to permanently shut ...2 weeks ago - Swarbrick calls on Auckland Mayor to end delay of revival of St James Theatre

Auckland Central MP, Chlöe Swarbrick, has written to Mayor Wayne Brown requesting he stop the unnecessary delays on St James Theatre’s restoration. ...2 weeks ago

- He Ara Anamata: Greens launch Emissions Reduction Plan

Today, the Green Party of Aotearoa proudly unveils its new Emissions Reduction Plan–He Ara Anamata–a blueprint reimagining our collective future. ...2 weeks ago

- PM appoints business leader to APEC Business Advisory Council

Prime Minister Christopher Luxon has appointed Sarah Ottrey to the APEC Business Advisory Council (ABAC). “At my first APEC Summit in Lima, I experienced firsthand the role that ABAC plays in guaranteeing political leaders hear the voice of business,” Mr Luxon says. “New Zealand’s ABAC representatives are very well respected and ...2 days ago

Prime Minister Christopher Luxon has appointed Sarah Ottrey to the APEC Business Advisory Council (ABAC). “At my first APEC Summit in Lima, I experienced firsthand the role that ABAC plays in guaranteeing political leaders hear the voice of business,” Mr Luxon says. “New Zealand’s ABAC representatives are very well respected and ...2 days ago - New intelligence oversight appointments

Prime Minister Christopher Luxon has announced four appointments to New Zealand’s intelligence oversight functions. The Honourable Robert Dobson KC has been appointed Chief Commissioner of Intelligence Warrants, and the Honourable Brendan Brown KC has been appointed as a Commissioner of Intelligence Warrants. The appointments of Hon Robert Dobson and Hon ...2 days ago

- New housing developments able to progress more quickly

Improvements in the average time it takes to process survey and title applications means housing developments can progress more quickly, Minister for Land Information Chris Penk says. “The government is resolutely focused on improving the building and construction pipeline,” Mr Penk says. “Applications to issue titles and subdivide land are ...2 days ago

- Actions to speed up air travel delivering results

The Government’s measures to reduce airport wait times, and better transparency around flight disruptions is delivering encouraging early results for passengers ahead of the busy summer period, Transport Minister Simeon Brown says. “Improving the efficiency of air travel is a priority for the Government to give passengers a smoother, more reliable ...2 days ago

- Ending contracted emergency housing in Rotorua

The Government today announced the intended closure of the Apollo Hotel as Contracted Emergency Housing (CEH) in Rotorua, Associate Housing Minister Tama Potaka says. This follows a 30 per cent reduction in the number of households in CEH in Rotorua since National came into Government. “Our focus is on ending CEH in the Whakarewarewa area starting ...2 days ago

- Vocational education and training decisions support return to regions

The Government will reshape vocational education and training to return decision making to regions and enable greater industry input into work-based learning Tertiary Education and Skills Minister, Penny Simmonds says. “The redesigned system will better meet the needs of learners, industry, and the economy. It includes re-establishing regional polytechnics that ...2 days ago

- Reducing the environmental impact of synthetic refrigerants

The Government is taking action to better manage synthetic refrigerants and reduce emissions caused by greenhouse gases found in heating and cooling products, Environment Minister Penny Simmonds says. “Regulations will be drafted to support a product stewardship scheme for synthetic refrigerants, Ms. Simmonds says. “Synthetic refrigerants are found in a ...2 days ago

- Ngāruawāhia section of Waikato Expressway back to 4 lanes for Christmas

People travelling on State Highway 1 north of Hamilton will be relieved that remedial works and safety improvements on the Ngāruawāhia section of the Waikato Expressway were finished today, with all lanes now open to traffic, Transport Minister Simeon Brown says.“I would like to acknowledge the patience of road users ...2 days ago

- Appointments to the ENZ board

Tertiary Education and Skills Minister, Penny Simmonds, has announced a new appointment to the board of Education New Zealand (ENZ). Dr Erik Lithander has been appointed as a new member of the ENZ board for a three-year term until 30 January 2028. “I would like to welcome Dr Erik Lithander to the ...2 days ago

- Government to celebrate Waitangi Day around NZ

The Government will have senior representatives at Waitangi Day events around the country, including at the Waitangi Treaty Grounds, but next year Prime Minister Christopher Luxon has chosen to take part in celebrations elsewhere. “It has always been my intention to celebrate Waitangi Day around the country with different ...2 days ago

- More gangs added to Gangs Act list

Two more criminal gangs will be subject to the raft of laws passed by the Coalition Government that give Police more powers to disrupt gang activity, and the intimidation they impose in our communities, Police Minister Mark Mitchell says. Following an Order passed by Cabinet, from 3 February 2025 the ...3 days ago

- Judicial appointment announced

Attorney-General Judith Collins today announced the appointment of Justice Christian Whata as a Judge of the Court of Appeal. Justice Whata’s appointment as a Judge of the Court of Appeal will take effect on 1 August 2025 and fill a vacancy created by the retirement of Hon Justice David Goddard on ...3 days ago

- GDP data highlights importance of growth

The latest economic figures highlight the importance of the steps the Government has taken to restore respect for taxpayers’ money and drive economic growth, Finance Minister Nicola Willis says. Data released today by Stats NZ shows Gross Domestic Product fell 1 per cent in the September quarter. “Treasury and most ...3 days ago

- Strengthening Free Speech in Universities

Tertiary Education and Skills Minister Penny Simmonds and Associate Minister of Education David Seymour today announced legislation changes to strengthen freedom of speech obligations on universities. “Freedom of speech is fundamental to the concept of academic freedom and there is concern that universities seem to be taking a more risk-averse ...3 days ago

- Launch of Emergency Cellular Priority Service

Police Minister, Mark Mitchell, and Internal Affairs Minister, Brooke van Velden, today launched a further Public Safety Network cellular service that alongside last year’s Cellular Roaming roll-out, puts globally-leading cellular communications capability into the hands of our emergency responders. The Public Safety Network’s new Cellular Priority service means Police, Wellington ...3 days ago

- Minister reopens Mangamuka Gorge

State Highway 1 through the Mangamuka Gorge has officially reopened today, providing a critical link for Northlanders and offering much-needed relief ahead of the busy summer period, Transport Minister Simeon Brown says.“The Mangamuka Gorge is a vital route for Northland, carrying around 1,300 vehicles per day and connecting the Far ...3 days ago

- Funding confirmed for second Ashburton Bridge

The Government has welcomed decisions by the NZ Transport Agency (NZTA) and Ashburton District Council confirming funding to boost resilience in the Canterbury region, with construction on a second Ashburton Bridge expected to begin in 2026, Transport Minister Simeon Brown says. “Delivering a second Ashburton Bridge to improve resilience and ...3 days ago

- Government boosts support for avian influenza response

The Government is backing the response into high pathogenic avian influenza (HPAI) in Otago, Biosecurity Minister Andrew Hoggard says. “Cabinet has approved new funding of $20 million to enable MPI to meet unbudgeted ongoing expenses associated with the H7N6 response including rigorous scientific testing of samples at the enhanced PC3 ...3 days ago

- Levelling the playing field for media advertising

Legislation that will repeal all advertising restrictions for broadcasters on Sundays and public holidays has passed through first reading in Parliament today, Media Minister Paul Goldsmith says. “As a growing share of audiences get their news and entertainment from streaming services, these restrictions have become increasingly redundant. New Zealand on ...3 days ago

- Inspector-General of Defence appointed

Today the House agreed to Brendan Horsley being appointed Inspector-General of Defence, Justice Minister Paul Goldsmith says. “Mr Horsley’s experience will be invaluable in overseeing the establishment of the new office and its support networks. “He is currently Inspector-General of Intelligence and Security, having held that role since June 2020. ...3 days ago

- Fire and Emergency New Zealand final levy rates confirmed

Minister of Internal Affairs Brooke van Velden says the Government has agreed to the final regulations for the levy on insurance contracts that will fund Fire and Emergency New Zealand from July 2026. “Earlier this year the Government agreed to a 2.2 percent increase to the rate of levy. Fire ...3 days ago

- More AML relief on the way for Kiwi businesses

The Government is delivering regulatory relief for New Zealand businesses through changes to the Anti-Money Laundering and Countering Financing of Terrorism Act. “The Anti-Money Laundering and Countering Financing of Terrorism Amendment Bill, which was introduced today, is the second Bill – the other being the Statutes Amendment Bill - that ...3 days ago

- Hawke’s Bay Expressway moving at pace

Transport Minister Simeon Brown has welcomed further progress on the Hawke’s Bay Expressway Road of National Significance (RoNS), with the NZ Transport Agency (NZTA) Board approving funding for the detailed design of Stage 1, paving the way for main works construction to begin in late 2025.“The Government is moving at ...3 days ago

- Government seeks partnerships to plant trees on Crown-owned-land

The Government today released a request for information (RFI) to seeking interest in partnerships to plant trees on Crown-owned land with low farming and conservation value (excluding National Parks) Forestry Minister Todd McClay announced. “Planting trees on Crown-owned land will drive economic growth by creating more forestry jobs in our regions, providing more wood ...3 days ago

- Wide ranging legislation to make justice system more efficient

Court timeliness, access to justice, and improving the quality of existing regulation are the focus of a series of law changes introduced to Parliament today by Associate Minister of Justice Nicole McKee. The three Bills in the Regulatory Systems (Justice) Amendment Bill package each improve a different part of the ...3 days ago

- Diverse skills in community trust appointments

A total of 41 appointments and reappointments have been made to the 12 community trusts around New Zealand that serve their regions, Associate Finance Minister Shane Jones says. “These trusts, and the communities they serve from the Far North to the deep south, will benefit from the rich experience, knowledge, ...4 days ago

- Torture redress for survivors of the Lake Alice Unit

The Government has confirmed how it will provide redress to survivors who were tortured at the Lake Alice Psychiatric Hospital Child and Adolescent Unit (the Lake Alice Unit). “The Royal Commission of Inquiry into Abuse in Care found that many of the 362 children who went through the Lake Alice Unit between 1972 and ...4 days ago

- A busy year in the House

It has been a busy, productive year in the House as the coalition Government works hard to get New Zealand back on track, Leader of the House Chris Bishop says. “This Government promised to rebuild the economy, restore law and order and reduce the cost of living. Our record this ...4 days ago

- Consultation opens on working with engineered stone

“Accelerated silicosis is an emerging occupational disease caused by unsafe work such as engineered stone benchtops. I am running a standalone consultation on engineered stone to understand what the industry is currently doing to manage the risks, and whether further regulatory intervention is needed,” says Workplace Relations and Safety Minister ...4 days ago

- Greater reporting on Treaty settlement commitments

Mehemea he pai mō te tangata, mahia – if it’s good for the people, get on with it. Enhanced reporting on the public sector’s delivery of Treaty settlement commitments will help improve outcomes for Māori and all New Zealanders, Māori Crown Relations Minister Tama Potaka says. Compiled together for the ...4 days ago

- New appointments to the Charities Registration Board

Mr Roger Holmes Miller and Ms Tarita Hutchinson have been appointed to the Charities Registration Board, Community and Voluntary Sector Minister Louise Upston says. “I would like to welcome the new members joining the Charities Registration Board. “The appointment of Ms Hutchinson and Mr Miller will strengthen the Board’s capacity ...4 days ago

- Building consent processing times improve

More building consent and code compliance applications are being processed within the statutory timeframe since the Government required councils to submit quarterly data, Building and Construction Minister Chris Penk says. “In the midst of a housing shortage we need to look at every step of the build process for efficiencies ...4 days ago

- Faster access to support through Innovation Fund

Mental Health Minister Matt Doocey is proud to announce the first three recipients of the Government’s $10 million Mental Health and Addiction Community Sector Innovation Fund which will enable more Kiwis faster access to mental health and addiction support. “This fund is part of the Government’s commitment to investing in ...4 days ago

- New Zealand to assist Vanuatu on earthquake response

New Zealand is providing Vanuatu assistance following yesterday's devastating earthquake, Foreign Minister Winston Peters says. "Vanuatu is a member of our Pacific family and we are supporting it in this time of acute need," Mr Peters says. "Our thoughts are with the people of Vanuatu, and we will be ...4 days ago

- Government takes steps to reduce card fees for Kiwis

The Government welcomes the Commerce Commission’s plan to reduce card fees for Kiwis by an estimated $260 million a year, Commerce and Consumer Affairs Minister Andrew Bayly says.“The Government is relentlessly focused on reducing the cost of living, so Kiwis can keep more of their hard-earned income and live a ...4 days ago

- Review recommends ECE regulation shakeup

Regulation Minister David Seymour has welcomed the Early Childhood Education (ECE) regulatory review report, the first major report from the Ministry for Regulation. The report makes 15 recommendations to modernise and simplify regulations across ECE so services can get on with what they do best – providing safe, high-quality care ...4 days ago

- Offshore Renewable Energy Bill passes first reading

The Government‘s Offshore Renewable Energy Bill to create a new regulatory regime that will enable firms to construct offshore wind generation has passed its first reading in Parliament, Energy Minister Simeon Brown says.“New Zealand currently does not have a regulatory regime for offshore renewable energy as the previous government failed ...4 days ago

- Local Government (Water Services) Bill passes first reading

Legislation to enable new water service delivery models that will drive critical investment in infrastructure has passed its first reading in Parliament, marking a significant step towards the delivery of Local Water Done Well, Local Government Minister Simeon Brown and Commerce and Consumer Affairs Minister Andrew Bayly say.“Councils and voters ...4 days ago

- Gene Technology Bill passes first reading

New Zealand is one step closer to reaping the benefits of gene technology with the passing of the first reading of the Gene Technology Bill, Science, Innovation and Technology Minister Judith Collins says. "This legislation will end New Zealand's near 30-year ban on gene technology outside the lab and is ...4 days ago

- New Zealand ratifies AANZFTA Upgrade

New Zealand has ratified the Upgrade to the Agreement establishing the ASEAN-Australia-New Zealand Free Trade Area (AANZFTA), Minister for Trade Todd McClay announced today. “ASEAN which is comprised of Brunei Darussalam, Cambodia, Indonesia, Lao PDR, Malaysia, Myanmar, Philippines, Singapore, Thailand, and Vietnam, is New Zealand’s fourth largest trading partner in two-way trade – ...4 days ago

- Caitlin Johnstone: Where does the aggression really begin?

Report by Dr David Robie – Café Pacific. – COMMENTARY: By Caitlin Johnstone New York prosecutors have charged Luigi Mangione with “murder as an act of terrorism” in his alleged shooting of health insurance CEO Brian Thompson earlier this month. This news comes out at the same time as ...3 hours ago

Report by Dr David Robie – Café Pacific. – COMMENTARY: By Caitlin Johnstone New York prosecutors have charged Luigi Mangione with “murder as an act of terrorism” in his alleged shooting of health insurance CEO Brian Thompson earlier this month. This news comes out at the same time as ...3 hours ago - OECD Report Highlights That More Is Needed

This report reflects that gap in our dealings overseas, and it shows that legislators, the public sector and businesses need to walk the talk. ...11 hours ago

This report reflects that gap in our dealings overseas, and it shows that legislators, the public sector and businesses need to walk the talk. ...11 hours ago - Government quietly scraps waste minimisation policies

The government has quietly cancelled plans to improve recycling and roll out a kerbside food scraps composting scheme. ...12 hours ago

The government has quietly cancelled plans to improve recycling and roll out a kerbside food scraps composting scheme. ...12 hours ago - MEAA welcomes News MAP funding ‘leg up’ for Australian journalism

Pacific Media Watch The union for Australian journalists has welcomed the delivery by the federal government of more than $150 million to support the sustainability of public interest journalism over the next four years. Combined with the announcement of the revamped News Bargaining Initiative, this could result in up to ...13 hours ago

- Transmission Gully partnership breakdown will not hurt future public-private partnerships, Infrastru...

The roads partnership unravelled under a confidential settlement this week, meaning NZTA will now finish off what it had said was incomplete work. ...18 hours ago

- Funding cuts to charity particularly felt over Christmas period

The number of people seeking help from Lifeline is expected to increase by 10 to 20 percent over Christmas. ...20 hours ago

- Nelson Hospital conditions ‘unbearable’ – staff

One worker says the building is decrepit and falling down around them. ...20 hours ago

- The Secret Diary of .. Luxon at Xmas

MONDAY“Merry Xmas, and praise the Lord,” said Sheriff Luxon, and smiled for the camera. There was a flash of smoke when the shutter pressed down on the magnesium powder. The sheriff had arranged for a photographer from the Dodge Gazette to attend a ceremony where he handed out food parcels to ...20 hours ago

MONDAY“Merry Xmas, and praise the Lord,” said Sheriff Luxon, and smiled for the camera. There was a flash of smoke when the shutter pressed down on the magnesium powder. The sheriff had arranged for a photographer from the Dodge Gazette to attend a ceremony where he handed out food parcels to ...20 hours ago - Stand by for cricket’s Smash Palace

It’s a little under two months since the White Ferns shocked the cricketing world, deservedly taking home the T20 World Cup. Since then the trophy has had a tour around the country, five of the squad have played in the WBBL in Australia while most others have returned to domestic ...20 hours ago

- Early-onset dementia under the microscope

Comment: If we say the word ‘dementia’, many will picture an older person struggling to remember the names of their loved ones, maybe a grandparent living out their final years in an aged care facility. Dementia can also occur in people younger than 65, but it can take time before ...20 hours ago

- Keeping the pirates at bay: Should the Australian ‘Blocking Order’ case prompt a discussion in N...

Piracy is a reality of modern life – but copyright law has struggled to play catch-up for as long as the entertainment industry has existed. As far back as 1988, the House of Lords criticised copyright law’s conflict with the reality of human behaviour in the context of burning cassette ...20 hours ago

- ‘We were as famous as Tom Cruise’: Craig Parker on 90s Shortland St fandom

As he makes a surprise return to Shortland Street, actor Craig Parker takes us through his life in television. Craig Parker has been a fixture on television in Aotearoa for nearly four decades. He had starring roles in iconic local series like Gloss, Mercy Peak and Diplomatic Immunity, featured in ...21 hours ago

As he makes a surprise return to Shortland Street, actor Craig Parker takes us through his life in television. Craig Parker has been a fixture on television in Aotearoa for nearly four decades. He had starring roles in iconic local series like Gloss, Mercy Peak and Diplomatic Immunity, featured in ...21 hours ago - ‘I prioritise the mission, not my health’: Adam McGrath’s perfect weekend playlist

The Ōtautahi musician shares the 10 tracks he loves to spin, including the folk classic that cured him of a ‘case of the give-ups’. When singer-songwriter Adam McGrath returns to Kumeu’s Auckland Folk Festival from January 24-27, he’s not planning on simply idling his way through – he wants the late ...21 hours ago

- The rescue dog bringing joy to Christchurch retirement homes

Alex Casey spends an afternoon on the job with River, the rescue dog on a mission to spread joy to Ōtautahi rest homes. Almost everyone says it is never enough time. But River the rescue dog, a jet black huntaway border collie cross, has to keep a tight pace to ...21 hours ago

- Fiji pro-Palestine nativity scene exposes Gaza as ‘hell on earth’ at Christmas

Asia Pacific Report Fiji activists have recreated the nativity scene at a solidarity for Palestine gathering in Fiji’s capital Suva just days before Christmas. The Fiji Women’s Crisis Centre and Fijians for Palestine Solidarity Network recreated the scene at the FWCC compound — a baby Jesus figurine lies amidst the ...1 day ago

- Vanuatu quake: ‘Our shop was flattened like a deck of cards’

By 1News Pacific correspondent Barbara Dreaver and 1News reporters A number of Kiwis have been successfully evacuated from Vanuatu after a devastating earthquake shook the Pacific island nation earlier this week. The death toll was still unclear, though at least 14 people were killed according to an earlier statement from ...1 day ago

- How diplomats have broken the law in NZ – and what happened next

A handful of foreign diplomats have misbehaved during their time here - and not all of them have been brought to justice. ...1 day ago

- Swim schools report sinking enrolments as downturn deepens

Being able to swim is often considered a life skill, but tough economic times are forcing many families to pull their children out of lessons. ...1 day ago

- ‘There will be deaths because of this’ – Warning over Health NZ IT cuts

A West Coast IT worker is warning patients will die as Health New Zealand aims to slash its data and digital staff. ...1 day ago

- Polytech sales possible but unlikely when Te Pūkenga disestablished – minister

In a surprise move, the sale of polytechnics will be on the table when the national institute of technology Te Pūkenga is disestablished. ...1 day ago

- Parliament’s final sitting day an insight into party factions

On Parliament's last day of the year, there was a rare glimpse of the factions within the major parties. ...1 day ago

- Former Labour MP, North Shore mayor Ann Hartley dies

Former Labour MP and mayor of Auckland's North Shore City Ann Hartley has died. ...1 day ago

- The closest thing Australian cartooning had to a prophet: the sometimes celebrated, sometimes contro...

Source: The Conversation (Au and NZ) – By Richard Scully, Professor in Modern History, University of New England Bunker. Image courtesy of Michael Leunig, CC BY-NC-SA Michael Leunig – who died in the early hours of Thursday December 19, surrounded by “his children, loved ones, and sunflowers” – was the ...1 day ago

- Labour moves Speaker from the ‘nice’ to ‘naughty’ list

Last week's fights with the Speaker over the Fast Track schedule may have changed the tone in Parliament. ...1 day ago

- Govt ends pilot programme for Māori and Pacific, sparking outrage

The Government announced the end of the programme that allowed Māori and Pacific people to acess bowel cancer screening at 50-years-old. ...1 day ago

- Parliament fits an extra morning into final sitting day

The House - On Parliament's last day of the year, there was the rare occurrence of a personal (conscience) vote on selling booze over the Easter weekend. While it didn't have the numbers to pass, it was a chance to get a rare glimpse of the fact ...1 day ago

- The Friday Poem: ‘Bejeweled log’ by Holly Fletcher

A new poem by Holly Fletcher. bejeweled log i was dreaming about wasps / wee darlings that followed me / ducking under objects / that i was fated to pickup / my fingers seeking / and meeting with tiny proboscis’s / but instead / i wake up / roll sideways ...2 days ago

- Sunglasses don’t just look good – they’re good for you too. Here’s how to choose the right p...

Source: The Conversation (Au and NZ) – By Flora Hui, Research Fellow, Centre for Eye Research Australia and Honorary Fellow, Department of Surgery (Ophthalmology), The University of Melbourne Versta/Shutterstock Australians are exposed to some of the highest levels of solar ultraviolet (UV) radiation in the world. While we ...2 days ago

- How does franchising work?

Source: The Conversation (Au and NZ) – By Andrew Terry, Professor of Business Regulation, University of Sydney Michael von Aichberger/Shutterstock Even if you’ve no idea how the business model underpinning franchises works, there’s a good chance you’ve spent money at one. Franchising is essentially a strategy for cloning ...2 days ago

- The one episode of Shortland Street you need to watch this year

If something big is going to happen in Ferndale, it’s going to happen at Christmas. This is an excerpt from our weekly pop culture newsletter Rec Room. Sign up here. If there’s one episode of Shortland Street you should watch each year, it’s the annual Christmas cliffhanger. The final episode of ...2 days ago

- As China expands its cyber espionage and sabotage operations, how will the Trump administration resp...